Prices

July 17, 2016

Comparison Price Indices: Ho Hum Week

Written by John Packard

Flat rolled prices had a relatively “ho hum” week as we saw very little movement in any of the indexes with the exception of SteelBenchmarker which only produces prices twice per month.

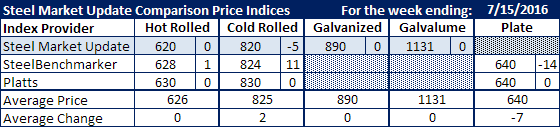

Benchmark hot rolled prices ranged from a low (average) from our own index which came in at $620 per ton for a second week. Platts remained unchanged at $630 per ton while SteelBenchmarker came in at $628 per ton. The average for the three indexes is $626 per ton.

Cold rolled prices were similar to that of HRC only $200 per ton higher. The SMU cold rolled average was down $5 per ton to $820 per ton. Platts remained unchanged at $830 per ton while SteelBenchmarker came in up $11 to $824 per ton. The average of the three indexes came in at $825 per ton.

Both galvanized (.060” G90) and Galvalume (.0142” AZ50, Grade 80) were unchanged.

SMU Price Momentum Indicator continues to be referenced as “Neutral” meaning our expectation is for prices to track sideways (+/- $20 per ton) over the next 30 days.

FOB Points for each index:

FOB Points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.