Overseas

June 25, 2020

CRU: Long-Term Oil—Has Covid-19 Brought Forward Peak Oil Demand?

Written by Ross Cunningham

By CRU Senior Cost Economist Ross Cunningham, from CRU’s Steelmaking Raw Materials Monitor

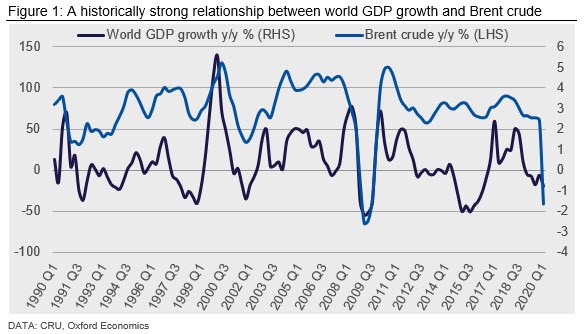

The Brent crude price is often deemed a bellwether for the global economy. A high oil price increases inflation and impacts economic growth. It influences global confidence, affects investment decisions and weighs on exchange rates—particularly those of large oil exporters. In the long-term our view is that peak oil demand will occur sometime in the mid-2030s. Technological efficiencies, the uptake of renewable energy, carbon tax schemes and electric vehicle (EV) penetration in the car market will be the main drivers of demand falling year on year at that time. Undoubtedly, the unprecedented impact of Covid-19 has changed the way we work, live and do business. Will these changes become a mainstay and have enough of an impact on the oil market to bring forward peak oil demand? This Special Feature sets out our view on long-term oil, the fundamental drivers of our price forecast and whether these have changed enough to alter our view.

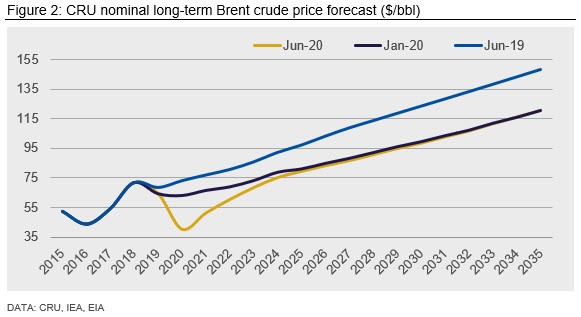

Our short-term Brent crude forecast is $40/bbl in 2020 and $51/bbl in 2021. Over this period the oil markets will be heavily influenced by market balance, sentiment and geopolitics. Our long-term outlook is anchored at $120/bbl nominal in 2035. We lowered our forecast from $148/bbl in 2035 in January 2020. In the long-term, our forecast is underpinned by assumptions about domestic resources, the uptake of technological advances and changes in global economic growth. Based on the scenarios we considered, the most plausible variants indicate a forecast range for Brent crude in 2035 between ~$60-$140 /bbl.

How We Construct Our Base Case

Our base case is constructed using our short-term (monthly reviewed) forecast for Brent crude aligned with an amalgamation of the reputable base case long-term forecasts of the U.S. Energy Information Administration (EIA) and the International Energy Agency (IEA). In the years 2021-2023, we control the rate of reconciliation (how quickly we align with the EIA/IEA consolidation) considering multiple factors. These include forecast supply and demand fundamentals, market sentiment and any impending regulations that may have an impact on oil price.

An In-Depth Look at Our Base Case

Our short-term forecast has changed significantly as a result of the impact of Covid-19. Late last year we expected moderate economic growth in 2020, a weaker U.S. dollar by H1 2020 and a surge in demand for distillate fuels due to the International Maritime Organization (IMO) 2020 regulation. Instead, Covid-19 has caused a global recession and the dollar remained strong in H1 as its safe-haven identity prevailed in times of such uncertainty. The demand for crude and refined products—particularly that of kerosene (for jet fuel), motor gasoline (petrol) and distillate fuel oil has imploded along with the prices. As for the effect of the IMO regulation, the price of very low sulphur fuel oil (VLSFO) is now similar ($30-40 spread) to that of IFO 380 bunker fuel, the high sulphur fuel that the regulation was meant to make redundant.

Covid-19 crippled global oil demand. As much as three-fourths of the world’s population has been in partial or complete lockdown. Commercial air travel became non-existent—many airlines have gone into administration or have needed government bailouts to remain in business. Road travel ground to a halt. Factories stopped producing goods as all non-essential businesses were forced to close. Supply chains were irreparably damaged causing ocean freight, rail and air travel to plummet. This combination caused crude oil demand to fall by more than 20 percent y/y in April and just under 20 percent y/y in May.

