Market Data

February 21, 2018

MSCI Data Shows Service Center Shipments Up in January

Written by Laura Remington

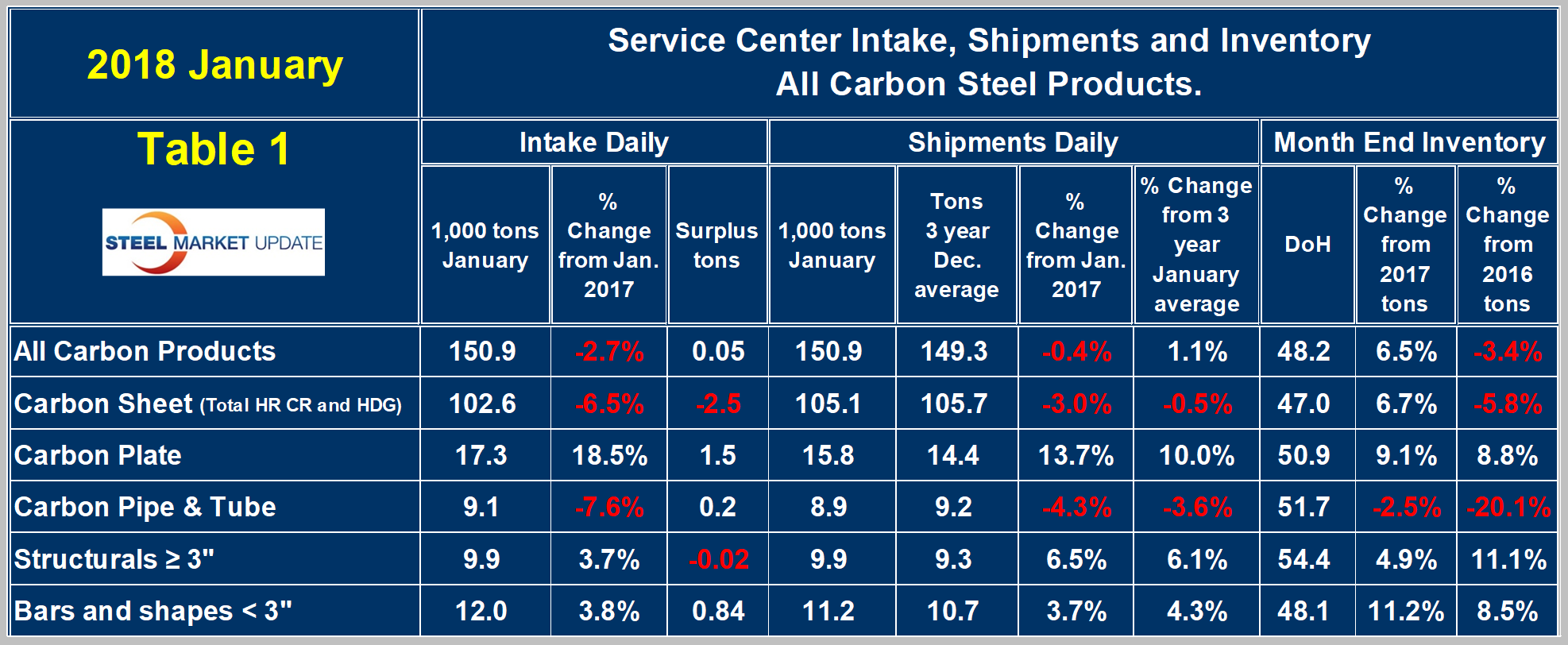

January service center intake rose 12 percent month over month but was flat compared to the seasonal norms and was down 2.7 percent compared to January 2017 intake. Daily shipments in January were 31.1 percent higher than in December and were 4.3 percent higher than January 2017. According to Steel Market Update’s latest analysis of Metals Service Center Institute data, on average since 2009 January shipments have risen 20 percent over December; therefore, these latest numbers were seasonally better than the historical average for this time of year. Carbon steel shipments averaged 140,300 tons per day, and with two additional shipping days, Days on Hand (DoH) as of the January 31 averaged 48.2 days, down from 57.3 at the end of December, but 3.1 points higher than January 2017 DoH.

