Prices

March 5, 2017

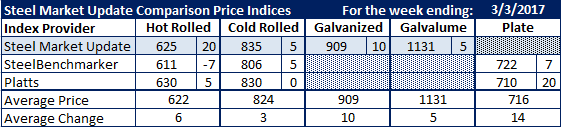

Comparison Price Indices: Back to Trending Higher

Written by John Packard

Flat rolled steel prices rose this past week on every item with the exception of the SteelBenchmarker hot rolled index.

Steel Market Update (SMU) saw benchmark hot rolled as up $25 per ton to $625 per ton. Platts moved up $5 per ton to $630 per ton and SteelBenchmarker, who reports prices twice per month, had HRC dropping by $7 per ton to $611 per ton.

Cold rolled prices had SMU at $835 per ton while Platts was unchanged at $830 per ton and SteelBenchmarker was up $5 to $806 per ton.

Galvanized G90 .060” was up $10 per ton to $909 per ton. Please note SMU continues to use the January 1, 2017 G90 coating extras. However, with lead times already in April and beyond, we will most likely adjust our pricing to reflect the new extras in next week’s numbers.

Galvalume pricing was also up $5 per ton on .0142” AZ50, Grade 80 material.

Plate prices rose by $7 per ton at SteelBenchmarker and $20 per ton at Platts. Note: Nucor announced a $30 per ton price increase on carbon and alloy plate and $50 per ton on heat-treated plate on Friday, March 3rd.

SMU Note: Galvanized prices include $69 in extras for a .060″ G90 product. Galvalume prices include $291 in extras for a .0142” AZ50 Grade 80 product.

FOB points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.