Despite having a cartel in place to keep the oil market balanced and prices reasonable, Saudi Arabia was involved in a price war with Russia in April and both nations along with other OPEC members increased production to keep their shares of a much reduced market. This toxic combination meant the industry was close to 25Mbbl/d over supplied in the month of April. Brent crude reached $16/bbl and U.S. WTI front month contracts traded at negative $49/bbl as storage capacity was close to reaching its limits. OPEC+ have since agreed a 9.7Mbbl/d supply cut until July (from an Oct. 18 baseline), with smaller (yet still very substantial) cuts to December of 7.7Mbbl/d, then 6Mbbl/d cuts until April 2022. These massive cuts will slowly deplete the large inventory build-up that Covid-19 demand destruction has caused. When we see evidence of such reduction, we will see the Brent crude price begin to recover to late 2019/early 2020 levels.

Beyond 2021, crude oil will continue to play a major role in global energy. We project global oil demand to grow by ~1 Mbbl/d each year to 2025, before average annual demand growth slows to around 0.25 Mbbl/d to 2035. We foresee China overtaking the U.S. to be the world’s largest oil consumer in the late 2030s. We expect strong demand growth in India and the Middle East. India will become a larger consumer of crude than the EU in the early 2030s.

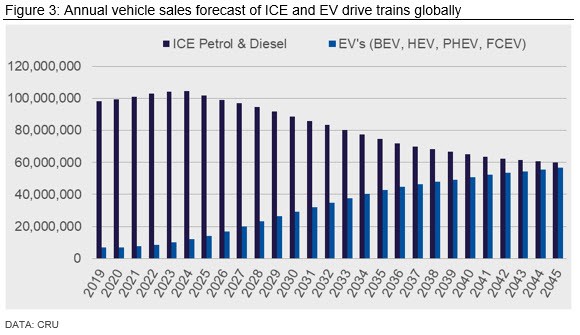

The use of refined oil products in cars is expected to peak in the mid-2020s even though the global car fleet grows by 80 percent to ~2 billion in 2040. While this may sound like a contradiction, it is the sharp uptake in electric vehicles that causes peak oil use in cars so soon. We expect electric vehicle sales to reach 56 million units per year by 2045, very close to what internal combustion engine (ICE) vehicle sales drops to over the same period.

Could Covid-19 Change Our View on Long-Term Oil?

In April, global crude demand fell by 21 percent y/y and in May 17 percent y/y, translating to an average of 14Mbbl/d oversupply for those months combined. To put it another way, more than 800Mbbls of crude were put into global storage in these months. For 2020, the EIA expects a reduction in demand of 5.2Mbbl/d compared to last year, and the IEA expects 9.3Mbbl/d less consumption. However, both institutions see demand returning close to 2019 levels next year. The EIA expects consumption to be 1 percent higher in 2021 compared to 2019 and the IEA 2.7 percent higher at end 2020 compared to end 2019. The question remains, could some of the demand destruction we have seen be permanent and bring peak oil forward from the widely believed mid-2030s? If demand does not recover completely, could 2019 be the year of peak oil demand?

