Prices

June 16, 2019

CRU: Softer Steel Markets Weaken Metallics Demand

Written by Tim Triplett

By CRU Principal Analyst Chris Asgill

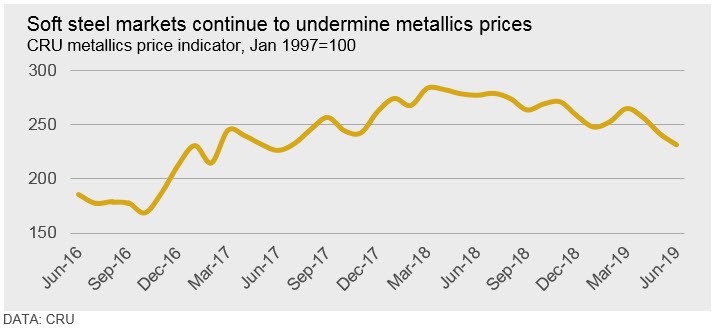

Scrap supply has continued to outpace demand in most of the key scrap supply markets and CRU’s metallics price indicator (CRUmpi) has fallen a further 4.2 percent m/m to 231.2 (see chart). This is the lowest level for the indicator since June 2017. The depth of U.S. scrap price weakness surprised the market, while seasonally softer demand elsewhere was generally the key driver of weakness. Steel market sentiment is gloomy and this is not expected to change in the near-term.

The U.S. was again the weakest market this month, with prices there falling by $30 /t m/m as a supply overhang remains. This is despite dealers slashing scale prices and inflows falling throughout May, and is indicative of the fall in scrap demand. In Europe, excess supply is not so much the issue, but demand has softened as a result of weaker steel markets, particularly in Italy. Despite healthy scrap demand in Russia, domestic prices there have fallen due to softer steel market sentiment. In Japan, seasonal demand weakness is a key driver of price declines as mills cut output amid softer construction activity due to the monsoon season there currently.

Importing markets also have faced weakness. In Asia, this primarily has been seasonal steel demand weakness, alongside more bearish sentiment across the market. After falling through mid-May, Turkish import prices rebounded later in the month before slipping again more recently. The rebound was due to initial enthusiasm following the reduction in the U.S. Section 232 tariff from 50 percent to 25 percent. Since the 50 percent tariff was implemented in August 2018, U.S. imports of Turkish steel have been minimal as it was uncompetitive compared to other sources of material. Since the tariff reduction was announced, U.S. domestic steel prices have fallen further. This means Turkish rebar is no longer competitive, even despite the recent slip in scrap prices to below $300 /t CFR for HMS 80:20.

Despite rising costs following the recent surge in iron ore prices, pig iron prices have either fallen slightly or remained stable. Demand for Brazilian pig iron is coming mostly from Asia, while CIS pig iron demand is from the U.S. and Europe. Brazilian export prices slipped slightly m/m, while CIS export prices held their ground. For the CIS, weaker domestic conditions may lead to lower offer prices if U.S. demand does not pick up and provide support.

Outlook: Scrap Price Falls to Ease, But More Weakness Lies Ahead

While the pace of falls in scrap prices is expected to slow, further declines are possible. If inflows in the U.S. market drop sharply in June, this may stabilize prices there. Equally though, further steel market weakness may result in an additional but small price fall. Scrap prices elsewhere in the world command a premium to U.S. scrap now, at a level higher than in the past couple of years. This premium widens when the U.S. steel price premium to elsewhere in the world narrows as U.S. producers push for lower domestic prices and domestic demand as a share of scrap generation declines. These relationships are being distorted by import tariffs in the U.S., which have widened compared to the natural premium that U.S. steel prices have historically held to other steel markets.

Scrap prices are very low compared to iron ore and coal prices, particularly when accounting for high pellet premiums. Under these conditions, BOF-based producers would be expected to lift scrap rates and this should be occurring to a degree. Flat-rolled BOF-based producers are somewhat limited by prime supply, though, and with automotive output generally weak prime scrap generation growth has been limited. Even so, this has not been enough to support higher prime grade premiums due to the downward pressure on flat-rolled steel prices. This condition is not expected to change.

European BOF-based steel producers are understood to be considering output cuts in response to high iron ore costs and limited pellet availability. These producers could lift scrap rates, but these are already estimated to be near a technical limit. That said, this could still lead to an uplift in scrap demand from these producers of up to 10 percent if they increased scrap’s share of the charge by 2 percent. This would allow producers to reduce hot metal production, and thus exposure to pellets, by 2.5 percent.