Prices

April 5, 2018

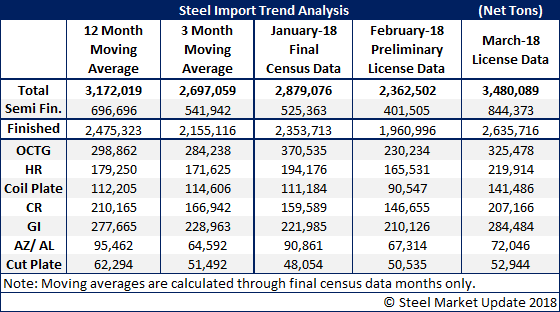

March Steel Imports Near 3.5 Million Tons

Written by John Packard

Earlier this week, the U.S. Department of Commerce released steel import license data for the months of February and March 2018. There is a considerable difference between the two months, which SMU believes is partially due to the March 23 deadline before Section 232 tariffs went into effect.

February license data suggests the month will come in around 2.3 million net tons, while March is trending closer to 3.5 million net tons.

Semi-finished steels (which are mostly slabs used by the domestic steel mills) were well above their 12-month and 3-month moving averages. At 844,000 net tons, they were more than double February’s 401,000 net tons.

Finished imports for March were, again, well above the 12-month and 3-month moving averages. The 2.6 million tons will be about 700,000 tons higher than what we are seeing in the February numbers.

Virtually every product followed by SMU was above its 12-month and 3-month moving averages and significantly higher than what we saw for February 2018.