Prices

November 12, 2019

CRU: Chinese Pig Iron Imports Lift as High Local Scrap Costs Persist

By CRU Principal Analyst Chris Asgill

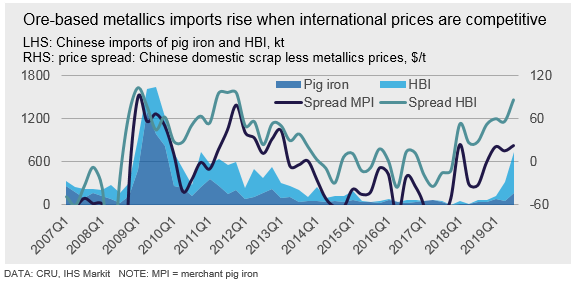

There has been a marked rise in Chinese imports of pig iron and HBI this year. This has been primarily due to limited domestic scrap supply that cannot be offset by external supply due to restrictions in scrap imports. Limited scrap supply relative to demand has meant that scrap prices in China have become high compared to other markets. Chinese mills have looked to offset high domestic costs by leveraging lower costs for pig iron and HBI in other markets. At this stage, imports have been confined to a few Chinese steel companies and are a small share of Chinese metallics consumption. However, the impact on the international market could be more significant as these “small” volumes represent a significant share of merchant trade. Ultimately, volumes will be capped as international ore-based metallics prices will rise to a similar level as Chinese domestic scrap prices and mitigate the cost benefit currently being gained. That said, international HBI and pig iron prices could become more closely linked to Chinese domestic scrap prices as buyers there enter and exit the market.

In 2019 Q2, DRI/HBI imports rose to just over 250 kt, with a further increase to 570 kt by Q3. Pig iron imports have taken longer to rise, remaining low in Q2 and increasing to 160 kt in Q3. International HBI prices were quicker to respond to growing steel market weakness than for pig iron, which is why imports for HBI rose comparably faster. International pig iron prices held ground for longer due to the greater impact of high seaborne iron ore prices on production costs for Brazilian producers of this material. More recently, international pig iron prices have come under pressure and traditional buyers had been holding out in anticipation of a price drop.

However, Chinese buyers have plugged this hole in orders, and we understand that Brazilian producers have secured around 250 kt of pig iron orders from China over the past six weeks. This has filled their order books through to December/January. This volume represents about 15 percent of historical merchant pig iron trade that is principally made up of three key sets of buyers from the U.S., Italy and Turkey. These orders have already turned around the fall in pig iron prices over the past month, despite producer costs falling, as we understand traditional buyers are now scrambling to secure volume.

Relative Pricing Enables Trade

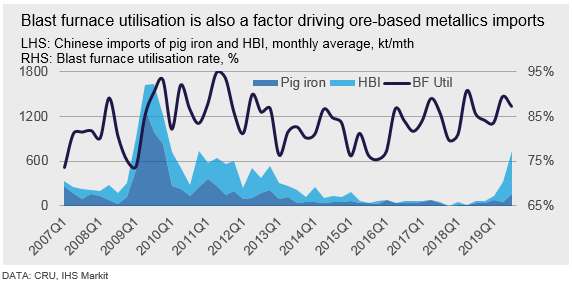

China has imported ore-based metallics in the past. Like the current situation, this was primarily when Chinese scrap prices exceeded those on the international market by some way. HBI has been the more “usual” material imported at these times, as pricing for it has been more closely aligned with international scrap prices. In contrast, pig iron prices have often been at a significant premium to scrap prices. Furthermore, ore-based metallics imports generally only occur when utilization of blast furnace capacity is high. Importantly, the two factors are linked, as high blast furnace utilization means a strong domestic market, which often means high metallics demand and, consequently, domestic scrap prices.

Chinese Ore-Based Metallics Imports to Persist, But of Limited Volume

Looking ahead, while we expect the Chinese scrap market to remain tight in 2020, it will be looser than in 2019. Demand will remain healthy next year, though availability is expected to increase. While the obsolete recovery rate remains stable in 2020 compared to 2019, there are policy factors impacting short-term supply dynamics that are not captured in this measure. This will mean the Chinese domestic scrap premium to international markets will ease in the year ahead but will remain high. Despite this, there are constraints on the imports of alternative materials, such as DRI/HBI and pig iron. This includes the size of the international merchant markets for these materials and the ease of importing in China.

Chinese Scrap Market to Remain Tight in 2020, But Less So Than in 2019

Chinese scrap demand is expected to grow next year, though at a much slower pace than in 2018 and 2019. Meanwhile, more scrap supply will be available through policy changes, which will help loosen the market slightly. A looser supply environment is expected to reduce the premium Chinese scrap holds to international markets. This premium reached $83 /t in 2019, up from $40 /t in 2018, and could fall back to $50 /t given the loosening in the market balance. At this level, there is incentive to import HBI, but will mean that pig iron is unlikely to be an attractive option.

