Market Segment

November 19, 2019

CRU: How Long Will China’s Cost Disadvantage Constrain its Steel Exports?

Written by Paul Butterworth

By CRU Research Manager Paul Butterworth, from CRU’s Global Steel Trade Service

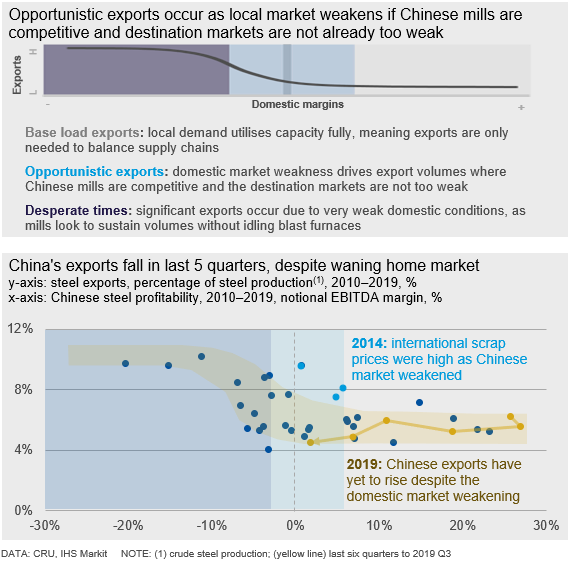

Although profitability for domestic sales in China has fallen sharply in 2019, steel exports from the country have not risen. Historically, when domestic profitability dropped, exports would rise. Prior analysis has shown that the strength of the domestic market is a key driver of Chinese export volumes, with additional factors being cost competitiveness and the strength of destination markets (see our Insight – Chinese steel exports: lower volumes, higher prices). Earlier this year, international markets were weaker than those in China and sales domestically were more attractive. As the year progressed, the Chinese market has weakened and, by late-Q3, margins there were negative. However, as international markets were also weak and Chinese costs were higher than elsewhere, this has meant that Chinese exports have remained low. Earlier in the year, the Chinese domestic market, while weakening, was stronger than potential destination markets. Cost competitiveness was also a factor at this time, though it was not until the second half of the year that it become a key limiter of exports. High costs have been driven by strong domestic coal and scrap prices compared to international markets. This Insight will focus of the impact of this cost disadvantage and address potential outcomes should this situation reverse: in every case, global steelmakers’ margins remain weak unless the Chinese domestic market recovers.

Exports Generally Rise When the Domestic Market is Weak

Previous analysis by CRU has shown that there is a close relationship between the performance of the domestic market in China and the level of exports from the country and that profit performance is the primary driver of export propensity. That is, when the domestic market is performing poorly and steel sector domestic margins are low, exports tend to increase as steelmakers are incentivized to seek sales outside the country. Analysis also showed that cost competitiveness was a secondary factor dictating the level of exports.

Despite Weak Domestic Conditions, China is Out of the Export Market So Far This Year

Steel mill profitability in China has weakened throughout 2019, most notably in Q3. Given this, exports of steel from the country should have increased materially over recent months. However, exports as a percentage of crude steel production have fallen and Chinese mills have remained largely out of the export market, which has opened up opportunities for Turkish, CIS and Indian material. Indeed, the steel market generally is performing poorly, which is forcing all steel producers to seek alternative markets, but why has China remained stubbornly out of the export market so far?

Under normal circumstances, given current profitability, we would expect China to be exporting more steel today, perhaps by as much as 20 Mt on an annualized basis. Manufacturing and industrial production has been impacted by uncertainty caused by the trade war and, while stimulus measures provided a significant boost to primarily longs demand in 2019 Q2, this was unable to lift the fortunes of the sector. As a result, domestic market profitability has fallen to well below minimum sustainable levels and turned sharply lower in Q3. While profitability fell below sustainable levels during Q2, destination markets were weaker than the Chinese domestic markets and international steel prices were low enough to disincentivize exports. This was exacerbated by a combination of government policy and poor market conditions that have served to undermine the cost competitiveness of Chinese steel mills and this is a likely block on higher exports currently. However, if conditions changed, China would return to the steel export market, which would further undermine an already fragile market.

