Prices

May 21, 2020

Hot Rolled Futures: Raw Materials Roar

Written by Tim Stevenson

SMU contributor Tim Stevenson is a partner at Metal Edge Partners, a firm engaged in Risk Management and Strategic Advisory. In this role, he and his firm design and execute risk management strategies for clients along with providing process and analytical support. In Tim’s previous role, he was a Director at Cargill Risk Management, and prior to that led the derivative trading efforts within the North American Cargill Metals business. You can learn more about Metal Edge at www.metaledgepartners.com. Tim can be reached at Tim@metaledgepartners.com for queries/comments/questions.

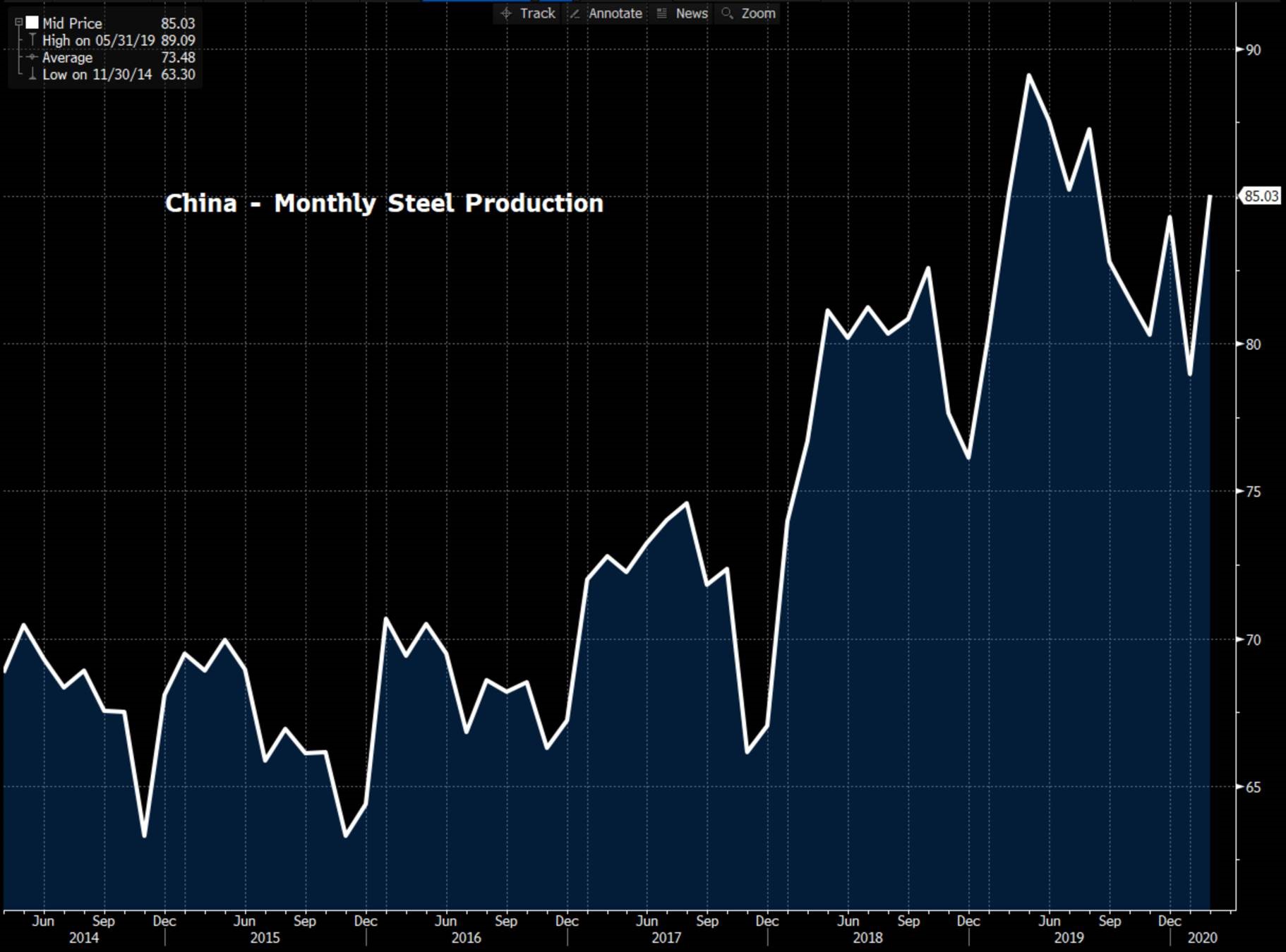

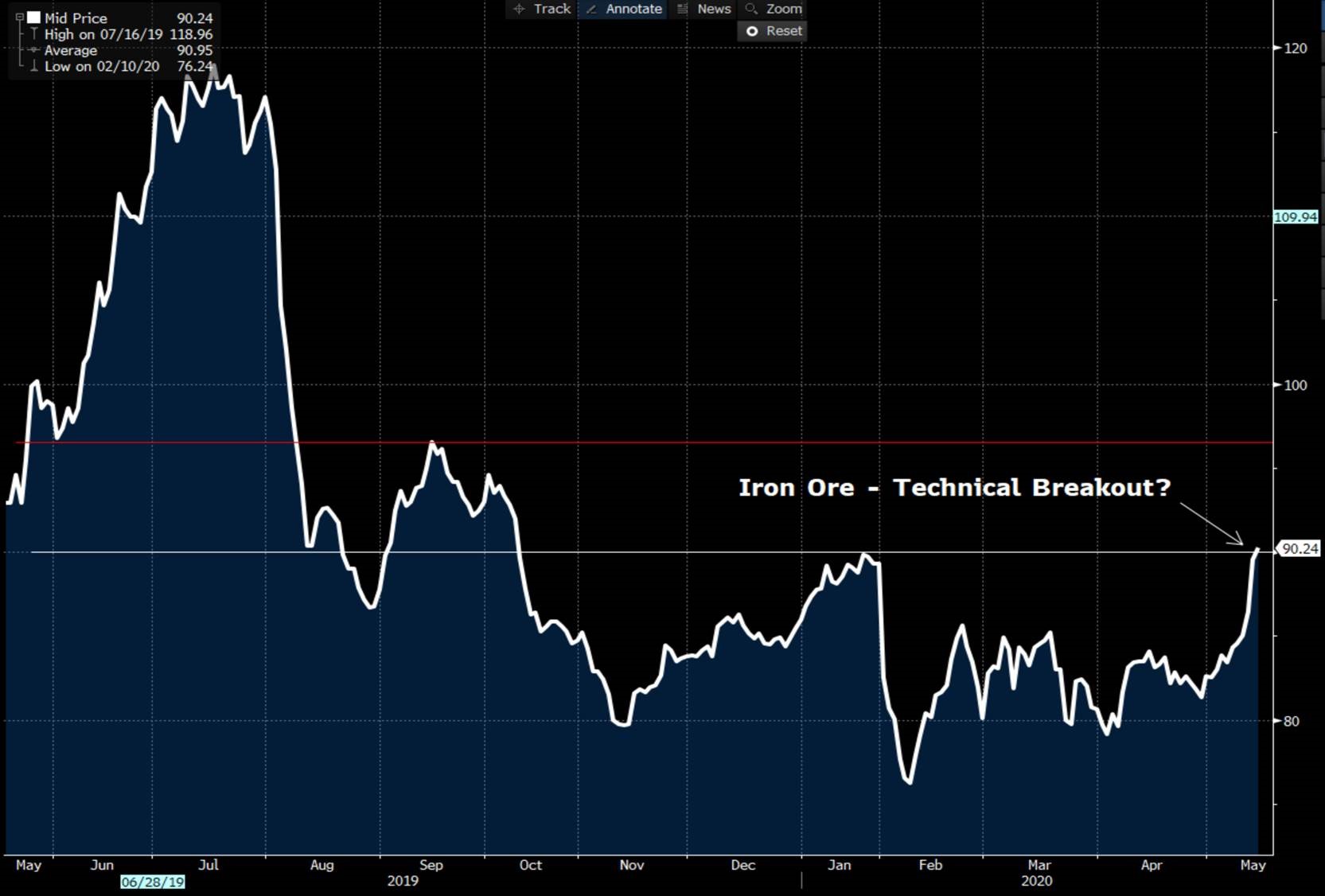

Raw materials are the foundation of steel making and, along with energy, are oftentimes the first indicator of a price move in the final product. Iron ore has confounded the skeptics through this entire pandemic, staying much higher than the bears felt was reasonable. And now, prices have not only just held in there but have ripped above $90/ton! China’s steel production has remained very strong – and in April, their production was up year over year, coming in at 85 million tons for the month (last April was just over 83 mmt).