Intake and Shipments

January carbon steel intake, defined as monthly shipments plus any inventory surplus, totaled 150,900 tons per day, up from 132,800 tons in December and exceeding the three-year January average by 3,600 tons. Albeit small, this was the second month of surplus following two monthly deficits in 4Q 2017. January sheet products data offset these gains with an intake deficit of 2,500 tons as reported month-end inventory for sheet products fell 1.1 percent compared to December 2017.

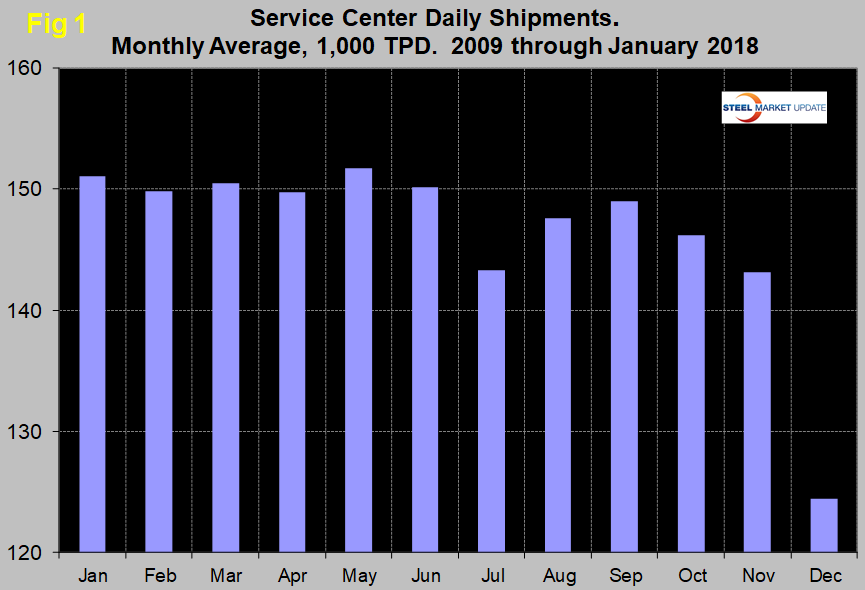

As is normal, shipments decreased in December, but the decline was less than the historical average. MSCI attributed some of the modestly stronger end-of-year shipments to pre-buying ahead of price increases. Total January daily carbon steel shipments increased from 126,600 tons in December to 150,900 tons. MSCI data is seasonal, so to eliminate that effect we report changes in shipments, intake and inventories on a year-over-year basis to get an undistorted view of market direction. Figure 1 exhibits this seasonality and illustrates why comparing a month’s performance with the previous month can be misleading, particularly in July and the fourth quarter of 2017.

Table 1 (click to enlarge) shows the performance by product in January compared to the same month last year along with the average daily shipments for this and the two previous months of January. We then calculate the percent change between January 2018 and January 2017 to compare it with the most recent three-year January average. January this year fell 0.4 percent from January 2017 and was up by 1.1 percent from the three-year January average. When the year-over-year growth comparison is better than the three-year comparison, it suggests that momentum is positive. Plate, structural and bar shipments were up from January last year, while sheet and pipe and tube products fell.

