Market Data

July 7, 2016

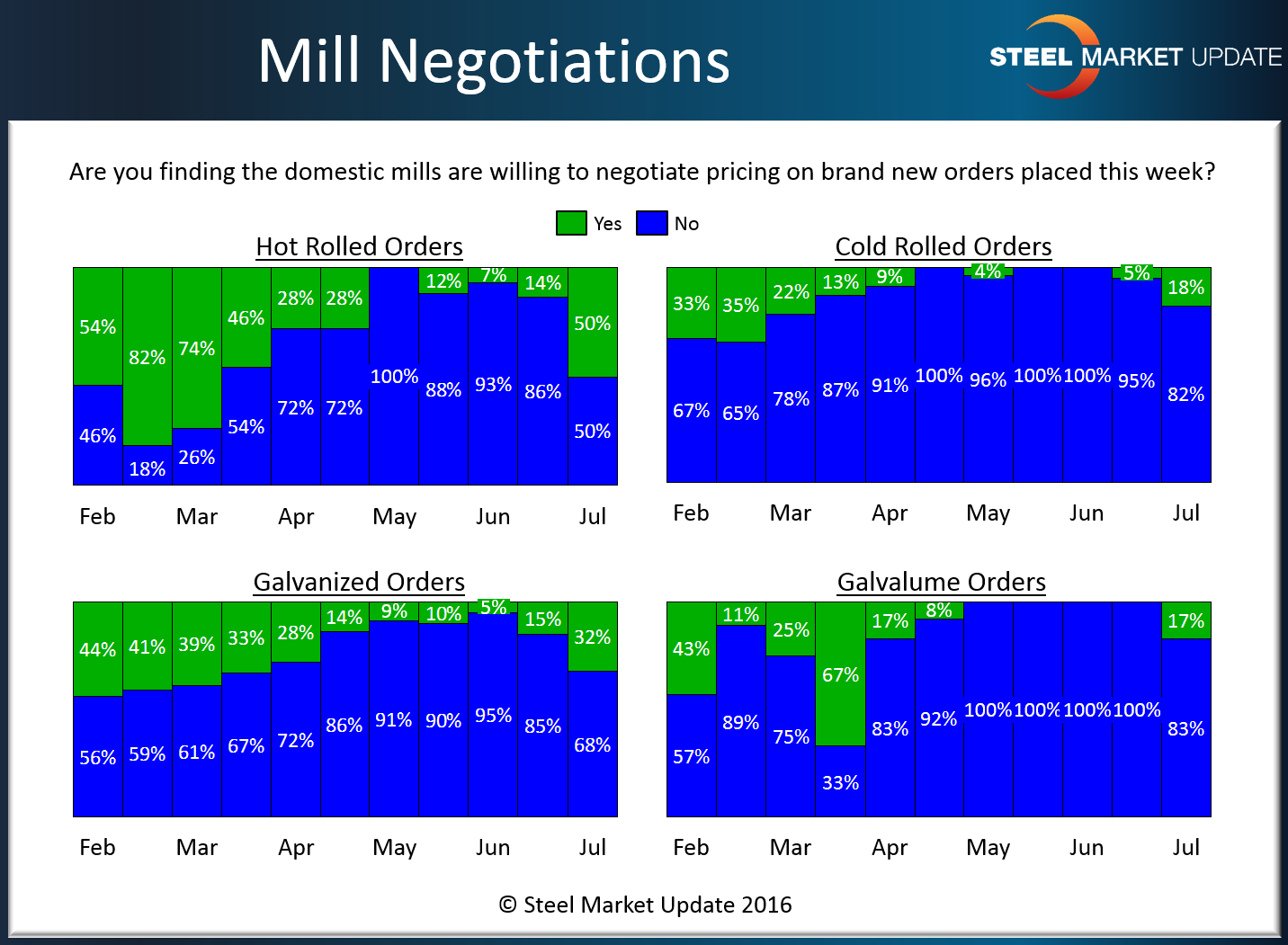

SMU Survey: Mill Negotiations

Written by John Packard

A second key subject addressed in our flat rolled steel survey regards negotiations between the domestic steel mills and their customers. We ask manufacturing companies and steel service centers to comment on whether their domestic mill suppliers are willing to negotiate spot steel pricing on hot rolled, cold rolled, galvanized and Galvalume steels.

The less willing mills are to negotiate the better able the mills are at keeping pricing firm. We are looking for trends or changes and we did see that in hot rolled this week where 50 percent of our respondents reported the mills as willing to negotiate HR prices this week. Two weeks ago, and for the past few months, there has been a relatively small percentage of respondents reporting HR prices as negotiable.

Cold rolled saw a very small increase (18 percent from 5 percent), galvanized a slightly larger increase (15 percent to 32 percent) as well as Galvalume (0 to 17 percent).

With this week being a holiday week (4th of July), the number of respondents was slightly lower than normal so we will watch the next survey to see if this is the beginning of a trend or just a blip in our numbers.

We remind our readers these results are based on responses to our survey. Each individual mill may have different approaches to negotiations and steel markets can be quite volatile and change quickly. It is important to stay close to your suppliers to make sure you are being kept up to date as to what they are doing and how your company fits into their plans.

A side note: The data for both lead times and negotiations comes from only service center and manufacturer respondents. We do not include commentary from the steel mills, trading companies, or toll processors in this particular group of questions.

To see an interactive history of our Steel Mill Negotiations data, visit our website here.