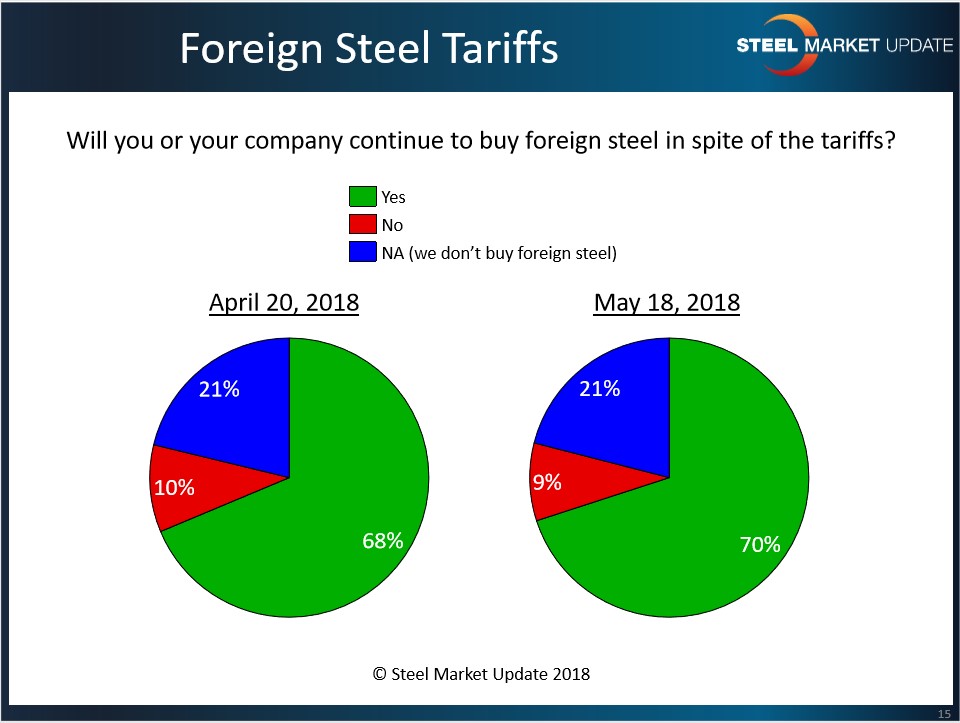

Market Data

May 22, 2018

SMU Q&A: No Signs of a Price ‘Breakout’ Either Way

Written by Tim Triplett

Steel Market Update canvassed the market on May 22 to gather steel executives’ views on supply, demand and pricing in the current environment. Some also shared their thoughts on their biggest challenges today. Below are some of their more insightful comments:

Q: Are you seeing any signs that steel prices are going to “break out” in one direction or the other in the coming weeks?

A: “We have seen relatively stable flat rolled and plate spot prices over the past month.”

A: “Plate pricing hasn’t moved much in the past 60 days. The USA plate mills continue to quote me the same landed number for late March, April and May.”

A: “I do not currently see any ‘breakout’ signs, but most of the risk appears to the upside moving ahead.”

A: “I see steady demand in the U.S. with less imports. To me, that means tighter supply and higher pricing.”

A: “Like most, our current view is clear as mud. We do feel there are more signs pointing to the market going up than down, and have been actively engaging our customers in that discussion, as well. Having said that, we are aware of how fast things tend to change in steel.”

A: “I think we have a bifurcation in market views. We see some service centers reselling lower in the perception of a historical summer slowdown coming. The mills, however, are filling up nicely. I do not think the mills blink. They are into August, and they are talking up $40/ton. My call, no breakouts either direction, solid and pretty steady.”

A: “HR continues to be the strongest of all flat-rolled products. Availability is tight and there is little room to negotiate with the mills. Even though CR and coated are not as strong, the domestic mills still do not want to negotiate much. It’s almost like they do not want to trigger an avalanche.”

A: “Once again, the unknowns regarding trade have this market frozen. I see more upside pressure on pricing than lower. Energy is a big factor for demand right now for HR and plate. If tariffs, quotas or circumvention somehow limit pipe and OCTG imports into the U.S., I think we will see $940 HR by September.”

A: “There are no signs of a breakout other than my instincts telling me it’s coming. Lack of imports will bring a lot of buyers back to the domestics.”

