Market Data

August 19, 2018

CRU: U.S. Tariffs Will Drive Greater Turkish Steel Exports

Written by Tim Triplett

Editor’s note: The following was contributed by analysts at the CRU Group.

The Turkish-U.S. political relationship has soured sharply in the past week. U.S. President Donald Trump tweeted relations were “not so good” on Friday, Aug. 10, and doubled tariffs on U.S. imports of Turkish steel. Turkish President Erdogan responded with anger, suggesting the country will forge new alliances and impose tariffs of its own on Turkey’s imports of various good from the U.S. This escalation in tensions between the two countries has investors worried about Turkey’s economic outlook and many are retreating to safety. Following the tweet, the lira dropped to a low of 7.0 against the U.S. dollar before recovering to around 6.0 by Friday.

With Turkey’s future much less certain, we look at several scenarios from an unlikely quick return to business-as-usual to a full-blown multi-year economic crisis. While the U.S. tariffs will affect Turkey’s steel exports, the bigger issue is the potential reduction in domestic steel demand. The weakness of the lira is exacerbating existing issues of high debt levels in the country and confidence its economic management has been undermined.

In the event of rapid recovery, Turkish trading activity may be reduced while market participants digest the situation before a clearer outcome emerges and investor confidence is renewed. Here, although steel export demand in the U.S. will be largely disrupted, domestic steel demand remains firm. In a more dramatic outcome, the Turkish economy dives into a recession, investment drops and steel demand tanks as a result. In all scenarios, Turkey’s exports to the EU remain constrained by the safeguard measures there, which act as an additional pressure point on Turkish steel mills.

In sum, at this stage, the Turkish economy is set to slow down sharply, as the plunge in the Turkish lira will push inflation above 20 percent, on top of a further deterioration in the relationship with the U.S. Unless the government decides to implement crisis measures, including a sharp increase in interest rates and a tightening of fiscal policy, the possibility of a recession in the coming months is not completely off the table. In this case, a drop in Turkish domestic steel demand will ensue, and mills will either need to reduce utilization of steel facilities or seek additional export volumes. Therefore, paradoxically, U.S. steel import tariffs on Turkey could increase the threat of greater export volumes in the near future before Turkish mills are forced to reduce production due to high costs. The additional export volume diverted from the U.S. is likely to go to the EU, though the EU may further tighten safeguard measures.

The Turkish economy is vulnerable to an economic crisis. The escalating in tensions between Turkey and the U.S. has unnerved investors, leading them to pull assets to a safe haven, such as the U.S. While the lira has been depreciating for some time, Trump’s tweet on Friday resulted in a further 16 percent depreciation of the lira against the U.S. dollar in the days that followed. A weakened lira means challenges for domestic business, and individuals who have foreign debt but receive earnings in lira would face higher debt repayment and higher operating costs, leading to an increase in non-performing loans. Turkey’s foreign debt is as high as 53 percent of GDP, of which 60 percent is in the private sector. Steel-consuming sector construction, manufacturing and real estate are highly exposed to foreign debt. The combination of high inflation of 15 percent and relatively low interest rates, albeit at over 17 percent, have not helped investor confidence. As private investors’ confidence falls, planned investments will be abandoned in Turkey. Lower investment and high inflation increase the risk of non-performing loans, where banks will have more difficulties receiving debt repayment. Ultimately, this risks sharply undermining growth, with the potential for a crash.

One option for Turkey to contain the depreciation of the lira is to lift interest rates, which will tighten domestic credit conditions. President Erdogan is, however, strongly resistant to the approach because Turkey relies on cheap credit for the high growth rates it has experienced in recent years.

In addition, the tensions between Turkey and the U.S. are caused by largely intractable problems, meaning these are not likely to go away quickly. In Syria, these NATO allies ended up fighting on opposites sides, with Turkey’s allegiances more aligned with Russia’s. More recently, Turkey has kept an America pastor in detention on suspicion of espionage and terrorism. Negotiations for the pastor’s release failed in July and the U.S. responded with sanctions on two Turkish ministers. Meanwhile, Turkey has publicly opposed sanctions on Iran, and Turkey’s foreign minister has stated that the country is not obliged to implement them.

