Prices

December 22, 2019

Foreign Steel Imports Down in the Fourth Quarter

Written by Brett Linton

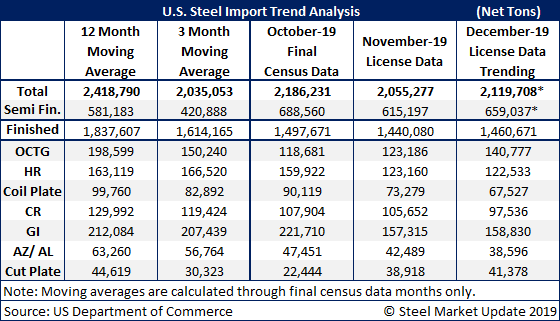

With the month nearly complete, finished steel imports into the United States in December are trending in line with October and November at just over 1.4 million tons, based on Steel Market Update’s projections of Commerce Department license data. Finished steel imports in the fourth quarter have been well below the 12-month average of around 1.8 million tons.

Steel Market Update will no longer project imports of semifinished steel—mostly slabs imported by domestic mills—at least as long as imports from major steel-producing nations such as Brazil are subject to quarterly quotas. The quotas tend to skew the monthly license data. As noted by the asterisks in the table below, the figure for semifinished represents actual import licenses through Dec. 17. The total figure of 2.1 million tons is the sum of the projection for finished steel and the actual for semifinished. Although they are preliminary, these figures indicate that steel imports were down in the fourth quarter.

Looking at the December projections by product category, hot rolled and galvanized imports were little changed from November. OCTG imports were on track for the biggest gain.