A: “Supply will remain tight and pricing levels will stay high. I expect some price correction before year’s end, but do not expect a crash.”

A: “Steel pricing has been stable for the last three weeks. I met with a vendor yesterday and there’s no sign of another uptick. As of now. Nucor has always waited until the end of the week for any changes. We hope not.”

A: “Most U.S. customers are waiting to book new business until after a final decision is made regarding the tariff situation related to Section 232 between the EU and the U.S. Customers in the EU are expecting prices to fall as the anticipated flood of import material is starting to occur, and this has resulted in a slowdown of new business with the European mills. However, HR mills in Europe at the moment aren’t showing signs of decreased pricing, yet.”

A: “I think mills are seeing buying starting to come in below the max levels of programs. That is easing supply, and demand will be seasonally slower. So, there should be some slight downward pressure on prices. But with full results of Section 232 yet unknown, mills do not seem to be chasing business even though there is more availability. When adding in the potential of Section 232, I think the net price risk is to the upside. If more extensions are granted, or the results of exclusions become clear and favor consumers, the risk quickly shifts back to lower prices.”

A: “Steel prices are stable now with a slight downward bend through November…. Our industry is one of over corrections. We clearly have overcorrected on the height of the current price cycle, and it will be damaging on the downward correction. The downward corrections are normally a lot longer than the ‘up”’markets.”

A: “If hard quotas are instituted, I think this brings a different dynamic than a straight tariff. I think the mills were about at the end of their runway on pricing with the implementation of tariffs. With quotas, it could give them more leeway to move prices higher or maintain current levels. Prior to the quota conversation, I was thinking pricing might pull back starting in Q3. Not so sure about that now.”

Q: Accidents at two steel mills are creating some production issues along with maintenance outages that are planned for this summer. What concerns do you have regarding the availability of steel through the third quarter?

A: “Hot rolled could get very tight.”

A: “These issues should help hold the market firm along with foreign slab issues at NLMK, the sale of CSN, etc.”

A: “We are not worried about availability, but are aware of possible tightening, especially when it comes to HR. If steel flow tightens up, it would be an opportunity for our business.”

A: “I believe HR availability will become a real concern in the third quarter and possibly beyond. The energy demand spike is putting real pressure on the HR and plate markets, and it looks to worsen in the months ahead. HR imports were already anemic prior to Section 232, and will drop even further. Expected outcomes for Section 232 point toward more restrictions on OCTG imports, so domestic mills will maximize production of this HR product given its profitability. Users will not be able to satisfy their needs between domestic OCTG and product from ‘quota”’countries, and will be forced to buy OCTG tons with a 25 percent tariff attached”

A: “The mills are way behind, which has put a crunch on a select number of sizes. We need to manage our demand side closely to make sure we don’t develop any holes in our inventory.”

Q: What risks do you see associated with the buying of foreign steel for future delivery?

A:“Lead times are long, and prices are near a 10-year high. A bad combination.”

A: “I have foreign steel on order now that is late coming in from a steel vendor. This creates spot buys that are more expensive.”

A: “We normally buy import for most of our supply but today we’re not. We think the market could go either direction, and we don’t want the risk. We’d rather run out than get caught.”

A: “Changes in policy can turn this market very quickly as we have seen the last couple of years. How do you predict the price of steel six months from now, which is when you would get your steel, when everything can change with the next Tweet?”

A: “With the quota model seeming to be the path the administration wants to go down, it raises concern about longer-term availability from foreign sources.”

A: “Price fluctuation is a big concern. There is a lot of uncertainty due to the temporary exemptions on major countries. If the exemptions are made permanent with some quotas, prices may fall a bit, and if you book imports today you may lose big time. However, for some products, you have to keep on importing.”

A: “Other than unknown outcomes of Section 232, I see no risk in buying foreign. Soon, there will be well known ‘rules of the road’ and buyers/sellers will begin to position themselves for the months ahead. This may take a few months until we get more clarity.”

A: “There is little risk, depending on the exporting country and trader, if the Section 232 duty is already included in the price. However, if the EU is somehow restricted by a quota or even perhaps Canada, all bets are off.”

Q: What are the most serious challenges facing the steel industry and your company/customers through the balance 2018?

A: “Finding the right balance between demand and supply.”