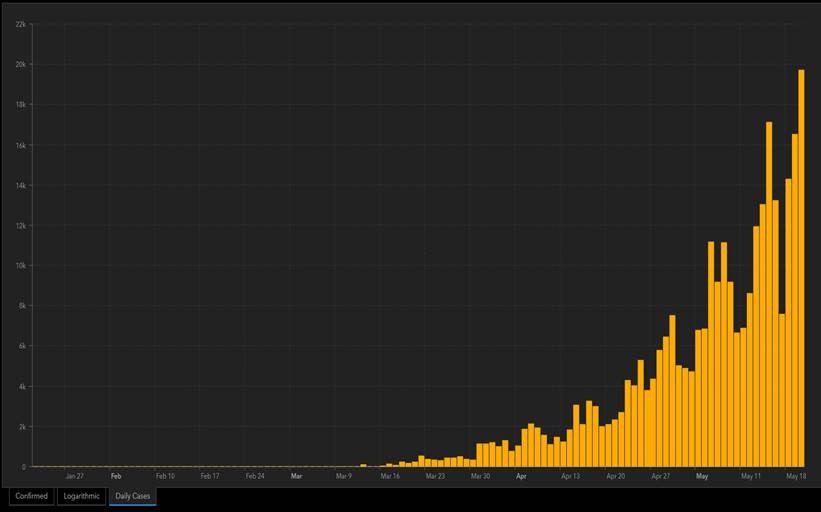

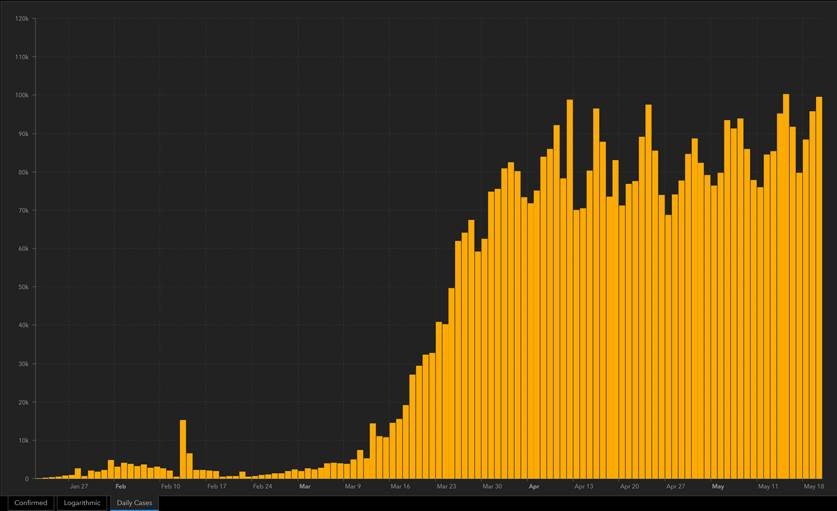

Not all data in China has supported a rapid recovery, but auto sales have come back almost to where they were pre-crisis, and oil refineries in China are operating at a 10-year high in terms of the utilization rate. Monthly construction starts there have moved from -35 percent at the peak of the virus crisis there to -8 percent y/y. And despite steel production being up year over year, inventories of HRC and rebar are coming down. In a nutshell, iron ore demand in China is strong, and supply side worries have emerged recently, which has added fuel to the fire. Brazilian virus cases have spiked, resulting in supply worries for ore. On the charts below, you can see the worsening situation in that country, while the world overall is showing an encouraging flattening in the curve.

Brazil: Daily New Virus Cases

Global: Daily New Virus Cases

All of this has led to an impressive recent rally in ore, as evidenced by the below chart.

In fact, the iron ore futures curve is now above where it was in January, before the virus impact hit!