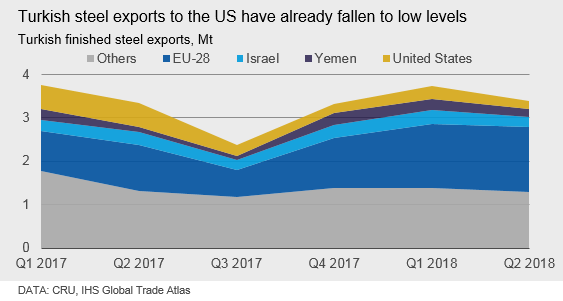

Overall, while a loss of U.S. export volumes is not great news for Turkish mills, the impact is limited. Turkish exports to the U.S. have fallen since late 2017 due to an initial duty of 8 percent applied in mid-2017 and then because of additional tariffs due to the Section 232 investigation. For example, Turkey exported 88 kt of finished steel to the U.S. in June 2018, only 6.4 percent of its export volume and less than 3 percent of total steel production. While the U.S. represents a small portion of Turkish steel exports, Turkish steel is a large source of steel for the U.S., representing 23 percent of U.S. total finished steel imports.

In contrast to smaller export volumes to the U.S., Turkish exports to the EU have risen substantially this year. Compounding woes for Turkish steel exporters, the EU has recently implemented quota-tariff safeguard measures. These are provisional measures that run for 200 days and offer an opportunity for steel exporters to still move steel into the EU before facing a tariff of 25 percent. That said, the run rate on the quotas for steel products Turkey exports to the EU is quite high and likely to be filled before the end of this period.

As discussed, there is a high level of uncertainty ahead for Turkey and we believe there are two scenarios that outline the most likely outcomes for the Turkish economy and how this will impact steel demand. Much hinges on forward U.S. policy announcements and economic uncertainty in Turkey. A sharp reversal of the current situation, with a quick recovery of the lira and a fast return to economic growth in Turkey, seems unlikely, though there is potential for a more orderly recovery, given the right conditions. However, there is a risk the Turkish economy may collapse, and if this is the case, domestic demand will fall sharply. Paradoxically, given that the catalyst was U.S. import tariffs, this could lead to an even greater threat of steel exports from Turkey. Below we outline two potential scenarios, though we emphasize uncertainty is high:

Short-Lived Crisis—Concessions come quickly and strong economic stimulus mitigates most of the impact in the near-term: A short-lived crisis would require a sudden removal of the catalysts for the current situation Turkey faces – depreciation of the lira and undermined investor confidence. This would be a combination of Erdogan allowing interest rates to rise, which succeeds in curbing inflation, and Trump easing the pressure being applied on Turkey. These two factors would need to be enough to mean international investors regain confidence in the Turkish economy, easing the downward pressure on the value of the lira. Combined, these will act to stabilize the local economy and reinvigorate investment, albeit delayed, and provide support for domestic steel demand. In this scenario, a return to more normal growth occurs in the coming quarter.

Economic Distress—Concessions and economic stimulus contain the downturn to a year: If the U.S. gets the concessions it seeks from Turkey and the Turkish government is successful in stimulating the economy, a short period of economic distress will still likely occur, before an orderly recovery takes place over the next 6-12 months. In the meantime, however, domestic demand will suffer greatly due to reduced investment in the country, and mills will be forced to either seek greater exports or reduce utilization of capacity.

There is also the risk that the Turkish economy enters a period of significant and prolonged downturn, economically isolated from historical allies. If this occurs, there will be no signs of concession from either the U.S. or Turkey, and Turkey will be unable to sufficiently boost the confidence of investors elsewise. Investment in the country will suffer greatly and steel demand will fall as a result.

Economic Distress Likely Over the Coming Year

There are few signs currently that either side of this U.S.-Turkey political conflict is willing to concede. Turkey has responded with tariffs and threats of changing allegiances, while the U.S. has indicated that even the release of the U.S. pastor will not result in a reduction in the tariffs. Combined with the various other intractable tensions between the two countries, we do not expect concessions to be forthcoming in the short-term. More importantly, the international investor community has lost confidence in the potential for stability in Turkish politics or its economy. With these concessions, we do not believe that economic management alone will help the economy muddle through. There is still a great deal of uncertainty, though, and President Trump’s agenda has been changeable on a range of issues. Therefore, while there is a risk of a prolonged economic crisis, we believe there is potential for conditions to evolve such that the impact is contained to a year or so.

Near-term weakness is almost the only certainty. In either scenario, pressure will still mount on steel mills as delayed investment curbs steel demand in the very near-term. Meanwhile, mills will be looking for new opportunities to cover the loss of volumes in both the domestic market and exports to the U.S. The EU may be a target market until the safeguard quotas are exhausted and the tariff that applies afterwards makes shipping steel there prohibitive. Other markets, such as South East Asia, are also being targeted by Turkish steel mills. Furthermore, Turkish mills have been looking for alternative export destinations, such as one group of traders looking to time charter vessels to West Africa reducing transport costs from $100 per ton today to $30 per ton. According to customs data, we have seen an uptick in shipments to African countries for steel long products and South America for sheet products in the past few months.

