Overseas

March 29, 2018

Foreign vs. Domestic HR Price Spread Rising

Written by Brett Linton

The following calculation is used by Steel Market Update to identify the theoretical spread between foreign hot rolled steel import prices (delivered to USA ports) and domestic (USA) hot rolled coil prices (FOB Domestic mills). We want our readers to be aware that this is only a “theoretical” calculation as freight costs, trader margin and other costs can fluctuate, ultimately influencing the true market spread.

Our primary numbers for this analysis are from Platts as we compare European HRC export pricing (FOB Ruhr), Turkey HRC export pricing (FOB Turkey) and Chinese HRC export pricing (FOB Chinese port). Be aware that Chinese hot rolled pricing is not available to the U.S. market, so the Chinese spread is nothing more than an exercise in “what if.” SteelBenchmarker is the secondary data provider of foreign hot rolled coil prices and is noted further down in this article.

![]() SMU adds $90 per ton to these foreign prices taking into consideration freight costs, handling, trader margin, etc. This provides an approximate “CIF U.S. ports price” that can then be compared against the SMU U.S. hot rolled price average (FOB Mill), with the result being the spread (difference) between domestic and foreign hot rolled prices. As the price spread narrows, the competitiveness of imported steel into the United States is reduced. If the spread widens, then foreign steel becomes more attractive to U.S. flat rolled steel buyers. A positive spread means U.S. prices are higher than foreign prices, while a negative spread means U.S. prices are less than foreign prices.

SMU adds $90 per ton to these foreign prices taking into consideration freight costs, handling, trader margin, etc. This provides an approximate “CIF U.S. ports price” that can then be compared against the SMU U.S. hot rolled price average (FOB Mill), with the result being the spread (difference) between domestic and foreign hot rolled prices. As the price spread narrows, the competitiveness of imported steel into the United States is reduced. If the spread widens, then foreign steel becomes more attractive to U.S. flat rolled steel buyers. A positive spread means U.S. prices are higher than foreign prices, while a negative spread means U.S. prices are less than foreign prices.

As of Thursday, March 29, Platts’ published European HRC prices were at $640 per net ton FOB Ruhr, up $1 from two weeks ago. Adding in $90 per ton for import costs, that puts the price at $730 per net ton from Europe delivered to the U.S. The latest Steel Market Update hot rolled price average is $870 per ton for domestic steel, up $30 from two weeks ago. That makes the price difference between European and U.S. HR prices soar from +$111 two weeks ago to +$140 per ton today. That means domestic HR is now theoretically $140 per ton more expensive than importing HR steel from Europe. Six weeks ago, the prices were only $8 apart, and in late 2017 we saw the opposite where domestic steel was cheaper than European imports.

Chinese HRC prices were reported at $517 per net ton, down $21 from two weeks ago. Adding $90 in estimated import costs puts Chinese HRC prices at $607 per ton delivered (if Chinese mills were able to ship to the United States, which they are not). The spread between the Chinese and U.S. HR price is now +$263, up from +$212 two weeks ago. So, if Chinese mills were able to ship HR to the U.S., it would theoretically cost $263 per ton less than buying domestic steel. This price difference has been increasing since September 2017, back when the spread was negative (meaning domestic HR would have been cheaper than Chinese imports).

Platts published Turkish export prices at $601 per net ton FOB Turkish port, unchanged from two weeks ago. Adding $90 in import costs, the Turkish HRC “to the U.S. ports” price is $691 per ton. This moves the spread between the Turkish and U.S. HR price from +$149 per ton two weeks ago to +$179 per ton today, meaning HR from the U.S. is theoretically $179 per ton more expensive than steel imported from Turkey. The Turkey/U.S. price spread has increased week by week since September/October 2017 when it dropped down to -$36 per ton (meaning domestic HR was $36 per ton cheaper than importing Turkish HR).

Freight is an important part of the final determination on whether to import foreign steel or buy from a domestic mill supplier. Domestic prices are referenced as FOB the producing mill, while foreign prices are FOB the Port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight, from either a domestic mill or from the port, can dramatically impact the competitiveness of both domestic and foreign steel. When considering lead times, a buyer must take into consideration the momentum of pricing both domestically and in the world markets. If U.S. prices are rising, which they are at this time, thus the shrinkage in the spreads, then one must consider when the steel is to be delivered versus what is available at a firm price from foreign sources. In most circumstances (but not all), domestic steel will deliver faster than foreign steel ordered on the same day.

Below is a graph comparing the Platts foreign HR export prices against the SMU domestic HR average price. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance with either logging in or navigating the website, please contact us at 800-432-3475 or info@SteelMarketUpdate.com

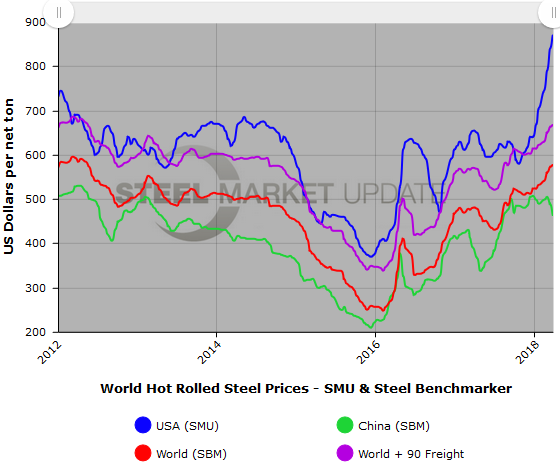

SteelBenchmarker World Export Price

The SteelBenchmarker world export price for hot rolled bands is $578 per net ton FOB the port of export, according to data released by SteelBenchmarker on Monday, March 26. This is up $6 per ton from two weeks ago. Adding in $90 in estimated import costs, that puts prices around $668 per ton delivered to the U.S. As previously mentioned, the Steel Market Update hot rolled price average this week is $870 per ton.

Therefore, the theoretical spread between the SteelBenchmarker world HR export price and the SMU HR price is +$202 per ton, up from +$178 two weeks ago, meaning imported HR is theoretically now $202 per ton cheaper than steel purchased domestically. To put this into perspective, the record high in our seven-year history was +$210 on June 27, 2016.

The latest price spread is $90-110 per ton higher than the average spread seen over the last few months. In late October 2017, the spread was the lowest seen in 2017 at -$27 per ton. This time last year the spread was +$84 per ton, and remained around that through July. The record high in our seven-year history was +$210 on June 27, 2016 (meaning domestic steel was theoretically $210 per ton more expensive than foreign steel), while the record low was -$70 in August 2011. The average spread for 2018 so far is +$129 per ton, while the average spread for 2017 was +$48 per ton.

We want to again remind our readers that the calculations shown above are “theoretical,” but in most markets are probably a good indicator of where you can expect to find offers being made.

Below is a graph comparing SteelBenchmarker world HR export prices against the SMU domestic HR average price. We also have included a line with the world price including freight and traders’ costs, which gives you a better indication of the true price spread. You will need to view the graph on our website to use its interactive features; you can do so by clicking here.