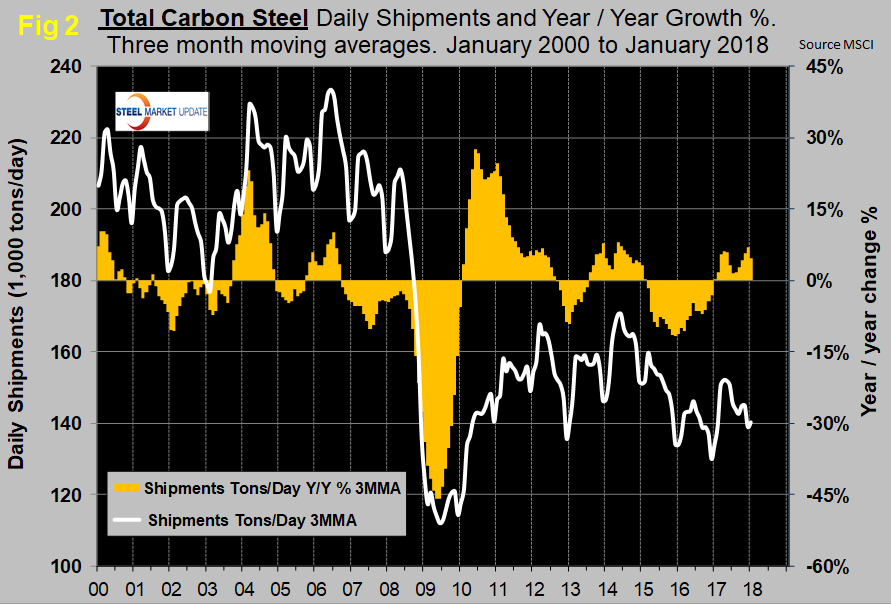

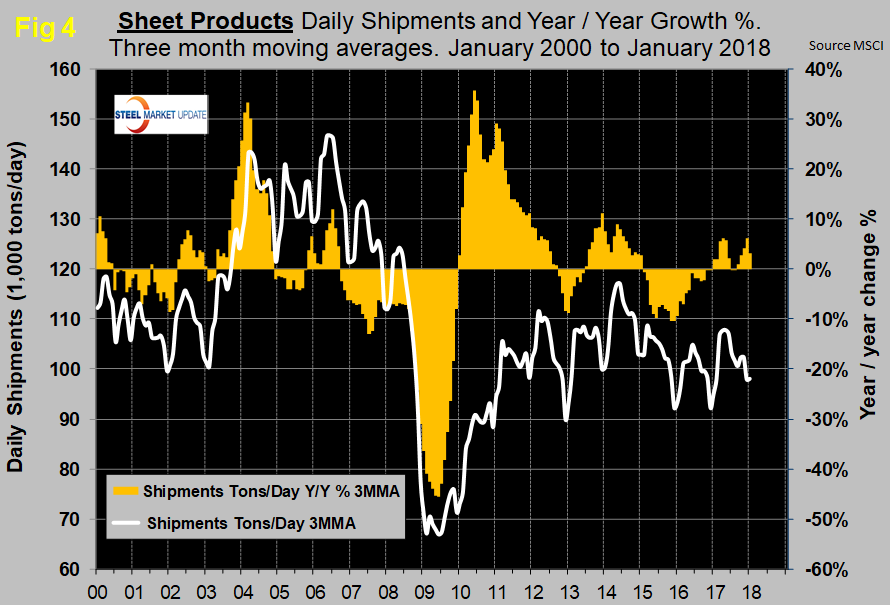

Figure 2 shows the long-term trend of daily carbon steel shipments since 2000 as three-month moving averages (3MMA). The quickest way to size up the market is the brown bars in Figures 2-6, which show the percentage year-over-year change in shipments by product. In January 2017 on a 3MMA basis, year-over-year growth was 0.07 percent, which improved to 4.6 percent in January 2018. These are the first positive year-over-year results since February 2015.

