Prices

December 10, 2017

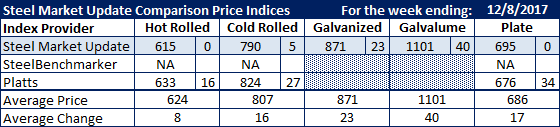

Comparison Price Indices: Platts Bumps Numbers While SMU Waits

Written by John Packard

Flat rolled prices moved higher as the domestic mills announced yet another price increase this past week. There is now a large division between Platts and Steel Market Update (SMU) steel indexes as we prefer to wait a few days to let the dust settle after an increase has been announced.

Benchmark hot rolled, prior to the announcements, was reported to be $615 per ton by SMU and $617 per ton by Platts. By the end of the week, Platts moved their HRC average to $633 per ton ($632.75 is the actual number). The Platts number is up $16 per ton since the beginning of the week. SteelBenchmarker did not report prices this past week as they only produce prices twice per month.

Cold rolled had similar results to HRC as the SMU index average on Tuesday was $790 per ton, up $5 per ton from the prior week. Platts took their CRC average to $824 per ton, up $27 per ton compared to earlier in the week.

Galvanized prices are now higher on .060” G90 as Steel Market Update took our coating extra up to reflect the higher extras being asked by all of the mills except U.S. Steel (USS has yet to publish new coating extras).

Galvalume spot prices on .0142” AZ50, Grade 80 rose by $40 per ton to $1,101 per ton.

SMU held plate prices steady as we wait for the impact of the latest price announcement (up $50 per ton). Platts took their plate numbers up to $676 per ton (FOB SE Mill). The Platts number is $34 per ton higher than where they were at the beginning of this past week. Note: SMU plate numbers are delivered to the customer numbers.

SMU Note: Galvanized prices include $86 in extras for a .060″ G90 product. Galvalume prices include $291 in extras for a .0142” AZ50 Grade 80 product.

FOB points for each index:

SMU: Domestic Mill, East of the Rockies.

SteelBenchmarker: Domestic Mill, East of the Mississippi.

Platts: Northern Indiana Domestic Mill.

Plate price FOB points are different for each of the indexes:

SMU: FOB Delivered to the Customer (includes freight)

Platts: FOB Southeaster Mill (does not include freight)

Note that SteelBenchmarker produces numbers twice per month. On the weeks they produce numbers we will include them in the average. The weeks where they do not produce numbers (NA = not available) we will not include their outdated numbers in the CPI average.