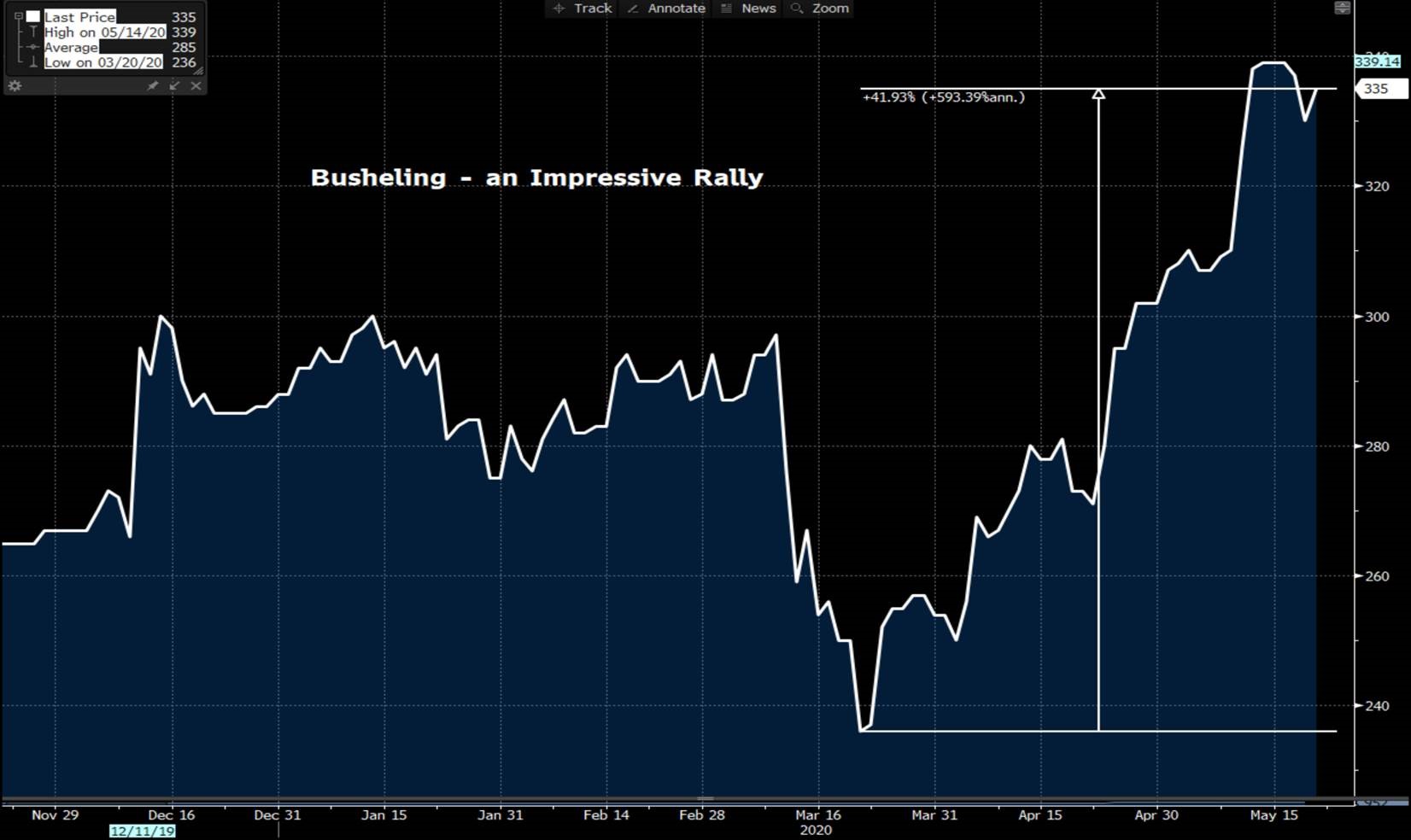

Bringing this back to the U.S., the busheling price has staged a stunning rally off the bottom in mid-March. In the case of scrap, it’s hard to make a case that this rally has a demand-driven component. Yes, many blast furnaces are offline, but EAFs here in the U.S. have also seen weak demand. It seems to be a supply-driven issue, caused by the drop in auto production to nearly zero in recent weeks.

The busheling curve (below) is now well above where it was “pre-virus.” Kind of amazing to see the strength here, and one has to wonder how supply and demand line up once we have restarts in the automotive and general industrial space.

