Prices

July 12, 2018

May Steel Exports Down 15 Percent Over One Year Ago

Written by Brett Linton

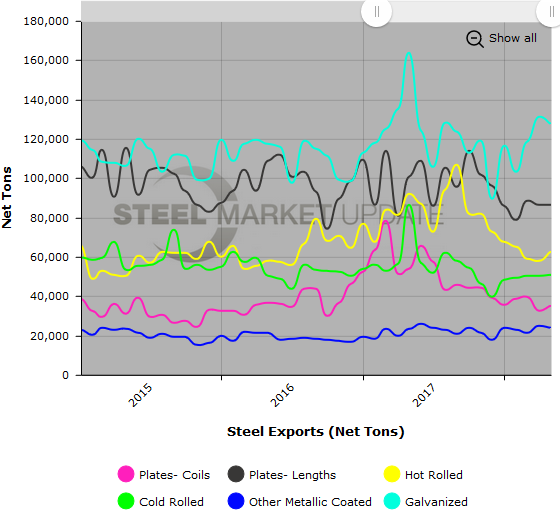

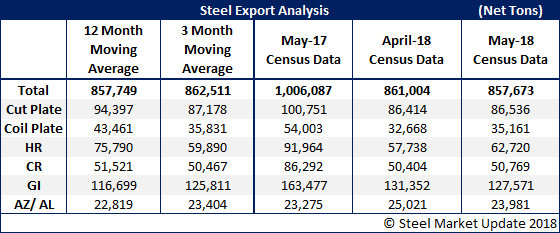

U.S. steel exports in May 2018 totaled 857,673 net tons (778,069 metric tons), flat over April but down 14.8 percent from May 2017 (which was at a 30-month high). Total exports have averaged around 860,000 tons the last few months. The total May export figure is a few thousand tons below the three-month moving average (average of March 2018, April 2018 and May 2018), and just a hair below the 12-month moving average (average of June 2017 through May 2018). Here is a breakdown of flat rolled and plate steel exports:

Cut plate exports increased 0.1 percent from April to 86,536 tons, down 14.1 percent compared to levels one year ago.

Exports of coiled plate were 35,161 tons in May, up 7.6 percent month over month, but down 34.9 percent year over year.

Hot rolled steel exports rose 8.6 percent month over month to 62,720 tons, but were down 31.8 percent from May 2017 levels.

Exports of cold rolled products were 50,769 tons in May, up 0.7 percent from April, but down 41.2 percent over the same month last year. This is the highest level seen since October 2017 when 54,398 tons were exported.

Galvanized exports fell 2.9 percent month over month to 127,571 tons. Compared to one year ago, May levels were down 22.0 percent.

Exports of all other metallic coated products came in at 23,981 tons, a 4.2 percent decrease from April, but a 3.0 percent increase compared to one year ago.

To see an interactive graphic of our steel imports history through final May data (example below), visit our website here. If you need any assistance logging in or navigating the site, contact us at info@SteelMarketUpdate.com or 800-432-3475.