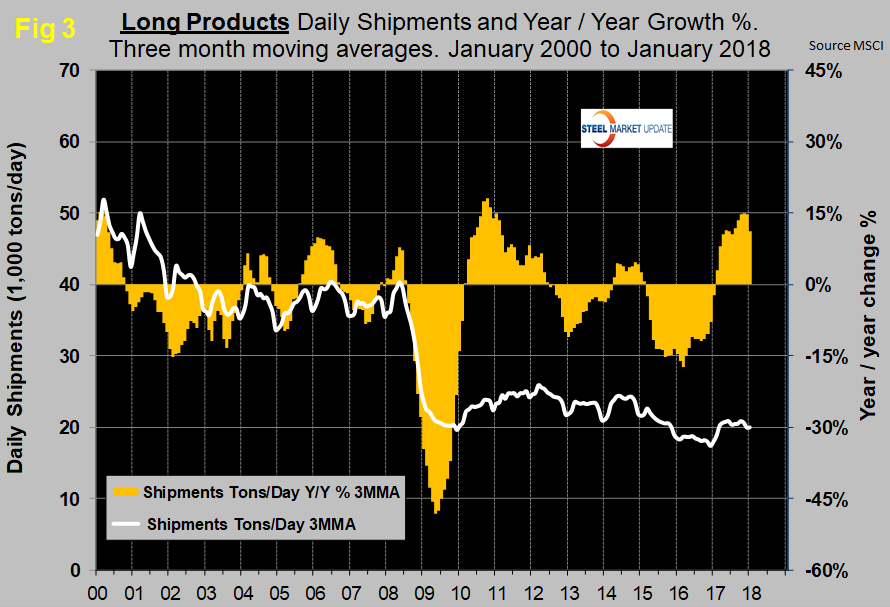

Figure 3 shows monthly long product shipments from service centers as a 3MMA with year-over-year change. Growth has improved throughout 2017 and is now the highest it has been since late 2010. The 10 months through December all exceeded a 10 percent year-over-year growth rate on a 3MMA basis, but with the release of the latest data growth slowed to 5 percent for January 2018.