Turkish mills are still expected to lower steel prices to secure volumes. These mills are largely EAF-based (i.e. about 70 percent of steel output) and dependent on scrap imports from Europe, the U.S. and the CIS. In lowering steel prices, Turkey’s mills may have to accept lower margins, unless there is a wider impact on scrap supply markets in the U.S. and Europe that turns scrap prices lower there. The European scrap price is the most likely to fall first because Turkish mills retain access there until the steel quotas are exhausted. This will dampen European mills’ appetite for greater scrap purchases and allow domestic scrap prices to soften alongside falls in scrap bids from Turkish mills.

Being dependent on scrap imports that are priced in U.S. dollars, mills need to secure higher domestic steel prices in lira to compensate for the weaker currency. This has already begun, but we do believe margins on domestic sales will also fall. Because producers are mostly EAF-based, that offers more flexibility than BOF-based operations that need to keep their blast furnaces operating on a continuous basis. Therefore, if margins fall below acceptable levels, EAF-based mills are more likely to curb steel output. This is, however, more the case for steel long products than flat products, which are mostly from BOF-based producers that are more likely to give in to lower prices to sustain production from their blast furnaces. In addition, EAF-based long producers in Turkey have more bargaining power on sourcing scrap than the BOF-based producers for bulk raw materials, because Turkish mills are relatively larger consumers of scrap than bulk raw materials compared to other international producers. Therefore, margins on Turkish steel flat products could fall more sharply than for longs. Some mills in Turkey can produce both flat and long products and therefore may divert production.

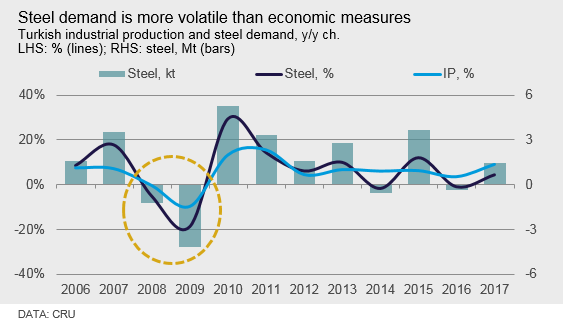

Because of the potential for economic woes to be prolonged, Turkish domestic steel demand may drop in 2019. Ultimately, this will cause more damage than restricted access to the U.S. and EU markets for steel exports. Steel demand is intrinsically linked to economic growth, in particular investment and industrial output. Turkish GDP grew by more than 7 percent year over year in 2017 and was already expected by CRU Economics to drop to around 4 percent before the current crisis developed, because we expected stimulus measures to be eased.

While we do not believe a recession is the most likely outcome at this stage, we use this as an example here to highlight the impact of even a mild contraction in economic growth. During the financial crisis in 2009, Turkish GDP contracted by 5 percent and industrial production by 9.9 percent, while domestic steel demand shrunk by 19.9 percent year over year, or 4.2 million tons. Using this period as a proxy, in the event of a recession in Turkey that resulted in GDP contracting by just 2 percent and IP by 4 percent in 2019, then steel demand is likely to shrink by 8 percent year over year. This drop in finished steel demand would mean a loss of nearly 3 million tons in demand. This means Turkish mills would either need to reduce utilization of facilities or exports would need to rise to as much as the equivalent of 7 percent of current production levels. While unlikely, if all this volume was exported, Turkish steel exports would increase by over 23 percent compared to 2018 levels. In some cases, imports may also be reduced as buyers divert purchases to local mills, though this depends entirely on how competitive Turkish mills are to imports.

The U.S. has doubled tariffs on Turkish steel imports as tensions between the two countries have escalated. While tariffs will directly impact Turkey’s steel exports, the greater impact will be on domestic steel demand as economic conditions in the country deteriorate. At this stage, we expect that much of the impact will be contained to the next year or so, though there is a risk the crisis could deepen and lead to a multi-year prolonged recession that would be much more damaging. Paradoxically, this will mean the U.S. tariffs increase the threat of Turkish steel exports as mills there look to compensate for the loss of domestic steel demand, at least in the short term, before steel production reduces. Flat rolled steel is at the greatest risk of this threat because there is more BOF-heavy steelmaking in Turkey, though at the same time Turkish mills may be able to displace imports of these products. EAF-based longs producers are likely to cut steel output more readily. This would drop demand for Turkish scrap imports and undermine scrap prices in key exporting markets, such as Europe and the U.S.