A: “Adapting to the new inflated cost levels. This will become more apparent as current contracts come to a conclusion and more of the new pricing surfaces in the new contracts.”

A: “Sustained high prices are reducing margins and raising manufacturing costs.”

A: “Trying to guess what the administration will do next. It’s hard to run a business when the rules change weekly.”

A: “Our challenge is price. Our OEM customers are placing orders with fab and machine shops in Mexico, Vietnam, Korea and China. Using today’s plate pricing, our quotes are 20 to 30 percent high.”

A: “Supply is going to be a lot tighter than anyone imagines with the only relief being seasonality.”

A: “Uncertainty makes it difficult to plan, but also creates opportunities. Being able to balance inventory positions (both cost and volume) are obviously crucial going forward.”

A: “Large projects being put on hold because of the higher steel costs combined with U.S. manufacturing being unable to export because of tariffs being placed on U.S. products.”

A: “For the mills, the biggest challenge in the near term is losing government support for all of their trade schemes, which seems unlikely. U.S. Steel and AM have their labor contracts coming up, but I really don’t see either the companies or the union stopping production. And, they might need better tax lawyers to figure out how to handle the enormous profits! For the rest of us – distributors, OEMs, fabricators, etc., the BIGGEST risk is offshoring of any and all configurations of blanks, parts, weldments, assemblies, etc. As the reality of sustained, embedded higher prices for steel in the U.S. sinks in, it will force companies to at least consider outsourcing. In the end, I expect the loss of a portion of this manufacturing to occur.”

A: “It feels like we are working our way through the summer doldrums right now. There’s some spotty mill discounting, but not a lot. Demand is still healthy, and energy could even find a higher gear in H2. I am looking to see imports drop appreciably and outages to restrict existing domestic supply. I see overall demand as constant and supply as the wild card. Do lower imports and mill outages exceed added domestic capacity, or do we have excess supply? If supply grows and spot prices drop relative to indexes and contracts, contract participation will drop, and mills will have more spot to sell. I see that scenario as one of the greatest threats. More spot typically means lower prices, and we spiral downwards. If supply stays tight, then we will have a strong and steady market well into or through Q3.”

A: “I am concerned there has been some demand pull-ahead that will show up in softer economic numbers later this year. With long lead times on some products, buyers have been forced to speculate much further than normal and this could create a glut of inventory down the road, especially if economic growth starts to decelerate. Many economic indicators are pointing to somewhat of slowdown later this year and into 2019.”

A: “On one hand, we don’t care for the mix of tariffs and quota agreements. The process is simply bait for catching bigger fish that we are paying a steep price for on the OEM level. On the other hand, as much as we dislike the tariffs, they are in fact tangible and allow us to take something to our customer that they can see and touch. Quotas are not tangible as they relate to market pricing. In fact, any effect from a quota on market pricing will only be seen through indices in arrears, meaning we’ll already be squeezed on margin before the index moves to support our customer pricing position. As much as we dislike tariffs, we dislike quotas even more. Tariffs regulate trade, but quotas actually restrict trade, and whether you embrace the concept of either free or fair trade, the implications of actually restricting trade are egregious and draconian.”

A: “We continue to be concerned over the precedence established by the Chinese circumvention case in Vietnam. There were extenuating circumstances in the China/Vietnam situation relating to the nonmarket economy status of the two countries, which ultimately allowed cost dynamics to be introduced that heretofore were not allowed, so it is possible that implications from the case will not be as far reaching as they appear. On the other hand, the outcome of the case rewrote many years of established trade law in the process, so there is no telling what lengths this administration is willing to go to in the process of MAGA.”

A: “I don’t expect much relief between now and then on the Section 232 exclusions and exemptions. Inventory is trending down, and not many are restocking at these price levels. Product substitutions from alternative products are aggressively and permanently eroding the steel business. Mills are not developing and supporting new markets for steel. Mill support of the tariffs is highly damaging to U.S. manufacturing.”

A: “As long as prices stay where they are or go slightly down, we’re going to have a very good year. Not a lot of concern here as we continue to successfully lower inventory, thereby taking off risk.”

A: “One word: clarity. There is no greater challenge than attempting to feel your way around while blindfolded in the dark and have a bullhorn blasting in your ear from every self-serving media outlet in the world (save for a select few, like SMU, of course).”