Prices

April 9, 2019

SMU Market Trends: Majority Unconcerned About Short-Term Prices

Written by Tim Triplett

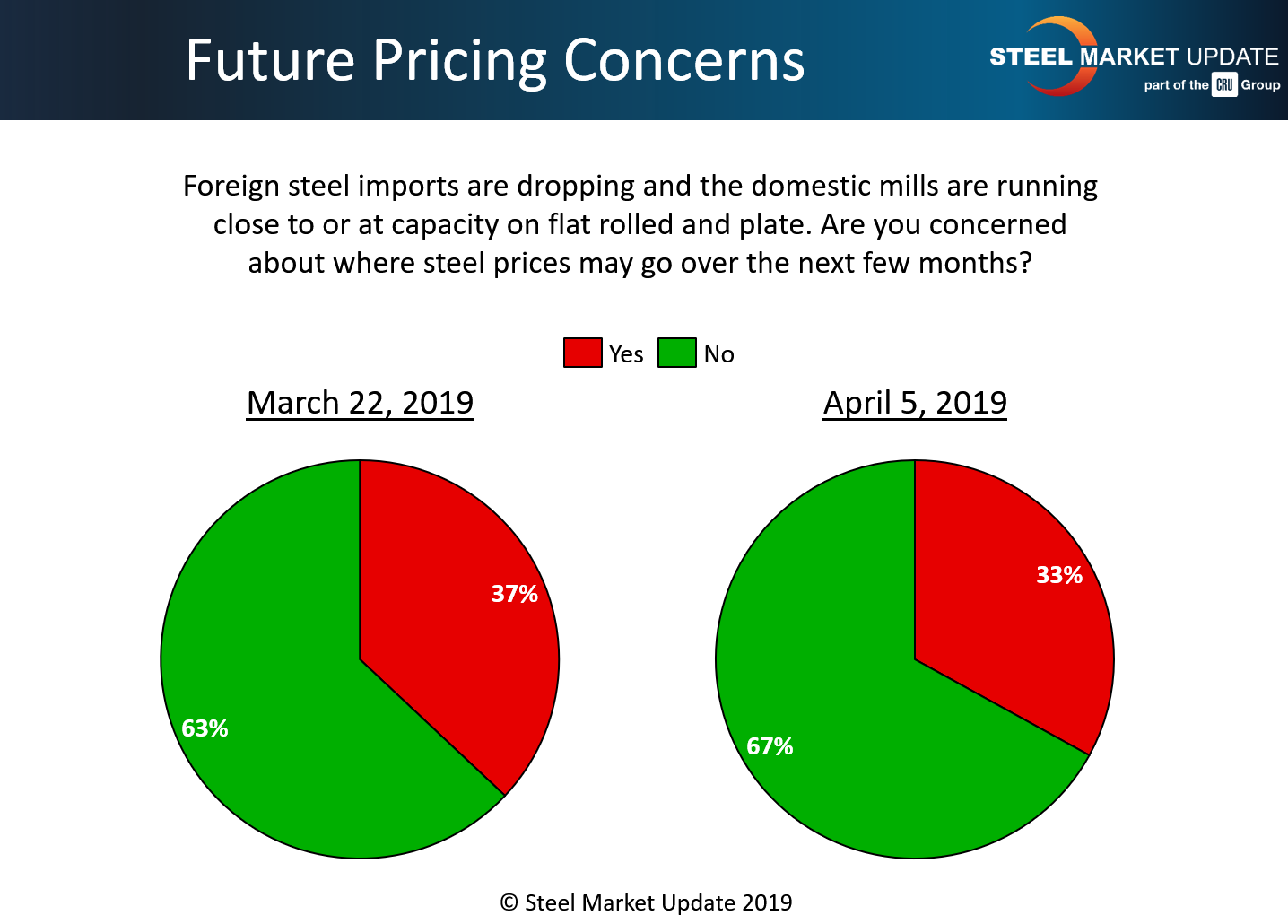

A surprising two out of three respondents to Steel Market Update’s market trends questionnaire last week said they are not concerned about the direction of steel prices, at least in the short term, though some question the staying-power of current demand.

Steel Market Update asked: “Foreign steel imports are dropping and the domestic mills are running close to or at capacity on flat rolled and plate. Are you concerned about where steel prices may go over the next few months?” In the final tally, just 33 percent indicated they are anxious about steel prices.

Below are some respondents’ observations on current market conditions and how they may impact steel prices:

- “Demand seems slow. Unless we have a real surge in demand, I think there is plenty of steel domestically to supply the market.”

