Prices

February 23, 2020

January and February Foreign Steel Imports

Written by Brett Linton

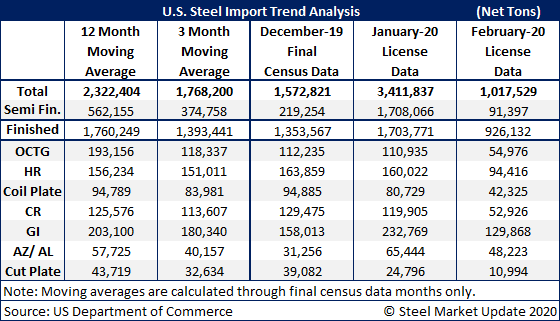

Licenses for imports of finished steel in January totaled around 1.7 million tons, according to the latest Department of Commerce data, well above the three-month moving average near 1.4 million tons. While the January license data is prelminary, the last time the final Census data for finished imports was this high was in August 2019 at 1.8 million tons.

Import licenses in January totaled 3.4 million tons, including licenses for 1.7 million tons of semifinished products. Those figures are unusually high as a result of buyers seeking to max out quarterly quota limits. The final Census data will show actual imports averaging lower during the course of the quarter.

License data through Feb. 18 shows total imports of just over one million tons, including 926,000 tons for finished products alone. Looking back at license data reported in mid-January, finished product imports were slightly higher at 1.0 million tons, meaning February to date is trending down approximately 12 percent.

Due to Trump administration tariffs and quotas that skew the data, Steel Market Update has not projected any of the figures in the table below.