China Cost Disadvantage is Due to Coal and Scrap Prices

There are three key areas where Chinese costs are currently higher than elsewhere. Chinese domestic coal prices are higher than seaborne prices due to import restrictions in the country. International scrap prices are low compared to bulk raw materials prices (i.e. iron ore and coal), which is improving the competitiveness of EAF-based output relative to integrated BF/BOF-based producers. Furthermore, Chinese domestic scrap prices have remained higher, limiting the competitiveness of Chinese EAF output.

This cost disadvantage is further illustrated by the fact that there are examples of Chinese companies importing billet, slab, coke, pig iron and DRI/HBI, which suggests they can be more competitively sourced from the seaborne market than domestically—a very unusual situation and one that is not expected to be sustained.

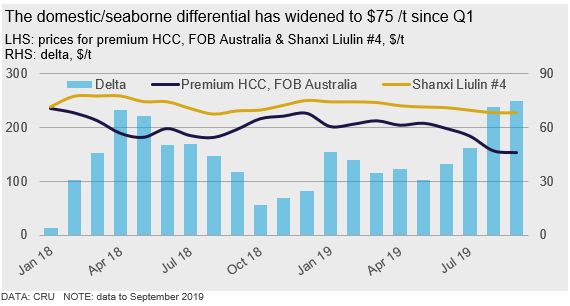

Chinese Domestic Coal Prices are Higher Than Seaborne Prices

The Chinese government has imposed a series of import restrictions on coal that, while not necessarily limiting overall volumes, have resulted in depressed prices on seaborne coal. This is primarily due to the time delays associated with getting coal into the country, up to 60 days delay in some circumstances. At the same time, domestic coal prices have remained elevated and the gap between domestic and seaborne prices has widened significantly. In contrast to iron ore, Chinese coal consumption is primarily domestic material, so high domestic prices relative to the seaborne market affects production costs significantly.

The chart below shows that the typical differential between domestic and seaborne coal is about $30 /t, with domestic coal commanding a premium after value adjustments associated with lead times, etc. However, since 2019 Q1, this differential has lifted to as high as $75 /t at times. Given the typical usage rate of coal in the steelmaking process, this will be disadvantaging Chinese steel mills by ~$30 /t relative to their peers in the export market.

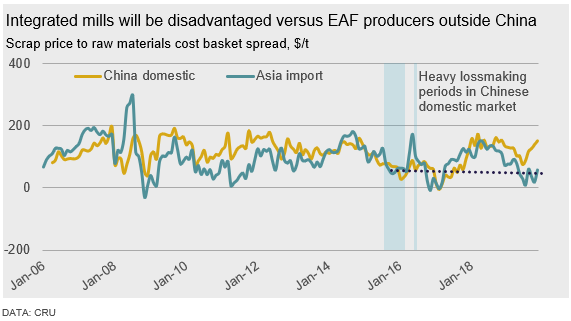

International Scrap Prices Have Remained Low Compared to Bulk Raw Materials Costs

A significant proportion of Chinese exports would compete with EAF-based production that uses scrap as its primary feedstock, particularly for steel long products. International scrap prices have been weak compared to bulk raw materials due to the weakness in international steel markets. The chart below shows the delta between the price of scrap in Southeast Asia and a basket of raw materials contributing to hot metal costs (i.e. iron ore and coal). From this chart you can see that scrap prices are currently very low compared with bulk raw materials. A majority of Chinese steel output is BF/BOF-based and the disadvantage from high cost coals is compounded by weak international scrap prices, limiting their ability to export. This analysis suggests the cost disadvantage will be greater than $100 /t before considering the cost of Chinese domestic scrap that is high-priced currently.

High Domestic Scrap Prices Impact Both Chinese BOF and EAF-based Competitiveness

Compounding issues further, Chinese domestic scrap prices have remained high since late-2017, when winter heating policies limited hot metal output and drove higher scrap consumption per tonne of steel output so that mills could sustain production. Higher scrap prices were not so much of an issue initially due to the high profitability of the sector at the time. However, since domestic steel prices started to fall at end-2018, this has impacted competitiveness in a variety of ways.