- “If you review the immediate and slow release reaction to the “injection” of increases from the mill, there has been very little change except for stabilizing the minor slide from Q4 into early Q1. I might be in the minority, but imports were low then and demand was on the rise, so…”

- “I believe we have another $20-40 up and then will slide into the summer months.”

- “Increased capacity seems to be offsetting decreased imports. So far.”

- “The next few months are fine. It is the longer term I am worried about with all the new capacity announced.”

- “We have pricing and tonnage locked up for Q2. I believe that any price increases (if there are any) will have backed off by the time we need to order again.”

- “I’m not worried in that the steel market, being artificially stimulated by the tariff, is predictable in its direction upward.”

- “While imports are likely to recede, they will not disappear. Demand seems poised to decline over the near term and additional CRC and coated domestic capacity should be a factor starting in late second quarter.”

- “If there is an unplanned outage, look out!”

- “It doesn’t feel like a normal market during a time (a second quarter) that should see strong consumption and improved pricing.”

- “I feel an induced shortage is on the way.”

- “I would certainly not build inventory because it will be a temporary cycle.”

- “I’m keeping a healthy supply of steel until governments stop the protectionist measures like Section 232, which creates steel price volatility.”

- “If domestic capacity utilization drops, imports will fill in the supply. Demand is what will determine where the prices go.”

- “I expect domestic prices to rise until they max the customers’ patience. This tends to make imports more attractive. History repeating itself.”

- “I think demand for steel using industries is dropping.”

- “There is still plenty of steel available in the world. There may be short-term interruptions, as may be the case if there is a filing against Vietnam, but enough material will eventually find its way here. Also, the Mexico-Canada situation will at some point be resolved.”

- “The effect will be universal—if you need steel, you’ll pay the going rate.”

- “The threat of imports is ever present. That will keep prices in check. Also, new mills like Mingo Junction and Big River will continue to sell at lower than market prices for the necessity of generating positive cash flow.”

- “A temporary increase in pricing is to be expected, but as new domestic capacity comes on line pricing will stabilize. In addition, if automotive, appliance and other large steel-driven industries see any significant downturn, prices will adjust proportionately.”

- “We are constantly being introduced to new sources. Most of our purchases have us covered through September and we feel we are well positioned for any upturns. In the event there are downturns, our purchase prices should absorb as much as a 15 percent downside.”

- “It doesn’t feel like demand will support higher prices. I’m not sure what will change the game.”

- “I find it interesting that at 80-90 percent we are ‘at or near capacity.’ That being said, there is still too much inventory in the supply chain and way too much foreign material available. It will get here one way or another.”

- “Imports from countries with quotas will be up again soon. There are talks of having high quotas for Canada and Mexico as necessary for the Congress, Canada and Mexico to ratify USMCA.”

- “We still have global overcapacity. There are still imports coming in, at lower levels but enough to satisfy needs. Pricing should be pretty flat this year. It may rise some in the coming months, but will surely go back down.”

- “The mills will push numbers hard this quarter, again for the windfall profit, only to torpedo their own increases as demand slackens in July.”

- “Demand will have to increase before pricing can escalate and hold firm.”

- “Inventories are dropping and, with foreign shipments also falling, we expect at least a minor bounce within the next few months.”

- “Mills may be running at capacity based on a combination of lower contract pricing and the anticipation of normal seasonal demand. Demand is the big question mark in the equation.”

- “If the mills get greedy and irresponsible, we go foreign!”

- “Even with lower imports, new capacity here has been able to fill the gap based on current demand.”

- “Higher mill prices seem imminent in the months ahead. However, higher priced inventory may still keep spot prices moving sideways.”

- “Demand is the question mark. Automotive builds will be reduced with the shutdowns announced by GM. Inventories are starting to climb. There will be more pressure on pricing as demand decreases.”

- “I think the mills will continue to play the same game—keep prices just below foreign to keep their mills full.”

- “As soon as the price rises and tariffs go off or are reduced, foreign steel will become immediately available. World demand uses less than 80 percent of capacity.”

- “Demand is steady, but not increasing. Overall, the economic picture isn’t great. Auto sales are definitely dropping. Mills can convert auto tons to general manufacturing business. I don’t foresee a supply shortage.”

- “I think we could see an uptick here as the weather gets better and there’s no foreign steel coming in.”

- “All the signs point to a rise in flat steel prices in the next few months. But manufacturers are claiming they are unable to increase their prices, so they’re pushing back hard on paying any higher steel prices.”

- “We have no concerns at this time, unless an unplanned outage occurs or a spike in demand.”

- “More foreign will come in to meet the demand left open by the mills. This means the market drops.”

- “I don’t see the demand and therefore I believe we will have a gradual decrease in pricing.”