Prices

April 24, 2016

Comparison Price Indices: Still Moving by Double Digits

Written by John Packard

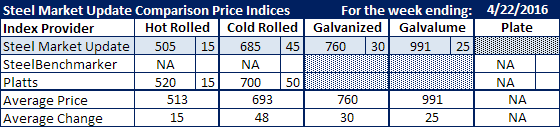

The steel indexes followed by Steel Market Update showed flat rolled steel spot prices continuing their climb higher as all products moved by double digits. Both Platts and SMU took hot rolled prices up by $15 per ton, although there is a $15 per ton spread between the two indexes.

Based on the SMU index, hot rolled is now at a 14 month high having last achieved $505 or higher back in the middle of February 2015.

Cold rolled rose by $45 (SMU) and $50 (Platts) and there continues to be a $15 per ton spread between the two indexes on CRC.

For cold rolled you have to go all the way back to January 2015 before you find a number higher than the $685 reported by SMU last week (14 months).

Galvanized went up by $30 per ton to $760 per ton for .060” G90 and Galvalume rose by $25 per ton on .0142” AZ50, Grade 80 and is now averaging $991 per ton.

Galvanized is also at a 14 month high as is Galvalume.

We did not have new plate prices in time for our deadline for publication.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.