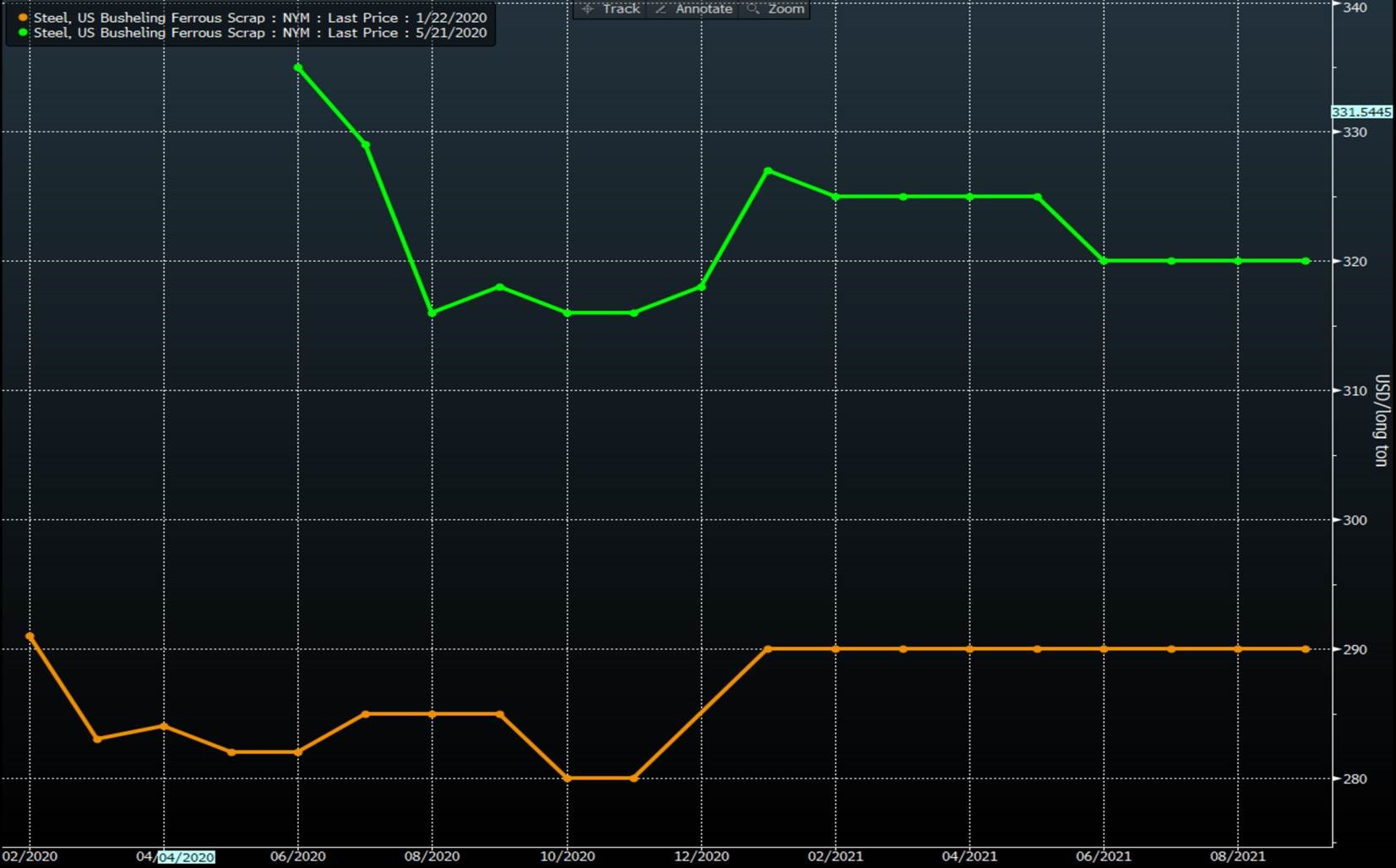

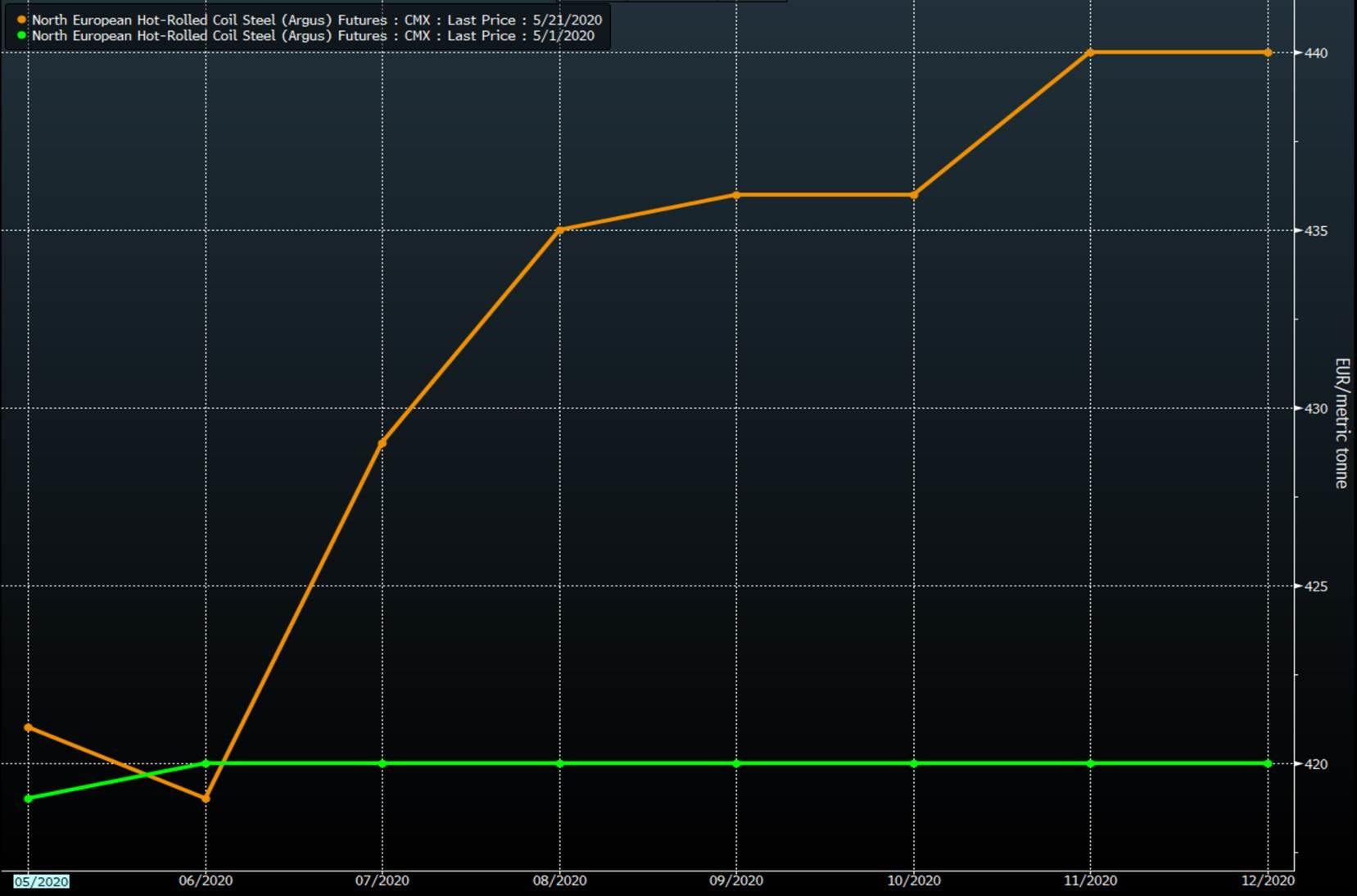

It is also notable that volumes on the busheling contract have doubled on a year-to-date basis as more parties become involved in trading futures. I’ll also mention the Northern European Steel contract, which has recently been launched. While volumes are small, the shape of that curve has taken on an interesting shape in recent weeks. On May 1, the contract was quite flat, but now has moved into a “contango,” with future prices being higher than spot. Market participants here seem to be thinking that prices will rise in the coming months in that region.

The futures markets have clearly exhibited some behavior that would have been pretty tough to predict, highlighting the need to reduce risks in your business that are beyond your control. Please stay safe and healthy, and we all look forward to some kind of return to normalcy!

Disclaimer: The information in this write-up does not constitute “investment service,” “investment advice” or “financial product advice” as defined by laws and/or regulations in any jurisdiction. Neither does it constitute nor should be considered as any form of financial opinion or recommendation. The views expressed in the above article by Metal Edge Partners are subject to change based on market and other conditions. The information given above must be independently verified and Metal Edge Partners does not assume responsibility for the accuracy of the information