Prices

September 21, 2017

Pace of Foreign Steel Import Licenses Picks Up

Written by John Packard

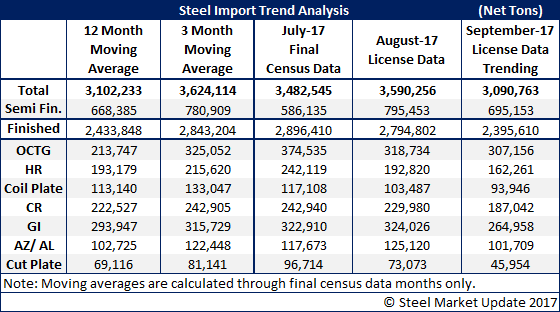

Earlier this month, foreign steel imports for September were trending toward a 2.6-million-ton month based on import licenses through the first 12 days of the month. Over the past week, the pace for import license requests has picked up. This is most likely due to the impact of the two hurricanes: Harvey in Texas and Irma in Florida. Based on the latest import license data, September is now trending toward a 3.0-million-ton month. The trend is modestly lower than our 12-month and 3-month moving averages. Yet, it is a bit of a disappointment as the steel industry is expecting foreign steel imports to drop dramatically due to the threat of the Section 232 investigation on steel from earlier this year. That threat has now been pushed out to maybe as late as 1Q next year.

![]() One of the products gaining traction after a slow start are semi-finished steels, the bulk of which are slabs. All of the semi’s imported into the country are done so by domestic steel, plate and pipe producers. Companies like NLMK USA, JSW, California Steel, AM/NS Calvert, Acero Junction, etc.

One of the products gaining traction after a slow start are semi-finished steels, the bulk of which are slabs. All of the semi’s imported into the country are done so by domestic steel, plate and pipe producers. Companies like NLMK USA, JSW, California Steel, AM/NS Calvert, Acero Junction, etc.

When looking at individual flat rolled products, we are finding the trend on hot rolled, cold rolled and galvanized to be less than their 12-month and 3-month moving averages.

The biggest exporters of hot rolled are Canada, Turkey, Brazil and Korea. Countries that are now exporting HRC to the U.S. but were not doing so one year ago include: Thailand, Malaysia, Egypt, Guatemala and Saudi Arabia. Most of these new mills are at relatively small tonnages or are shipping every other month, as opposed to consistently month in and month out.

Mexico is a modest supplier these days at around 10,000 net tons per month. Based on license data for September, they are trending toward a 6,400-ton month.

Mexico is a bigger player in cold rolled having exported approximately 21,000 net tons in August (and 10,000 net tons of galvanized).

The main cold rolled exporting countries right now are: Turkey, Russia, Canada and Mexico.

The Vietnam circumvention suit is scheduled by the Department of Commerce to receive the preliminary findings in mid-October. Galvanized exports from Vietnam were 13,800 net tons in August, but their trend for September is for 4,500 net tons. Last September, Vietnam shipped 53,700 net tons of GI steel to the United States.

The biggest exporting countries of galvanized right now are: Canada, Turkey, Korea, Brazil, Taiwan and United Arab Emirates (UAE).

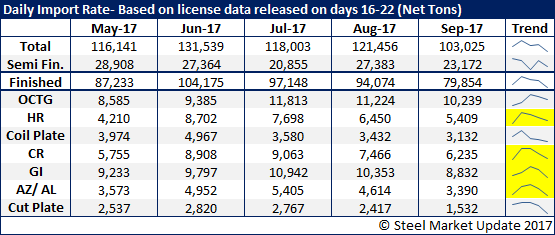

To get a better feel of how license data for September compares with prior months, see the table below. The license data below was collected between the 16th and 22nd days of each respective month.