Overseas

July 15, 2018

Another Look at Foreign vs. Domestic Hot Rolled Prices

Written by Brett Linton

The following calculation is used by Steel Market Update to identify the theoretical spread between foreign hot rolled steel import prices (delivered to USA ports) and domestic hot rolled coil prices (FOB Domestic mills). We want our readers to be aware that this is only a “theoretical” calculation as freight costs, trader margin and other costs can fluctuate, ultimately influencing the true market spread. We do not include the 25 percent tariff or any other unusual costs to the calculations we provide.

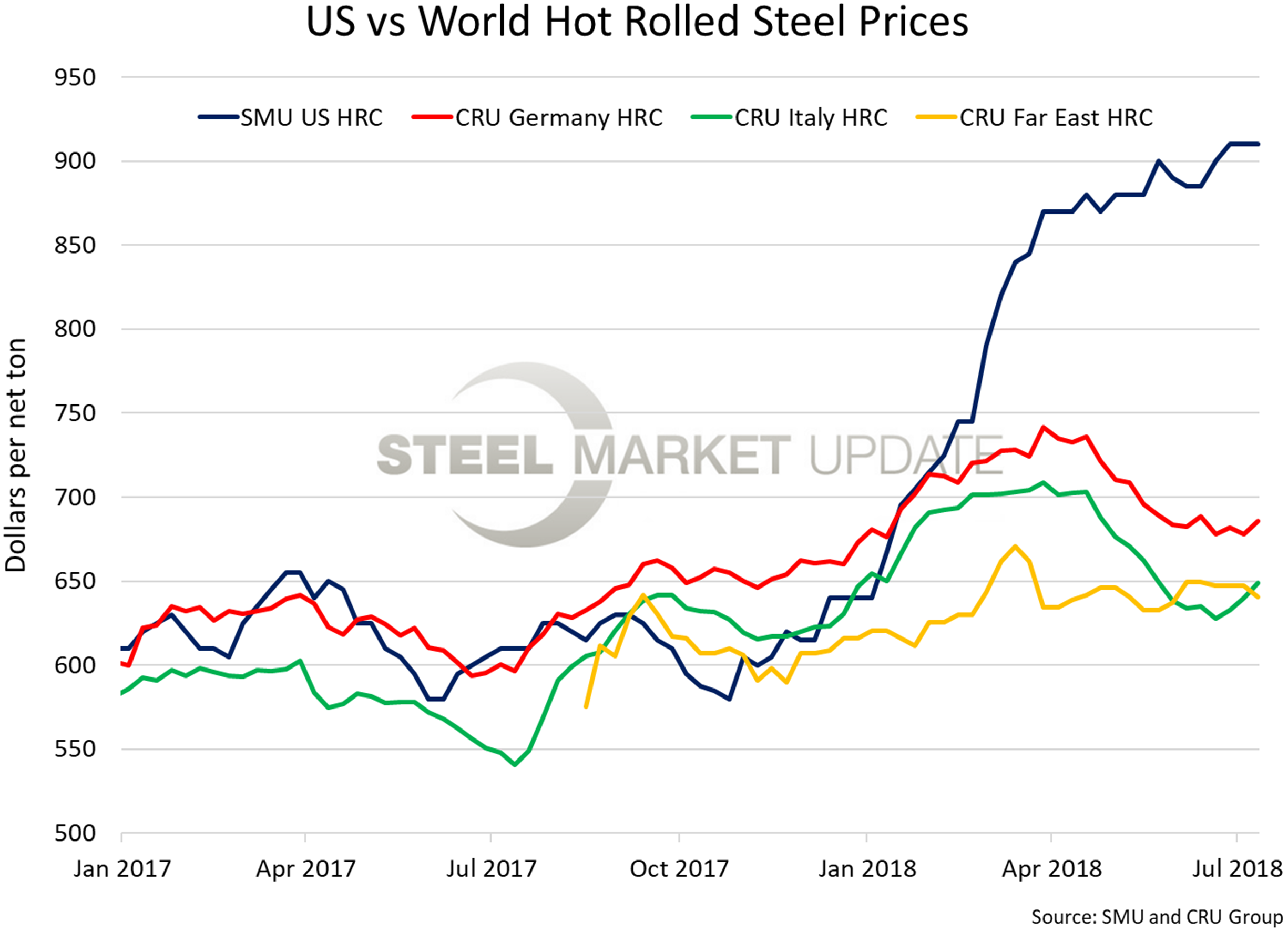

We are now comparing the SMU U.S. hot rolled index to CRU price indices for Germany, Italy and the Far East (East and Southeast Asian port).