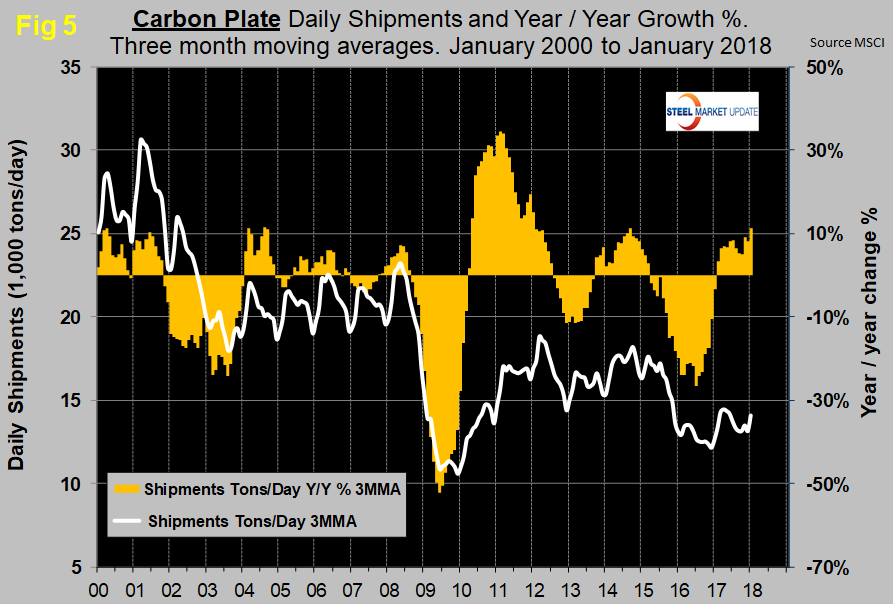

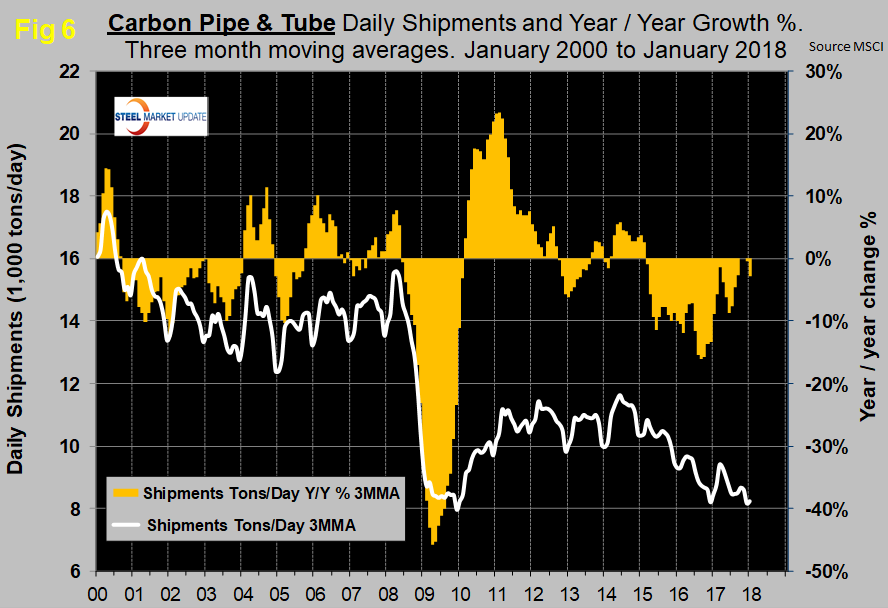

Figures 4, 5 and 6 show the 3MMA of daily shipments and the year-over-year growth for sheet, plate and tubular goods, respectively. Plate performed much worse than sheet in 2016 and 2017. In 2017, plate began to close the gap. Pipe and tube have performed very poorly since early 2015, which coincided with the decline in rig count. The rig count has doubled from where it was this time last year, but so far this has not translated into year-over-year shipment growth of pipe and tube from service centers.

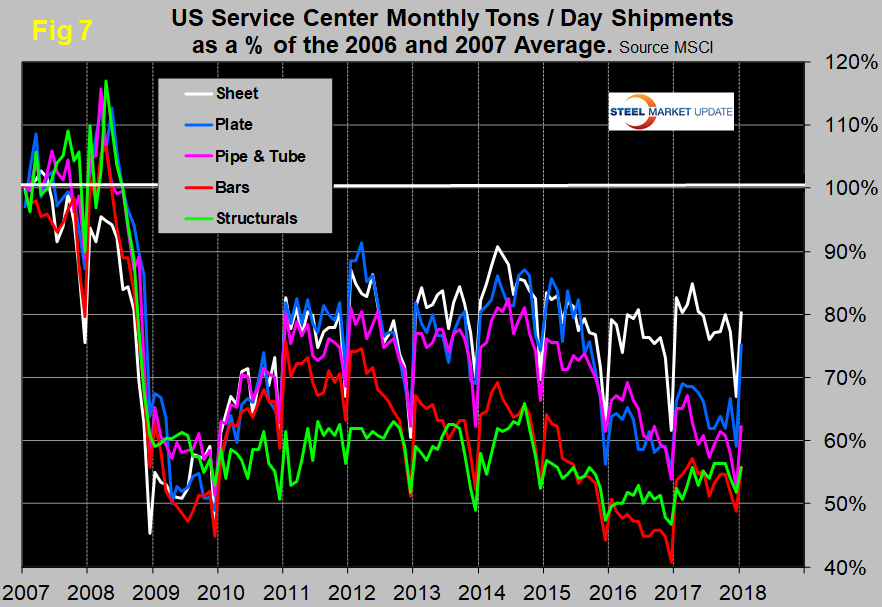

In 2006 and 2007, the mills and service centers were operating at maximum capacity. Figure 7 takes the monthly shipments by product and indexes them to the average for 2006 and 2007 to measure the extent to which shipments of each product have recovered. Each year, all products experience the December collapse and January pickup. In January, the total of carbon steel products was 71.1 percent of the average monthly shipping rate that occurred in 2006 and 2007. Structurals were 55.8 percent and bar was 55.7 percent. Sheet was at 80.3 percent, plate at 75.2 percent and tubulars at 62.2 percent.

