Market Data

November 1, 2018

ISM: Manufacturing Still Strong, but Slowing

Written by Sandy Williams

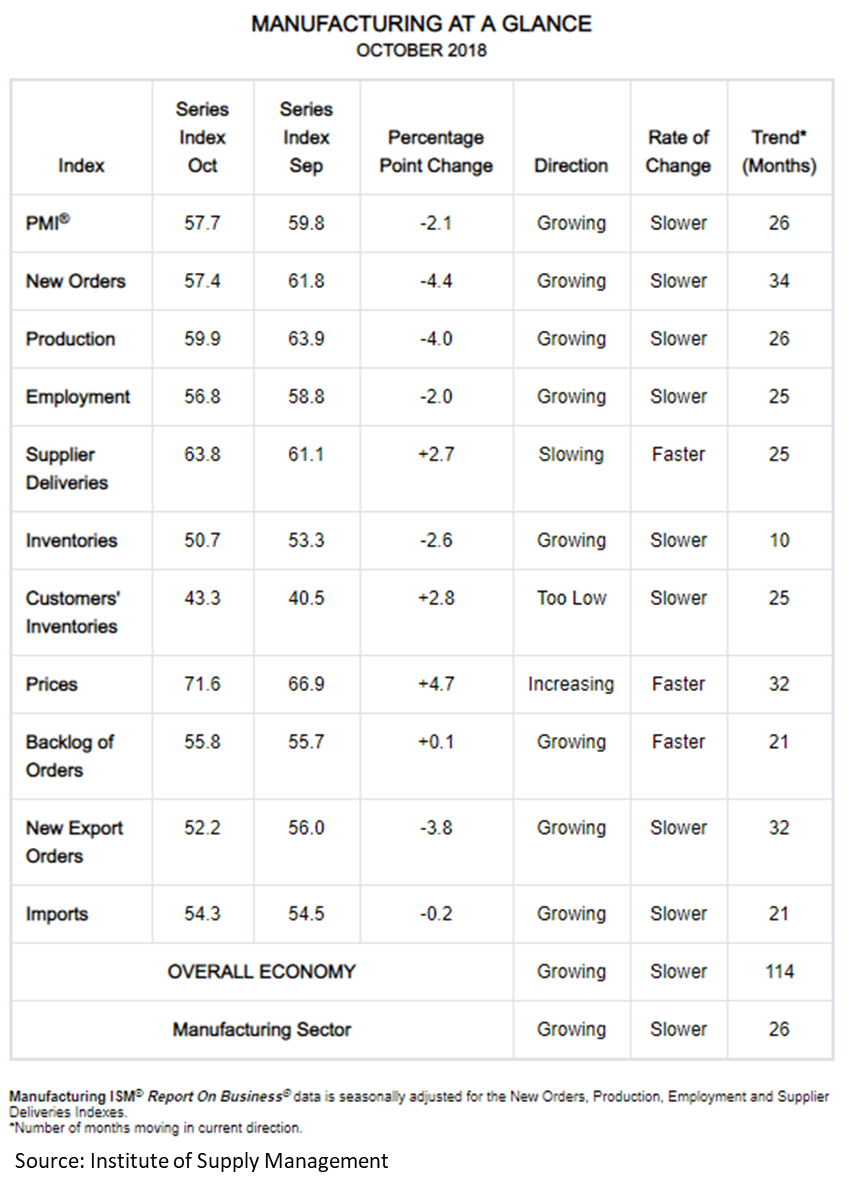

Manufacturing activity continues to be strong, according to the latest ISM Report on Business, although slowing its pace of growth as it enters the fourth quarter. The October PMI declined 2.1 percentage points from September to register 57.7 percent.

Most of the components of the PMI are trending at a slower rate. The new orders index fell 4.4 points, recording a decline for the second consecutive month. Production expanded at a slower rate, falling 4.0 percentage points to a reading of 59.9 percent.

“Labor constraints throughout the supply chain, impacts due to lead-time expansions and transportation difficulties continue to limit full production potential,” says Timothy R. Fiore, chairman of the Institute for Supply Management Manufacturing Business Survey Committee. “Overall, the manufacturing community continues to expand, but at the lowest level since April 2018.”

Supplier deliveries slowed in October and lead times continued to extend. The backlogs index grew at the same level as in September.

Raw material inventories expanded marginally in October, barely keeping up with production, said Fiore. The customer inventories index rose 2.8 points to 40.5 percent, but was still considered too low.

The prices index jumped 4.7 points to 71.5 percent, indicating higher prices for raw materials. The committee noted that prices have softened for steel, steel components and aluminum.

Indices for imports and exports declined 0.2 percent and 3.8 percent, respectively. Primary metals were among those industries reporting a decrease in new import and export orders.

Respondents to the ISM Survey expressed concern over supply chains and tariffs:

- “While order intake remains steady, the pace has slowed since the first half of the year. Instead of growing, the backlog is declining. We were processing orders at a high level; now they are at the point of status quo from late 2017. We are not concerned yet, but there is certainly trepidation about the future.” (Machinery)

- “We continue to run at full capacity. I continue to see pricing pressures and longer lead times in most commodities.” (Primary Metals)

- “Demand is high, and the supply chains are stressed.” (Transportation Equipment)

- “Orders and shipments are strong right now. Backlogs for Q4 and next year are way down. Savvy customers are asking us to hold pricing on blanket orders, but material suppliers will only hold prices for a few days, which puts us in a bad spot. We’ll be spending as much as possible on capital improvements before the end of the year.” (Fabricated Metal Products)

- “NAFTA 2.0/USMCA does nothing to help our company, as it does not address Section 232 tariffs.” (Plastics & Rubber Products)

- “Mounting pressure due to pending tariffs. Bracing for delays in material from China — a rush of orders trying to race tariff implementation is flooding shipping and customs.” (Miscellaneous Manufacturing)

- “Steel tariffs continue to negatively affect our cost, even though we utilize U.S. sources for steel. Oil prices put meaningful upward pressure on cost. Continued tightness with truck drivers is expected.” (Petroleum & Coal Products)

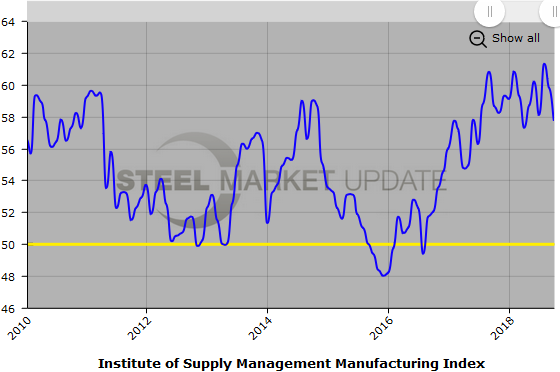

Below is a graph showing the history of the ISM Manufacturing Index. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging in to or navigating the website, please contact Brett at Brett@SteelMarketUpdate.com.