In the first instance, it meant Chinese EAFs were not competitive in the domestic market and they lowered steel output in response—effectively tightening the market as BOF-based producers filled the void left locally, rather than seeking volumes in the export market. Combined with low international scrap prices, high domestic prices have meant Chinese EAFs were not competitive abroad either and could not use these markets as an outlet for steel production.

Secondly, BOF-based producers also consume scrap and are also affected by high scrap costs. Because the marginal BOF tonnes are largely scrap-based (i.e. scrap provides a productivity uplift for the BOF but is also higher cost than the hot metal charge), this means these volumes are also not competitive in the export market. In other words, a steelmaker would limit output and reduce scrap consumption, rather than export and accept losses on the trade due to high scrap costs.

Chinese Market Weakness Caps International Recovery

While the cost disadvantage for Chinese steel may remain in place, the risk is that costs normalize. This could mean greater export volumes if the Chinese domestic market stays weak. If Chinese exports do rise and costs have not normalized, then this would indicate the domestic market there has weakened further and mills have become more desperate for volume. Furthermore, a recovery in international markets relative to China would likely lift international scrap prices, which would lift costs outside China and potentially reshape the cost position of Chinese mills. In every case, this places a cap on any recovery that may be tentatively taking hold in a number of markets currently, unless the Chinese domestic market stages a recovery itself.

Coal Price Premium to Fall When Quotas Reset at Start of 2020

Coal import quotas in China reset at the beginning of each year. This is expected to enable greater supply of imported material in early-2020, which will reduce the domestic price premium for coal. That said, the import quotas remain in place throughout the year and have caused delays in customs clearance. As such, the premium for domestic material is expected to remain above historical levels in 2020.

Domestic Scrap Prices to Remain High Compared to Bulks, But Less So to International Scrap

Environmental policy in China is expected to continue to support scrap demand. Meanwhile, the industry is still adapting to the combination of stronger demand and policy adjustments that limit both scrap availability (e.g. demolitions) and transportation. This is expected to lift domestic scrap prices relative to bulk raw materials. Meanwhile, international scrap prices are expected to rise in the coming six months. The tentative turnaround in steel markets is part of the driver of this, though is being compounded by scrap supply as winter tends to limit supply in key markets, such as the USA and Europe. The spread between Chinese and international scrap prices is significant (e.g. over $110 /t in November 2019), so international markets would have to recover strongly for this to come into play.

International Price Gains Capped by Threat of Chinese Exports

While the Chinese domestic steel market remains weak, this places a cap on any recovery that may take place in the international steel market. Steel prices need to stay low enough to ensure that Chinese steel remains uncompetitive. Likewise, international costs need to remain below Chinese costs. Ultimately, this means that while announced steel plant closures in several markets (e.g. in Europe, the USA and South Africa) would tighten these markets and potentially support prices, there is a cap on how high these can go. Too much exuberance following the recent downturn and exports will again become an attractive option for Chinese mills. In other words, the strength of destination markets may override the costs disadvantage that is currently limiting export volumes.

Chinese Exports May Rise, But Only If International Steelmakers Get Too Exuberant

There appears little scope for a sustained and significant recovery in international steel margins until the Chinese domestic market recovers. Otherwise, such a recovery would lead to greater Chinese steel export volumes and international steel prices and margins would fall back again. Importantly, while capacity closures outside China are underway and may tighten these markets as utilization of the remaining operating assets increases, margin gains are still capped by the threat of Chinese steel exports (i.e. destination markets would become attractive despite higher costs). A fall in Chinese costs, without a recovery in the country’s domestic market, would be the most damaging scenario as it would keep global steel prices at a lower level. This is because Chinese steel could be competitive again, despite weak destination market conditions.

If you would like to discuss dynamics in the current steel and raw materials markets or get more information on CRU’s Steel Cost Model or raw materials and steel prices, please click the link below.