Prices

April 9, 2019

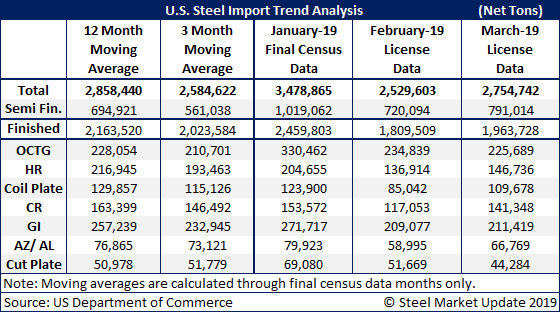

Steel Import License Data for March

Written by Brett Linton

The U.S. Department of Commerce released updated import license data on Tuesday evening, with new March license estimates up slightly to 2.76 million tons. These latest figures would be above the three-month moving average (3MMA, through final January data), but below the 12-month moving average (12MMA).

When removing the semi-finished (mostly slabs) licenses from the data, the finished steel imports drop to 1.96 million net tons, below both the 3MMA and 12MMA.

Noticeable jumps between February and March import data occured for the following products: plate in coils (up 29.0 percent), cold rolled steel (up 20.8 percent), plate cut lengths (down 14.3 percent), and other metallic coated (AZ/AL, up 13.2 percent).

March license data levels are below both the 3MMA and 12MMA for all of the finished products in the table below, with the exception of oil country tubular goods (OCTG), which is above the 3MMA.

As mentioned above, foreign slab receipts continue to be high with the past three months averaging 843,000 net tons per month. Most of the semi-finished steels are going to mills such as California Steel, JSW Baytown, NLMK USA and AMNS in Calvert, Ala. One of our readers made an interesting comment that we want to leave you to think about:

“I continue to be surprised that most of the industry coverage around imports discusses lower sheet receipts. However, slabs continue at higher rates and are nullifying the impact of lower sheet receipts. And perhaps to make it slightly worse, there’s a lag effect, where those extra slabs will get rolled in the months ahead, acting somewhat as delayed inventory reporting by buyers. Assuming we continue to see slab imports arriving at recent levels, then the only way this doesn’t impact supply is if there’s a pullback in melt output (assuming all else is equal). Given current margin spreads for the mills, I think they’d all be loath to cut back production,” said one service center executive.

SMU will continue to monitor imports and will review slab data in more detail in future issues.