Prices

June 11, 2020

CRU: Easing of Lockdowns Stabilizes Global Scrap Prices

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Metallics Monitor

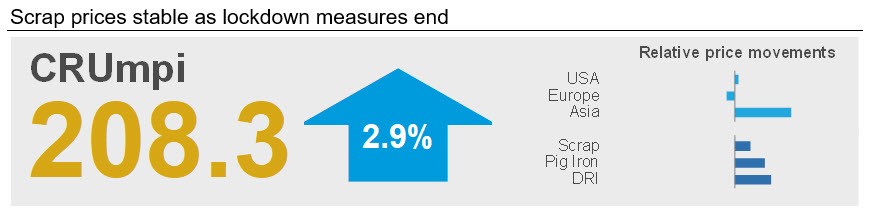

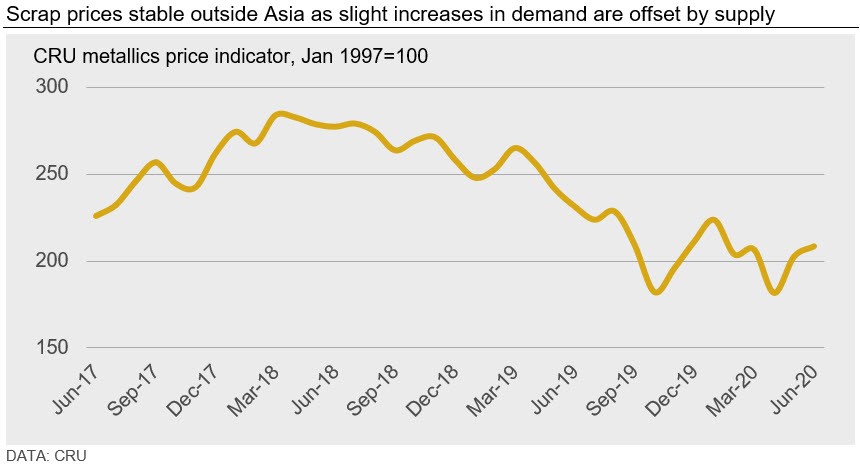

The CRU metallics price indicator (CRUmpi) increased slightly in June, rising by 2.9 percent m/m to 208.3. The reduction in lockdowns and other Covid-19-related restrictions across the globe allowed scrap to become more readily available as demand increased in major importing markets. In the near term, we expect that supply will begin to outpace demand in most markets given the limited probability of higher finished steel prices.

Scrap prices were broadly stable around the globe as more supply was made available by easing lockdown measures. In the U.S. and Europe, demand and supply mostly found a balance, although prime grade prices rose in the former and were weaker in the latter. In Russia, scrap prices fell after the country ended a national lockdown and favorable weather conditions supported collection. Meanwhile, Turkish mills were able to keep prices mostly unchanged m/m with supply becoming more plentiful. Other import markets in Asia had prices rise amid a strong demand-side recovery and limited supply.

U.S. obsolete scrap availability significantly improved in June as state governments reduced or ended Covid-19 containment measures. Peddler traffic increased substantially alongside demolition, and enough obsolete supply was made available that cut grade prices were little changed and shredded scrap prices fell by $10 /l.ton m/m. Prime grade supply was still somewhat limited after a slow recovery in manufacturing activity, so prices for #1 busheling rose by $10 /l.ton. Comparable price trends held true for nearly every region of the country, while Canadian producers reduced buying prices amid a surge in the Canadian dollar against the U.S. dollar.

A similar situation developed in Europe. While demand in both northern and southern Europe was still subdued from the pandemic, interest from Turkish buyers prevented an oversupply of E3 and shredded scrap. In Germany, E8 prices moved closer to obsolete grades given reduced demand from integrated mils. Further east, prices in Russia fell after the national lockdown there ended and mild weather conditions promoted the collection of scrap.

Scrap demand was strong in China despite the announcement of a weaker-than-expected stimulus package by the government. In addition to stronger demand, scrap became more attractive to steel producers because costs for iron ore are rising. Indeed, for both EAFs and BOFs, mills have returned to purchasing scrap at a more normalized level.

Major import markets in the rest of Asia also supported an increase in prices. Vietnamese demand continued to recover as construction projects resumed and scrap availability was relatively low. Meanwhile, exporters like Japan had domestic price increases because of weaker scrap collection and a higher steel demand from the construction sector.

In ore-based metallics markets, pig iron demand continued to be driven by interest from China even as traditional import markets stayed on the side lines. European producers have opted to buy HBI given its relative price competitiveness, while pig iron buyers in the U.S. reduced their purchased volumes. Still, prices for iron ore have risen and squeezed margins for pig iron producers. Taken together, China’s demand for ore-based metallics, alongside increased production costs from higher iron ore prices, resulted in prices for ore-based metallics rising m/m in June.

Outlook: Supply Likely to Outpace Demand in Most Markets

Supply in major exporting markets is returning quickly and we expect scrap prices to come under some downward pressure in the near term. Steel prices in North America and Europe are unlikely to rise soon given the restart of integrated mills, which will add more steel supply to an already weak market. In addition, because integrated mills do not require as much scrap as EAF operations, we expect that an increase in steel output will not result in much higher demand for scrap. As such, scrap supply is likely to outpace demand and result in lower prices.

We expect scrap prices in China to remain elevated relative to ore-based metallics. Therefore, China is likely to remain a major buyer in the international metallics market for the remainder of the year, which will keep pig iron prices high. However, upside potential will still be limited by lower prime grade scrap prices internationally.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com