Government/Policy

December 28, 2019

CRU: “Phase I” Trade Deal Raises Downside Risk to the Dollar

Written by Ross Cunningham

By CRU Senior Cost Economist Ross Cunningham, from CRU’s Economic Outlook

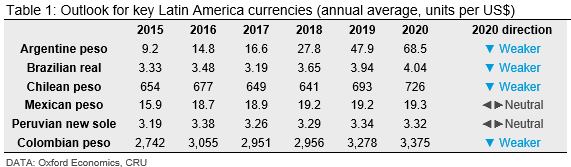

Political uncertainty equals big losses for Americas currencies. During the latter half of 2019, currencies in key South American economies have lost significant ground against the dollar. Since these economies depend on commodity exports for their growth, the negative effects of the trade war on Chinese import demand, as well as on global growth prospects overall, were already in place before political unrest flared.

Populism Returns to Argentina, But Investors Flee

The Argentine peso (ARS) had lost more than half its value by the end of 2018 due to high inflation and questionable choices by the central bank in terms of lowering interest rates. The high inflation problem was one of the reasons why President Macri was defeated in his re-election bid by Alberto Fernández and the former President Cristina Fernández de Kirchner.

After becoming president in December 2015, one of Macri’s first tasks was to allow the ARS to devalue to a realistic level. Macri then negotiated new debt servicing terms with the IMF and floated Argentine bonds for the first time since it defaulted on its sovereign bonds back in 2001. Macri has delivered on the IMF milestones, but doing so required austerity measures that the voting public found too difficult to support.

President Fernandez assumed office on Dec. 10. Prior to the inauguration, however, the government announced it would reprofile the country’s debt without imposing “haircuts” on principal or coupon reductions. This is to be achieved by two measures: extending maturities of short-term domestic debt for institutional bondholders and seeking a voluntary reprofiling of local and foreign-jurisdiction long-term debt, including that owed to the IMF under the current program. It is possible that creditors will not agree to the voluntary reprofiling and it is quite likely that Argentina will go through another episode of debt restructuring in the next few years.

The ARS is currently trading at 59.8/$. Although it has not lost much ground since the primary elections in August, we do not expect the new Fernandez administration to be as orthodox as the Macri government. We expect the ARS to continue to weaken to average 70/$ in 2020 given that inflation remains very high, though it is beginning to stabilize.

Brazil’s Long-Term Prospects Have Improved But the Near-Term Outlook is Cloudy

The Brazilian real (BRL) gained ground in early 2019. However, as it became clear that Argentina’s economy would deteriorate more significantly and the trade war between the U.S. and China was likely to escalate further, the BRL lost ground during both Q2 and Q3.

Thus far in Q4, the BRL has depreciated to its weakest ever level against the dollar due to a storm of factors. The election of the Fernández/Fernández de Kirchner ticket in Argentina raises new concerns about the ability of Brazil’s largest trading partner to manage a rebound. Brazil’s export surplus narrowed sharply in October, confirming that the trade war was taking a toll on the economy. The recent auction of offshore oil leases was not well subscribed by foreign companies, so the prospect of new foreign direct investment to boost growth in 2020 and beyond has not materialized. Inflation is well under control, in part due to weak domestic demand, so Banco do Brasil has been cutting the benchmark SELIC rate, reducing the rate of return for investors. In addition, the release of former President Lula from prison seemed to dent investor sentiment outside of the country.

The Brazilian central bank has been vigilant on inflation and has acted prudently. Lower inflation and lower interest rates should boost the country’s growth prospects, therefore policymakers are not yet worried about the weaker BRL, particularly since it makes exports more competitive. The BRL is currently trading at 4.14/$, off the all-time low of 4.26 on Nov. 27. We expect the currency to stabilize and average 4.0/$ in 2020.

Civil Unrest Heats Up in Chile

On Oct. 6, underground (subway) fares were raised by 3.8 percent from CLP800 to CLP830. The fare hike resulted in widespread fare evasion and protests by secondary school students. The protests spread and intensified, turning violent on Oct 18. The protests continue but are abating as the summer holiday season approaches.

The CLP has seesawed during Q4. On Sept. 30, the peso closed at around 729/$, this level of weakness reflecting the challenging environment for copper demand. It reached an intra-day low of 837/$ on Nov. 28 following a weak reading for overall economic activity. The Piñera government responded on Dec. 2 with a $5.5bn employment protection and recovery plan, which buoyed the CLP; it is now trading at 777/$.

Although weaker demand from China for Chile’s main export, copper, has fed into the CLP’s weakness during 2019, Chile is better placed than others to weather this storm of civil unrest. The ratings agencies are interpreting the protests as a one-off that the government will solve with reforms. A referendum will be held in April 2020 and the outcome will affect the investor outlook for Chile. However, with a two-thirds majority needed to enact major changes, the new Chilean constitution may look very much like the one in existence today. Banco Central do Chile is vigilant on inflation and has announced it will sell dollars to support the CLP through May. Though we expect higher inflation to result from the weaker peso, we do not anticipate inflation will average above 4 percent in 2020. We project the peso to be weaker on average in 2020 compared to 2019, but it should also strengthen from where it sits today.

The Causes May Be Similar, But the Outcomes Will Diverge

2019 has been underlined by a strong dollar, the causes of which are macro driven. The trade war is the key factor boosting the safe haven status of the U.S. dollar. While we do not expect the U.S. and China to settle their differences in any meaningful way, an agreement between the two countries that provides more certainty around the trading relationship in the future could allow the dollar to weaken.

The table below illustrates our outlook for the currencies of the key South American economies covered in CRU’s cost services. As noted above, we expect the ARS to have a difficult time in gaining any ground. That will spill over into Brazil as well, but Brazil could find better export prospects in 2020 to stem further deterioration in the BRL. The CLP should strengthen from current levels if the government is willing to go far enough on its reforms.

Country Exchange Rate Perspectives

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com