Overseas

August 14, 2020

CRU: Global Steel Price Uptrend Resumes

Written by Josh Spoores

By CRU Principal Analyst Josh Spoores, from CRU’s Steel Monitor

Steel markets have recovered from the depths of Covid-19 global disruption, but this has varied in pace across regions and has been stop-start in many. Indeed, as measured by CRU’s global finished steel CRUspi, finished steel prices bottomed in May at 129.3, the lowest reading since October 2016. This index then increased in June before falling in July. In August, the CRUspi rebounded to 144.4, its highest reading since April as strong m/m price gains in Asia were joined by a measured increase in Europe. In North America, prices fell back in August for the second consecutive month.

Price strength in Asia has been largely influenced by the government-led stimulus enacted in China. This led to increased domestic demand in China, which in turn restricted Chinese exports to regional markets. The knock-on effect of this stimulus has therefore been higher steel prices, primarily sheet, in markets where China is often a significant exporter such as the rest of Asia as well as markets further out, including Brazil. Because of higher-priced Chinese exports, markets such as India and even Europe have been able achieve higher export prices and volumes than they would otherwise, and this in turn has brought some balance to each respective home market.

While the overall rebound in global steel prices has not been consistent across all markets, it also has been more beneficial towards sheet products versus longs. China has again played a role here where seasonal factors such as the rainy season as well as recent policies targeting the real estate sector have limited longs products demand from construction earlier this summer. Meanwhile, China’s stimulus did have an outsized effect on key manufacturing sectors such as automotive and appliances, which supported sheet products. Further detail on China and the other regions can be seen by subscribers in the latest Weekly Covid-19 Steel Market Update available here.

Longs: Demand Recovery Slows on Seasonal Weakness

The Global Long Products Price Indicator (CRUspi Longs) increased by 1.2 percent m/m to 155.7 in August. Price rises in Asia offset weakness in both U.S. and German markets.

Long products prices have moved in different directions between eastern and western markets. Market sentiment remains positive after recent seasonal weakness in China, yet is poor elsewhere as non-Chinese markets continue to experience an uneven recovery from the economic damage doled out by Covid-19 containment efforts.

Sheet: Chinese Stimulus Supports Global Sheet Prices

Global sheet prices increased from July, yet m/m price changes varied significantly across regional markets. CRU’s Global Flat Products Price Indicator (CRUspi Flats) has captured the overall trend. It increased by 3.1 percent m/m to 138.8— close to its April level—yet was still down 8.9 percent y/y.

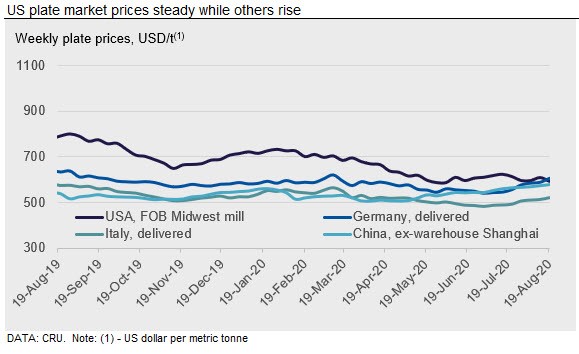

Though sheet prices were higher m/m, these gains varied by market. Prices in Asia, primarily China and East Asia, were supported by a strong recovery in China. In Europe, sheet prices have only recently begun to slowly move off the lows in early July. Finally, prices in the U.S. sheet market returned to their Q2 bottom as inventory throughout the supply chain corrected to levels that are now more in line with recent demand.

Outlook: Further Near-Term Price Gains to Materialize with Assistance from Steelmaking Costs

Global finished steel prices will continue to rise over the near term, though gains will continue to favor individual markets and products. China is entering a period of peak seasonal demand, which will continue to support sheet prices more than longs products. However, high capacity utilization levels as well as inventories may ultimately limit the upward extent of further price gains.

Demand improved for longs products in the northern hemisphere as delayed and recently started construction projects continue ahead of winter. As for sheet markets, rising demand from both the economic recovery as well as seasonal factors will support sheet prices, with stronger gains expected in North America and Europe versus the East Asian markets.

Steelmaking raw materials will continue to provide further support to finished steel prices, especially if iron ore and global metallics prices remain supported by strong steelmaking demand in China.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com