Prices

April 25, 2019

Market Prices Moving Sideways to Lower, Say Steel Buyers

Written by Tim Triplett

The vast majority of flat rolled and plate steel buyers are reporting to Steel Market Update that prices on all products will be moving at best sideways, with most believing prices will move lower from here. We are seeing pressure on hot rolled, cold rolled and plate prices right now as indexes on these products all move lower this week. Coated steels, galvanized and Galvalume, appear to have more support, but it will be difficult to maintain the spread between hot rolled coil at $640 per ton, and galvanized base of $815 per ton. That spread is now $175 per ton, well above the historical average, which is closer to $100-$120 per ton. One week ago, the HRC to GI spread was $155 per ton. Something has to give in the not-too-distant future.

SMU is trying to understand all the factors at play. Capacity utilization rates are being touted as 83 percent or higher at the domestic steel mills, even with two blast furnaces down at U.S. Steel Mon Valley. Various scheduled maintenance projects are coming up and the Section 232 tariffs are still in place. Even with all of these positives for the steel mills, pricing is under pressure.

A large service center provided some perspective on this phenomenon: “In my mind, the biggest reason it’s weaker [steel pricing] is because imports did not fall enough and stay low long enough when combined with the increased domestic output. Slab imports continue to run higher than a year earlier and are overwhelming the lower levels of sheet imports. We’re moving into an over-supply situation that will only worsen the deeper we move toward summer.” This executive continued with, “I think things are getting looser for sure. Lead-times have stalled and have come backwards in some cases. When we consider the myriad maintenance outages being taken between now and June, and we still see lead-times weakening, it portends bigger challenges ahead. Lower scrap prices and still relatively high imports are only adding to the challenges the mills are and will face in the weeks ahead. There are also newer indications that demand levels may be weakening on a more broad and sustained basis, but it’s difficult to discern whether this is temporary or a more long-term issue. We’re hearing that customers are catching up on past due order books and that future outlooks aren’t as rosy as hoped. The exception remains the energy sector where large projects are still being consummated, and a number of them are on the board for the coming months….”

As with any volatile market, not every company believes prices will move just in one direction. As mentioned above, there are products where lead times are extended and demand for those products is good. An executive with another distributor told us earlier this week, “[The market is] muddled…good description. Galv is stronger than HR. Prices have come off their highs, but with mini’s sold out with galv into June, there’s not much pressure to cave in.”

Last week, Steel Market Update conducted an analysis of the flat rolled and plate steel market trends through a survey that is sent to 540+ individuals. We conduct our surveys twice a month and have been doing this since shortly after our company began in fall 2008.

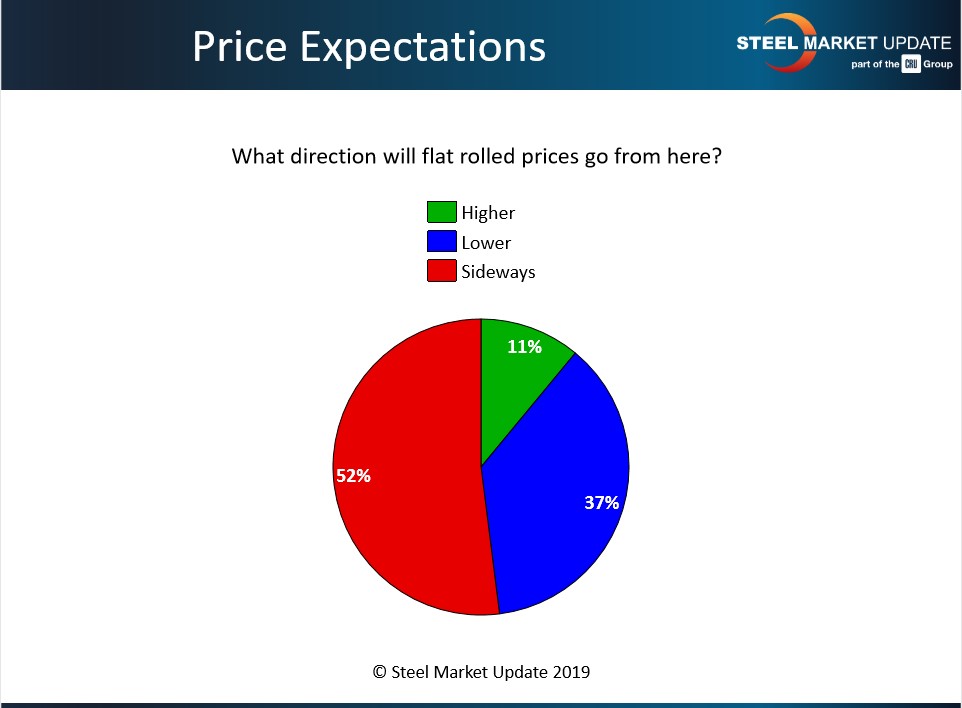

We looked at how buyers and sellers of steel feel about steel prices and what we should expect from here. Much like what we reported above, the majority of those responding to our survey believe prices will move sideways from here (53 percent). Another 37 percent believe prices will move lower while only 10 percent expect prices to increase, even at a time when seasonal demand usually picks up.

“It’s so hard to get a feel for demand. Obviously automotive is weakening. Construction is a key, and I feel very uncertain about an uptick in construction demand,” commented one executive.

“I have offers from suppliers to roll Q2 pricing into Q3. I am hoping that Q3 pricing will actually be a little better,” said one manufacturer.

“Prices will move lower if demand stays the same or declines,” said another respondent. “I am thinking down to $650 by summer,” added another.

“All flat rolled products are considerably weaker,” observed one service center exec. “If the long-anticipated decline in imports does not materialize, the mills are in for a disappointing year.”

One of the coated steel service centers provided some interesting insights that concern us as a steel publication. “Pricing continues to ebb and flow a few dollars every day and the major trade publications are now publishing daily rumors and unconfirmed transactions, which lead to even more confusion. But generally supply and demand are in relative balance with future pricing contingent on demand. Imports remain subdued and, at least in flat rolled, no new additions are anticipated for the immediate future.”

SMU is well aware of our responsibility to the industry as we strive to be fair and even-handed in our reporting. We have found, over the past 11 years, that reporting every single transaction or new special deal is not in the best interest of anyone. What is important is that you, your company and your suppliers are aware of the trend and any changes that might occur.

This will be a topic of discussion both during the 2019 SMU Steel Summit Conference as well as on the sidelines. When can too much information lead to indecision and paralysis?