Prices

October 20, 2019

CRU: North American Zinc Market Will Return to Surplus Next Year

Written by Sam Grant

By CRU Analyst Sam Grant

Looking at our North American zinc market forecasts for 2020, there are clear arguments for either a rollover or slight decline in contract premia as we head into negotiations during the final quarter of this year. In this article, we present an overview of the North American refined market fundamentals and discuss our current view.

North American Zinc Production to Experience Strong Growth

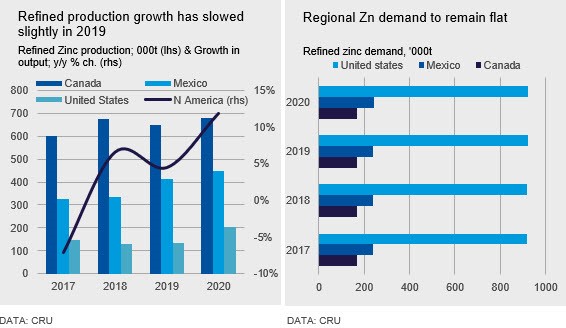

We estimate that North American refined zinc production will reach 1.13 Mt in 2019, increasing 4.5 percent y/y, despite issues which have caused a number of smelter disruptions this year and restricted growth rates. As the issues are resolved, we expect North American smelters to provide the market with an additional 142,000 t of refined metal in 2020. In the USA, AZR’s 150,000 t/y Mooresboro smelter is finally expected to restart in 2020 Q1, following a fire in late April this year which removed a forecast 60,000 t of refined production from the market in 2019. More recently in Canada, which is by far the region’s largest producer of refined zinc, Teck experienced a major equipment failure at the Trail refinery, which will take up to 20 weeks to repair, resulting in the loss of an estimated 30,000 t of refined zinc in the final months of this year, with a return to normal operating rates expected in the new year. In Mexico, although Peñoles’ 100,000 t/y smelter expansion ramped up a little slower than expected this year, Mexican 2019 refined production is expected to increase by 23 percent y/y as a result. Utilization rates at Torreon are expected to rise further next year, and we estimate that Mexican output will increase a further 8.7 percent y/y in 2020.

These issues led us to downgrade our estimate of North American smelter output this year, but barring further unforeseen disruptions next year production should grow strongly, and we anticipate growth of 11.9 percent y/y in 2020, bringing the total to 1.33 Mt.

At the same time, zinc concentrate availability in North America is set to remain stable in the medium term, despite scheduled closures at Teck’s Pend Oreille, Hudbay’s Flin Flon and Glencore’s Kidd Creek. North American zinc-in-concentrate production has been almost flat since the end of 2014, rising only 0.6 percent in 2014-2018, to 1.83 Mt. However, by 2020, increased output from several Peñoles mines and Peñasquito in Mexico will lift North American zinc-in-concentrate production above 2.0 Mt, even factoring in the recently announced closure of Nyrstar’s Canadian mine, Langlois, from 2020.

U.S. Demand is Expected to Remain Flat Next Year

North American refined demand is heavily dependent on the USA, which constitutes approximately 70 percent of regional demand. We estimate that the galvanizing sector accounts for approximately 55 percent of total U.S. zinc demand. CRU’s Steel Sheet team has forecast U.S. galvanized steel sheet demand will decline by 2 percent y/y in 2019. However, domestic output is forecast to increase 1.4 percent y/y, driven by a decline of 23 percent y/y in sheet imports, principally from Canada. Next year, our Steel Sheet team expects U.S. domestic galvanized sheet demand to fall by a further 3 percent y/y with output also declining 3.4 percent y/y, with Section 232 tariffs no longer supporting the domestic steel industry as in the opening five months of 2019.

One of the key end-use sectors in the U.S. is automotive, with the average vehicle weight in North America considerably greater than elsewhere in the world and including a very high proportion of galvanized steel. We estimate that the automotive industry accounts for approximately 25-30 percent of total North American refined zinc demand. This year has seen the global auto industry fall into decline, with emissions regulations and slowing trade key factors contributing to the downturn. In 2019, U.S. vehicle output is expected to decline 1.7 percent y/y and then remain flat in 2020, with tepid growth of 0.3 percent y/y, adversely affecting not only galvanized sheet demand, but the general galvanizing, die casting and zinc chemicals sectors too. The construction sector, which is also important for refined zinc demand, has performed slightly better so far this year. We estimate that U.S. construction output will grow 0.8 percent y/y in 2019 and accelerate to 2 percent in 2020.