![]() SMU adds $90 per ton to these foreign prices taking into consideration freight costs, handling, trader margin, etc. This provides an approximate “CIF U.S. ports price” that can then be compared against the SMU U.S. hot rolled price, with the result being the spread (difference) between domestic and foreign hot rolled prices. As the price spread narrows, the competitiveness of imported steel into the United States is reduced. If the spread widens, then foreign steel becomes more attractive to U.S. flat rolled steel buyers. A positive spread means U.S. prices are higher than foreign prices, while a negative spread means U.S. prices are less than foreign prices. PLEASE NOTE: HRC prices are being affected by 25 percent tariffs, which brings new offers well above $800 per ton from the limited number of suppliers even quoting HRC.

SMU adds $90 per ton to these foreign prices taking into consideration freight costs, handling, trader margin, etc. This provides an approximate “CIF U.S. ports price” that can then be compared against the SMU U.S. hot rolled price, with the result being the spread (difference) between domestic and foreign hot rolled prices. As the price spread narrows, the competitiveness of imported steel into the United States is reduced. If the spread widens, then foreign steel becomes more attractive to U.S. flat rolled steel buyers. A positive spread means U.S. prices are higher than foreign prices, while a negative spread means U.S. prices are less than foreign prices. PLEASE NOTE: HRC prices are being affected by 25 percent tariffs, which brings new offers well above $800 per ton from the limited number of suppliers even quoting HRC.

As of Wednesday, July 11, the CRU German HRC price was $596 per net ton, up $8 from the previous week. Adding $90 per ton for import costs, that puts the price at $686 per ton from Germany delivered to the U.S. The latest Steel Market Update hot rolled price average is $910 per ton for domestic steel, unchanged from last week. The spread between German and U.S. HR prices is now +$224 per ton, down from +$232 last week, and down from +$228 two weeks ago. That means domestic HR is now theoretically $224 per ton more expensive than importing HR steel from Germany. Prior to this week, the spread had risen consecutively for the previous three weeks. The four-week average price spread is now +$227 per ton, up from +$220 last week.

CRU published Italian HRC prices up $9 over last week to $559 per net ton. After adding import costs, we get a delivered price of approximatley $649 per ton. The spread between the Italy and U.S. figure is +$261 per ton, down from +$270 one week ago and +$277 two weeks ago. Meaning that U.S. HR is theoretically $261 per ton more expensive than importing steel from Italy. The four-week average is now +$270, up from +$267 last week.

The CRU Far East HRC price fell $6 to $551 per net ton. Adding import costs, that puts the price at $641 per ton. The spread between the Far East and U.S. figure is +$269 per ton, up from $263 last week and the week before that. That means domestic HR would theoretically be $269 per ton more expensive than importing steel from E or SE Asia. This is the fifth consecutive week that the spread has remained steady or risen. The four-week average price spread is now +$262 per ton, up from +$254 last week.

Freight is an important part of the final determination on whether to import foreign steel or buy from a domestic mill supplier. Domestic prices are referenced as FOB the producing mill, while foreign prices are FOB the Port (Houston, NOLA, Savannah, Los Angeles, Camden, etc.). Inland freight, from either a domestic mill or from the port, can dramatically impact the competitiveness of both domestic and foreign steel. When considering lead times, a buyer must take into consideration the momentum of pricing both domestically and in the world markets. In most circumstances (but not all), domestic steel will deliver faster than foreign steel ordered on the same day.

The graphic below shows all four price indices above. We plan to soon turn this into an interactive graphic and add a webpage in the ‘Steel Prices’ section of our website.