Prices

December 12, 2017

How High Can Steel Prices Climb?

Written by John Packard

Steel Market Update recently adjusted our Price Momentum Indicator to “Higher” as, in our opinion, steel buyers should anticipate flat rolled steel prices to move up over the next 30 to 60 days. During last week’s analysis of the flat rolled steel market, 78 percent of the respondents agreed with SMU, sensing that pricing momentum has shifted to the domestic mills and that steel prices will be heading higher into the New Year. So, how high do steel buyers expect flat rolled prices to go in the coming months?

Even though our Price Momentum Indicator is pointing toward higher spot prices, there are more factors in play than just momentum. We are carefully watching demand, lead times, negotiation posturing and production at the steel mills. Before we look at what steel buyers have been saying to SMU over the past 24 hours, let’s first take a historical look at pricing and domestic mill production.

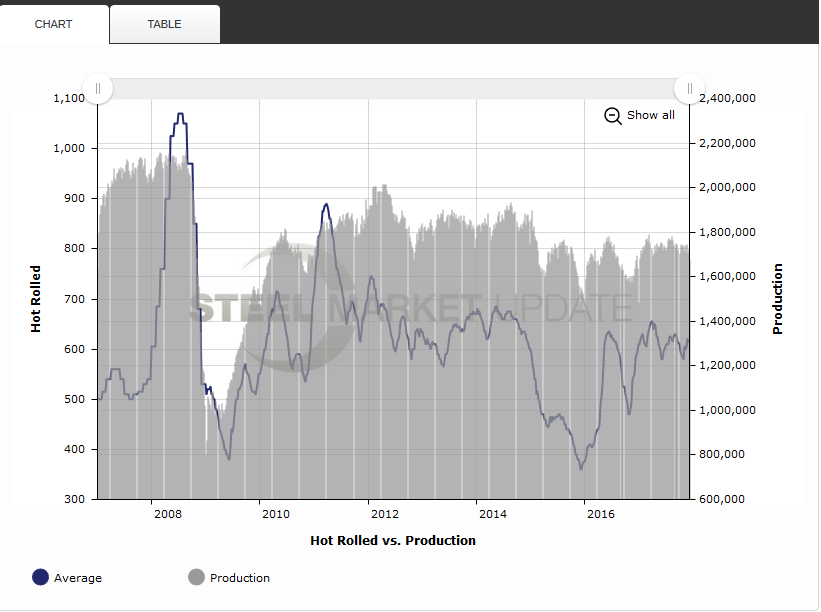

Below is a graphic taken off our website, which any member companies can reproduce on your own. The graphic depicts the weekly hot rolled average, which is overlaid on top of the weekly production numbers as provided by the American Iron and Steel Institute.

In the graphic, we show what the market was like prior to the crash at the end of September 2008. Once the crash occurred, prices plummeted through most of 2009. There was a strong recovery beginning in late 2009 and all through 2010 and 2011 before falling back during 2012.

Then we had the inventory correction and foreign steel flood slide of 2014/2015, which took benchmark hot rolled prices to the lowest point on our graphic at $360 per ton ($18.00/cwt) on Dec. 8, 2015.

The combination of higher than expected foreign steel imports due to the threat of Section 232 and the unknowns associated with the circumvention complaint kept pressure on domestic steel producers through 2017. The result has been production rates below 1,800,000 tons per week.

As you can gather from the graphic, the higher the production rates the better chance the domestic mills have to collect higher spot prices in the market.

As we move into 2018, we will be watching to see if there is any improvement in production rates, which would result in longer lead times and most likely higher prices.

How High Can Prices Go? Steel Buyers Offer Insights

As we maneuvered about the industry over the past two days, we asked steel buyers if they felt steel prices were poised to go higher and, if so, how high can they go? Here are some of their comments:

- “I would not have a problem maintaining normal inventory levels at the 31-32 for January delivery. I think the risk is for higher prices on even lower imports and better domestic demand. The tools available now (circumvention and self-initiation) could seriously affect pricing. Think Russia and Turkey investigated for circumvention and resulting shift to domestic purchases. There several other scenarios too…. With that in mind, peak prices could be very high. Consumers should be looking hard at hedging that risk if they have not already.” Service Center

- “I am not a buyer yet at these prices. I think there is a high likelihood these latest increases will stick (or most of it will stick). Every mill I talk to, both foreign and domestic, is extremely bullish. That said, I don’t think there is a lot of runway for prices from here if in fact CRU hits a current offer price of $680. That has to be the top barring an aggressive 232 ruling.” Service Center

- “I think we could see plate get close to $40.00/cwt delivered basis [$800 per ton].” Plate Service Center

- “I think Section 232 is difficult, but if they do something, this could really run. I like $38.00 delivered as a March peak [$760 per ton].” Plate Service Center

- “With futures continuing to rise and more expectations of price increases potentially by end of year, I am hedging more increases to come into the first quarter. All of the mills in the South look to have overbooked on HR and are shipping late. Lead times are much longer, in my opinion, than what is being reported.” This manufacturer went on to predict peak hot rolled at $680-$700 per ton.

- “If I had to peg a base at which this price cycle will peak, I would guess CRU around $42.00, with transaction numbers around $40.00/cwt.” Galvanized Buyer

- “We are going to run our inventories down, for the market is not that busy and the mill prices are $60 per ton greater than we are selling sheeted cold rolled into the marketplace. We have plenty of foreign to move. I believe the peak is here. The new pricing will slow purchases and the mills will be looking for orders, sooner rather than later.” East Coast Service Center

- “It’s always dependent upon the supply/demand balance and raw material input costs. Scrap will go up again in January, and if we have prolonged severe winter weather we might see a decent run-up. Our shipping rates have been much stronger year over year for the last four months and are expected to remain strong into the first quarter. I am bullish at this point, so I am going to go with $680/ton on hot rolled. Disclaimer: Government interference could change outcomes dramatically, be a non-event, or negatively impact the markets.” Service Center