Inventories

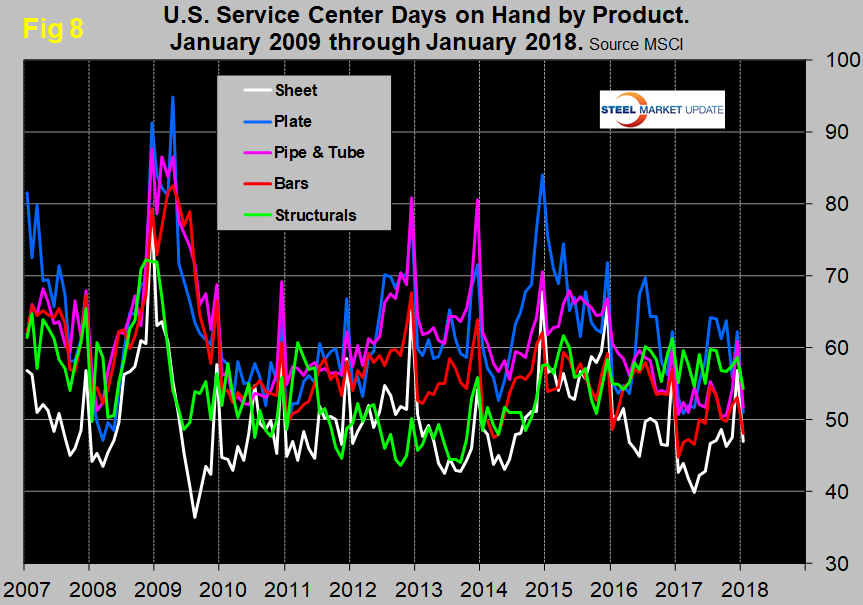

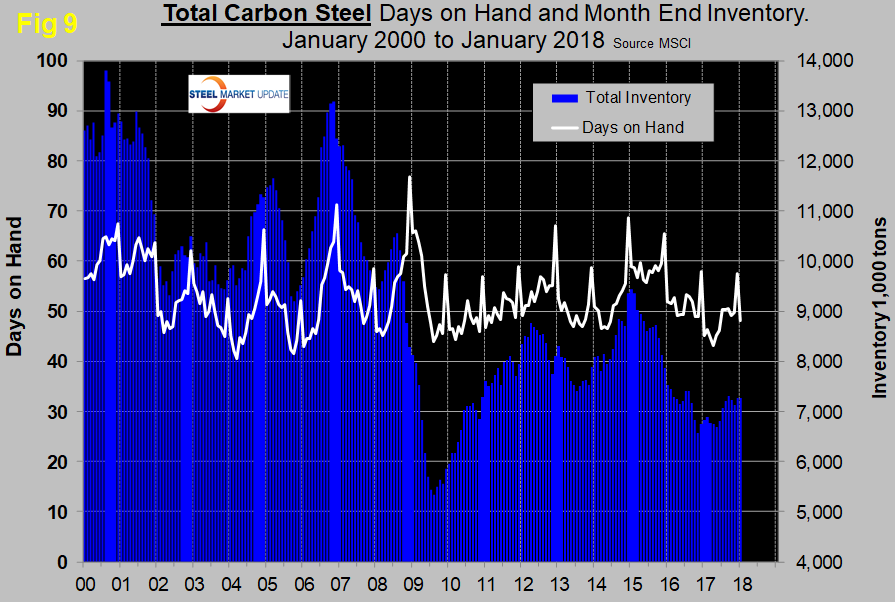

March closed with months on hand (MoH) of 1.94 for all carbon steel products, which was the lowest level in 13 years, since August 2004. This anomaly partly resulted from 23 shipping days in March, which is the maximum that ever occurs, and this fluctuation can skew the interpretation of data. We have now removed that effect as described in the notes below. Compared to the end of January last year, total carbon steel inventories were up from 45.1 to 48.2 days on hand (DoH). On a tonnage basis, total carbon steel inventories at the end of January were up by 6.5 percent year over year, but down by 3.4 percent compared to the end of January 2016. Compared to January 2017, all products except tubular goods had an inventory tonnage increase. Figure 8 shows the DoH by product monthly since January 2007. Figure 9 shows both the month-end inventory and days on hand since January 2007 for total sheet products. In the last three years, both the year-end spikes and the mid-year troughs of sheet inventory tonnage have been declining.

