Prices

June 6, 2017

SMU Price Ranges & Indices: Mixed Results

Written by John Packard

Flat rolled prices were mixed this week as the domestic steel mills announced their $30 per ton price increase and steel buyers placed whatever orders they were allowed to under the existing pricing agreements. We saw a tightening of the range on hot rolled while cold rolled was unchanged, galvanized was down $5 per ton, Galvalume was down $10 per ton and plate was up $15 per ton.

Here is how we see prices this week:

Hot Rolled Coil: SMU price range is $560-$600 per ton ($28.00/cwt-$30.00/cwt) with an average of $580 per ton ($29.00/cwt) FOB mill, east of the Rockies. The lower end of our range increased $10 per ton compared to one week ago while the upper end decreased $10 per ton. Our overall average is unchanged compared to last week. Our price momentum on hot rolled steel is pointing to Lower which means we expect prices to decline over the next 30-60 days.

Hot Rolled Lead Times: 3-5 weeks

Cold Rolled Coil: SMU price range is $740-$810 per ton ($37.00/cwt-$40.50/cwt) with an average of $775 per ton ($38.75/cwt) FOB mill, east of the Rockies. Both the upper and lower ends of our range remained the same compared to last week. Our overall average is unchanged compared to one week ago. Our price momentum on cold rolled steel is pointing to Lower which means we expect prices to decline over the next 30-60 days.

Cold Rolled Lead Times: 4-8 weeks

Galvanized Coil: SMU base price range is $37.00/cwt-$40.00/cwt ($740-$800 per ton) with an average of $38.40/cwt ($770 per ton) FOB mill, east of the Rockies. The lower end of our range was unchanged compared to one week ago while the upper end declined $10 per ton. Our overall average is down $5 per ton compared to last week. Our price momentum on galvanized steel is pointing to Lower which means we expect prices to decline over the next 30-60 days.

Galvanized .060” G90 Benchmark: SMU price range is $818-$878 per net ton with an average of $848 per ton FOB mill, east of the Rockies.

Galvanized Lead Times: 4-7 weeks

Galvalume Coil: SMU base price range is $38.00/cwt-$40.00/cwt ($760-$800 per ton) with an average of $39.00/cwt ($780 per ton) FOB mill, east of the Rockies. The lower end of our range remained the same compared to last week while the upper end declined $20 per ton. Our overall average is down $10 per ton compared to one week ago. Our price momentum on Galvalume steel is pointing to Lower which means we expect prices to decline over the next 30-60 days.

Galvalume .0142” AZ50, Grade 80 Benchmark: SMU price range is $1051-$1091 per net ton with an average of $1071 per ton FOB mill, east of the Rockies.

Galvalume Lead Times: 5-10 weeks

Plate: SMU price range is $730-$780 per ton ($36.50/cwt-$39.00/cwt) with an average of $755 per ton ($37.75/cwt) FOB delivered. The lower end of our range rose $10 per ton compared to one week ago while the upper end increased $20 per ton. Our overall average is up $15 per ton compared to last week. Our price momentum on plate steel is pointing to Lower which means we expect prices to decline over the next 30-60 days.

Plate Lead Times: 4-8 weeks

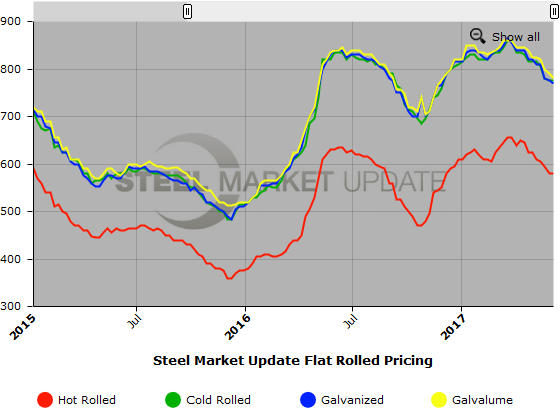

SMU Note: Below is a graphic showing our hot rolled, cold rolled, galvanized, and Galvalume price history. We will add plate prices to this graph once we have gathered a few months of data. To use the graphs interactive capabilities, you must view it on our website here. If you need help navigating the website or need to know your login information, contact us at info@SteelMarketUpdate.com or by calling 800-432-3475.