Market Data

April 20, 2017

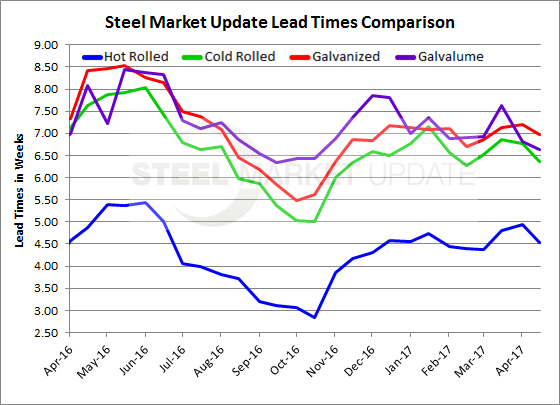

Lead Times: Survey Results vs. Mill Published Reports

Written by John Packard

Over the course of the last four days Steel Market Update (SMU) has been conducting our mid-April flat rolled steel market trends analysis. We finished earlier this afternoon and we are providing the results of some of our findings to our readers this evening.

Lead times, which is the length of time it takes to get an order produced, are on average shrinking according to those participating in our trends survey (note: our survey results may be different than what is being reported by each individual mill to their customers – we will have more on this at the end of this article).

We are seeing hot rolled lead times now at 4.54 weeks compared to 5 weeks at the beginning of this month. One year ago, HRC lead times were 4.87 weeks.

Cold rolled lead times are averaging just shy 6.5 weeks (6.37) down slightly from the 6.78 weeks reported at the beginning of this month and well below the 7.62 weeks we reported during the middle of April 2016.

Galvanized lead times are now averaging 7 weeks (6.98 weeks) based on our survey results. This is down slightly from the 7.19 weeks reported at the beginning of this month and well below the 8.42 weeks we reported during the middle of April 2016.

Galvalume lead times are close to what was reported at the beginning of April. AZ lead times are now 6.63 weeks, down slightly from the 6.82 weeks reported in early April. One year ago, AZ lead times were 8.08 weeks.

Quick Check of Mill Lead Time Reports

As we discussed above, the lead times we are reporting today are the average of all the data we collected from buyers in manufacturing and service centers. We wanted to see how the averages we are reporting (and most are trending as being slightly shorter than just a couple of weeks ago) compare to a few steel mills who published lead time sheets to their customers this week.

NLMK USA

Hot rolled: Portage = week of June 5th (6-7 weeks), Farrell (from slabs) = week of 5/22 (5 weeks).

Cold rolled: Farrell = week of 6/19 for fully processed (8-9 weeks).

Galvanized: Sharon Coatings = week of 6/19 (8-9 weeks).

Nucor Berkeley

Hot rolled: week ending 6/10 to 6/17 depending on widths (10-12 weeks)

Cold rolled: week ending 6/10 to 6/17 depending on widths (10-12 weeks)

Galvanized: inquire only

ArcelorMittal USA and AM/NS Calvert

Hot rolled: Burns Harbor week ending 5/27 (4-5 weeks), Indiana Harbor West week of 5/14 (3-4 weeks), Cleveland week of July 2 (10-11 weeks), Riverdale week ending July 15 (11-12 weeks), Calvert is not available as they have been having some production issues.

Cold rolled: Burns Harbor week of June 4 (6-7 weeks), Calvert week of June 11 (7-8 weeks), Cleveland week of June 4 (6-7 weeks), East Chicago week of June 4 (6-7 weeks), TEK week of June 4 (-7 weeks).

Galvanized: Calvert week of July 2 (10-11 weeks), Indiana Harbor West week of July 2 (10-11 weeks).

This is not a complete listing by any means but it will give our readers a feel for what a number of the mills are quoting to their customers as of the last 24 hours.

A side note: The data for both lead times and negotiations comes from only service center and manufacturer respondents. We do not include commentary from the steel mills, trading companies, or toll processors in this particular group of questions.

To see an interactive history of our Steel Mill Negotiations data, visit our website here.