Prices

June 12, 2016

Comparison Price Indices: One Last Time…

Written by John Packard

Last week Steel Market Update advised our readers that we were considering removing the Comparison Price Indices article from our newsletter. The index has more value, in our opinion, when there is a wider array of data points available to be compared. We publish only the indices where we have permission to do so. Over the years the number of indices has dropped to the current two plus our own SMU index.

We have not received any objections to having us remove the Comparison Price Indices articles from the newsletter therefore, this will be the last one produced.

Steel Market Update (SMU) will find other ways to note when there are large variations between the various indexes used to follow flat rolled pricing, steel contracts and for financial contracts.

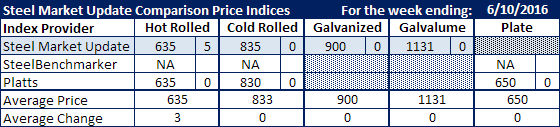

There was very little movement in flat rolled pricing this past week as both SMU and Platts saw benchmark hot rolled coil at $635 per ton ($31.75/cwt).

Cold rolled prices were referenced as being $835 per ton at SMU and $830 per ton by Platts.

Both galvanized and Galvalume prices remained the same (.060 G90 GI and .0142 AZ50, Grade 80 for AZ).

Platts kept their plate prices the same at $650 per ton.

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.