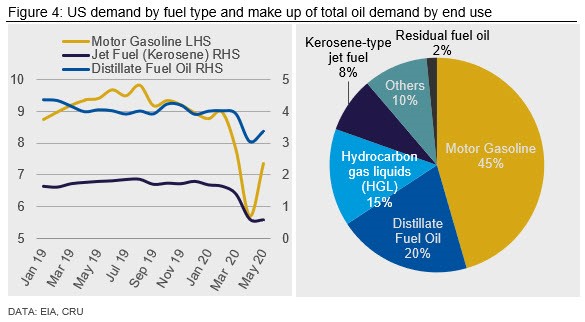

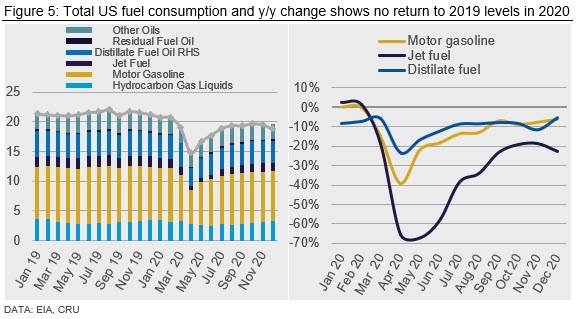

Covid-19 has caused major behavioral changes impacting oil demand. Hundreds of millions of daily commuters worldwide have been working from home. In the U.S., total fuel consumption has fallen from 21.3Mbbl/d in December to 14.8Mbbl/d—a fall of 30 percent across the board. Motor gasoline consumption fell 39 percent y/y in April. Jet fuel (or kerosene) saw an even sharper plummet in the U.S.; in April demand fell 65 percent y/y, as countries closed their borders and domestic flights were grounded. Alongside gasoline and kerosene, other end use fuel demand has been impacted by the virus. For distillate fuel oil (a general categorization for a variety of diesels and fuel oils) which makes up around 20 percent of total fuel, demand has dropped 23 percent y/y. Distillate fuel fared slightly better than kerosene and gasoline, because of how heavily it is used in industry. A core demand for distillate fuel has remained in the form of trucks, freight trains and the agricultural industry whose reliance on the fuel has proved relatively resilient, while use of diesel cars, public and school buses, public trains and generators used in non-essential industry has plunged.

Approximately 75 percent of oil demand in the U.S. comes from the three fuels highlighted above. Covid-19 has undoubtedly impacted their demand this year. Now that restrictions have started to be lifted, however, we have already seen motor gasoline and distillate fuel demand rebound, 29 percent and 11 percent m/m respectively. Unlike road travel, air has not seen a rebound in fuel consumption in May and will likely not return until new procedures are put in place for air travel. Furthermore, it may take some time for the public to return to the skies. We could see a spike in motor gasoline demand as people opt to pack up their cars and holiday domestically instead. The EIA expects jet fuel demand to not return to 2019 levels until beyond 2021. The EIA forecasts distillate fuel to follow motor gasoline demand and return to 2019 levels near the end of 2020 and early 2021.

In a post Covid-19 world, employees’ decisions to work from home more frequently will reduce commuter miles and inherently lower demand. People’s decision to not travel by plane for vacation, opting instead to stay domestically, will lower crude demand. The backlash against globalization from the virus bringing production and supply chains closer to market will similarly lower crude demand. But these reflect small changes to the crude oil market. Built into the long-term forecast for oil and the date of peak demand are the implementation of new technology, efficiencies, and the adoption of EVs in the global car market.

Efficiency improvements in ICE engines are evident in U.S. oil demand. The highest level of U.S. oil demand to date was back in 2005 at 20.8Mbbl/d. Despite the U.S. population growing by 20 million people over 2005-19, and vehicle miles travelled (VMT) increasing by nearly 10 percent from 8.2bn miles a day in 2005 to 9bn miles a day in 2019, U.S. oil consumption in 2019 was still below the 2005 level. The increases in population and VMT were outweighed by greater vehicle efficiency. As these efficiencies gradually infiltrate developing countries, the trajectory of demand growth will slowly flatten.

The largest impact on crude demand and the inevitability of peak oil demand comes from EV penetration around the world. As indicated earlier, CRU expects EV sales to approach 60 million units in the mid-2040s—48 percent of total car sales worldwide. An estimated 21.5Mbbl/d of the ~100Mbbl/d of global oil demand comes from cars. As ICE engine efficiencies reach developing countries and EVS penetrate the car market at very ambitious target rates set out by the main consumers—China, India and Europe the amount of crude consumed by cars in 2040 will be similar to that of today. Even as car numbers rise by ~80 percent.

The Further We Look, the More Uncertainty Arises

Global economic growth will result in an increase in oil demand. However, as we reach the mid-2030s efficiencies in engine technology, EV penetration in the global car market, carbon tax schemes and renewable energy profitability will bring the age of peak oil demand. Covid-19 has had some large effects on the oil market. While some practices will change (more working from home, less international travel, anti-globalization sentiment and rising green climate activism) the fundamental drivers impacting the largest parts of oil end use will have a much larger impact on peak oil demand. Our Brent crude forecast is $120/bbl in 2035 and $162/bbl in 2050. Inevitably, forecasting two decades ahead will always involve many uncertainties. The real value of this feature lies not in trying to predict the future, but in providing a structure and discipline to our thinking and analysis, allowing us to build a better rationale for forecasts to 2035 and beyond.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com