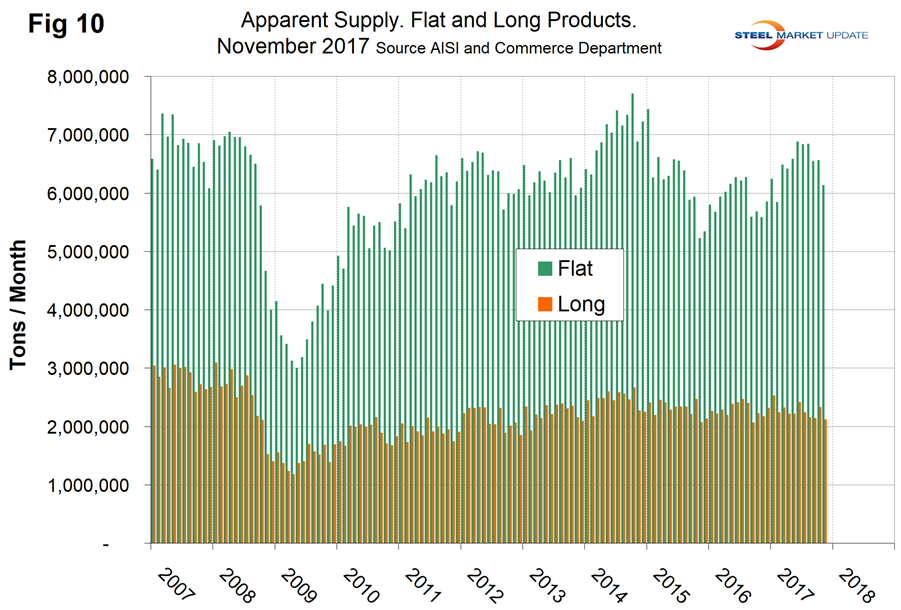

SMU Comment: In Figures 2-6, the white lines show tons-per-day shipments on a 3MMA basis. In the first few months of 2017, there was the normal seasonal increase in total shipments as January moved out of the rolling-three-month picture. However, there has been a big difference between products. Long products have enjoyed double-digit growth in the last 10 months, but at the other extreme tubulars have not had a positive month since February 2015. Plate grew strongly last year and has performed much more robustly than sheet, which had slightly negative year-over-year growth in January 2018. These observations don’t jibe with our analysis of AISI and Commerce Department data. Figure 10 shows the total supply to the market of long and flat products based on AISI shipment and import data through November, which is the latest data available.

Total supply of long products has gone nowhere since mid-2014, in contrast to the recent double-digit growth at the service center level. This suggests that the service center share has increased in 2017. Flat rolled products, on the other hand, were down in September through November, but even so have had a growth surge in total supply to the market for the last 12 months. At the service center level, sheet products didn’t do much in 2017, though plate with its much smaller volume fared better. There is also a discrepancy between total supply to the market and service center shipments of tubular goods. The total supply of tubulars is up sharply this year, according to AISI and the Commerce Department, but service center year-over-year shipments have been in decline since February 2015.

Notes: In this analysis, we began to report days on hand for the first time in August 2017. All previous SMU updates reported months on hand. The problem with MoH is that it is influenced by the number of shipping days, therefore another variable is introduced. In months with a high number of shipping days, monthly shipments are elevated, which reduces the numerical value of inventory divided by shipments. In months with few shipping days, the reverse is the case. This is a big deal because shipping days can be as low as 18 and as high as 23. This variable is eliminated by considering inventory divided by daily shipments.

The SMU database contains many more product-specific charts than can be shown in this brief review. For each product, we have 10-year charts for shipments, intake, inventory tonnage and months on hand, available on request.