Overall, we believe that U.S. refined zinc demand has remained flat this year and we forecast that demand will remain flat in 2020. This has been part of a longer-term trend and the case since 2016. As for the rest of North America, we also expect demand to remain flat this year, before picking up by 0.5 percent y/y in 2020. Mexico is expected to be the main driver of refined demand growth in the region going forward, due to the addition of new galvanizing capacity.

Refined Imports Should Moderate in 2020 as Mooresboro Comes On Stream

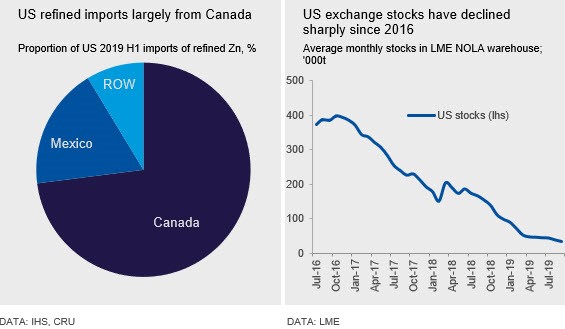

The USA is a large net importer of refined zinc, with 91 percent of the country’s imports coming from Canada and Mexico during the first half of 2019. Last year, U.S. net imports of refined zinc were 659,000 t, up 24 percent y/y, and we estimate that these will climb to just over 700,000 t in 2019. Imports from Canada have remained stable this year, climbing by 2 percent in 2019 H1, yet issues at Teck’s Trail smelter is likely to pull down this number through the final quarter. The USA’s net imports from Mexico have risen sharply, by 67 percent y/y, in January-August, due to the ramp-up of Torreon’s expansion. We expect the USA’s net imports to moderate in 2020 as Mooresboro comes on stream, potentially contributing 60,000 t to domestic supply.

Exchange stocks in North America have been drawn down dramatically over the last three years and the refined market has tightened. Refined zinc stocks in the LME’s U.S. warehouses declined to 25,300 t on Oct. 10, the lowest level since 2000. The recent supply side issues at Teck have led to some pockets of tightness in the U.S. physical market since September and a corresponding uptick in spot premia, but we understand that there is still enough spot metal to meet consumers’ requirements. While the market has tightened, it seems unlikely that premia will need to increase to a level that encourages imports from other regions in the near-term.

The Strongest Argument is For a Rollover or Decline in Premia

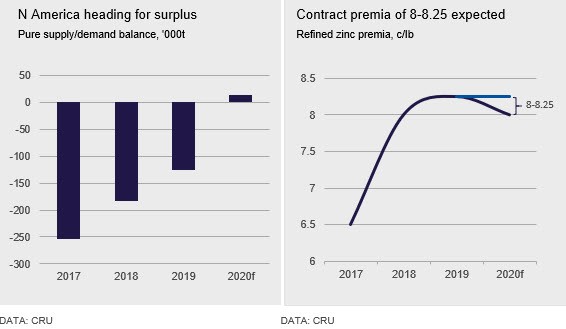

We forecast that the North American zinc market will return to a marginal surplus next year, following this year’s estimated 126,000 t deficit, based on the fundamental refined supply/demand balance. In terms of 2020 contract premia, we currently find the argument for a rollover or quarter cent decline, from 2018’s 8.25c/lb, the most compelling. While current market tightness increases the risk to the upside for premia, particularly if supply-side issues persist or demand suddenly picks up on the back of a positive resolution to U.S.-China trade issues, such developments are more likely to happen in 2020 rather than in the next few months, so we believe that it will be difficult for suppliers to achieve a higher number for next year’s long-term contracts. The fact that freight and trucking costs in the U.S. are still very high, while exchange stocks are at the lowest level in almost 20 years, supports a rollover. However, the expectation of a return to surplus in 2020 and the chance that the backwardation in zinc’s forward spreads will persist, with exchange stocks so low, suggests that premia could decline. Our current view is that premia of 8.00-8.25 c/Ib are most likely for 2020 contracts.