In 2019, Chinese scrap demand grew 9 percent y/y, following the sharp rise of 19 percent in 2018. This was driven by policy changes in China that led to a lift in scrap rates in steelmaking production and a rise in EAF output, recovering some of the lost output from the closure of induction furnaces in 2017. Growth in 2020 is expected to slow to 1 percent y/y as, despite rising scrap rates, BOF-based output begins to fall and increases in EAF output are small by comparison.

In terms of supply, a number of government policy initiatives are expected to lead to greater availability in 2020. Shanty town renovations will lift demolition activity, which was low in 2019. Renovations are expected to increase in 2020, otherwise the government will not meet its target of 15 million units over the 2018-2020 period. Vehicle scrappage rates are also expected to increase as the industry transitions to BS-VI emission standards from July 2020. This will lead to an increase in scrappage rates of vehicles of BS-IV standard. Changes in government policy earlier this year regarding vehicle wrecking and the resale of car parts will further aide supply as the industry continues to develop. Additionally, prompt scrap supply (i.e. yield losses from steel consumption) is also expected to expand as output from the manufacturing sector, in particular the automotive segment, recovers following the weakness of 2019.

Constraints Limit Chinese Ore-Based Import Volumes

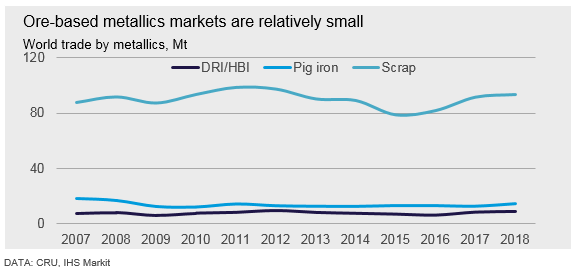

Aside from pricing dynamics, there are a few constraints on the ability of China to import sizeable volumes of these materials. Merchant ore-based metallics markets are generally quite small, meaning an increase in non-traditional sources of demand (e.g. China) would lead to an upswing in prices and erode the competitiveness of imported material relative to domestic supply. There are also regulatory hurdles to importing material in China, so typically it is larger state-owned enterprises that engage in this activity. Combined, these will limit Chinese import volumes of ore-based metallics until Chinese domestic and international metallics prices normalize.

Pricing in Small Ore-Based Markets Will Respond Quickly to Entry of Large Non-Traditional Buyers

Trade in ore-based metallics markets is relatively small. This would ultimately cap demand from the new entry, such as China in this case, as the material would no longer be competitive against other alternatives available domestically. As such the entry of a non-traditional buyer of sizeable volumes has the potential to lift prices significantly. For example, average trade in DRI/HBI and pig iron over the past few years has been about 8 Mt/y and 14 Mt/y, respectively. In contrast, trade in ferrous scrap has been closer to 80 Mt/y. Merchant supply of these materials is generally also concentrated in a few producing regions. For pig iron, a majority of supply is from Russia, Brazil and Ukraine. For DRI/HBI, merchant trade historically originated mostly from Venezuela, though domestic issues there have meant this is no longer the case. Today, Russia is the largest source of traded DRI/HBI, leveraging low cost domestic iron ore pellet supply.

Regulation Limits Attractiveness of Imports

We understand that large state-owned mills are the typical importers of ore-based metallics. This is because these mills are typically fully exposed to domestic taxes on scrap purchases and, consequently, their total cost for using domestic scrap is higher than smaller private mills that may avoid taxes. Additionally, state-owned companies are typically able to gain a Notice of Customs Clearance more easily than private mills, making imports of small volumes of material less burdensome.

Chinese Interest in Ore-Based Metallics Imports Will Remain Small

Historically, imports of pig iron and HBI have only occurred when it was cost competitive to do so and generally only when Chinese blast furnace utilization has been high. While blast furnace utilization will remain high in China in the year ahead, the competitiveness of these materials will wane. Chinese domestic scrap prices are expected to be high compared to international markets, though this premium will decline as international scrap prices rise from recent lows and the Chinese market loosens slightly. As international scrap prices increase, so will HBI prices and, to a lesser extent, pig iron prices. The latter lesser increase is because international pig iron prices have held more ground than scrap and HBI prices recently. Even if prices for imports of these materials were to remain more competitive than expected, Chinese buyers cannot lift imports significantly. To do so would tighten these markets sufficiently to drive prices higher and undermine the competitiveness of imports. That said, there is the potential for international ore-based metallics to become more closely aligned with Chinese domestic scrap prices over the near-term as Chinese mills enter and exit these markets.