Analysis

August 21, 2020

CRU: U.S. Sheet Exports to Mexico Resuming

Written by Eduardo Tinti

The latest CRU Global Economic Outlook indicates that Mexican auto production will not reach 2019 levels until 2023, with expectations that 2020 volumes will be down about 23 percent in 2020 and recover 19 percent in 2021. There is some near-term upside to the Mexican market as production returns to normality after the Covid-19-related shutdowns, which is benefitting U.S. steel sheet exporters.

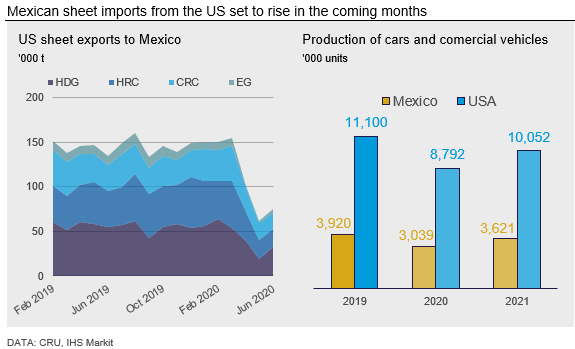

The pandemic-driven slump in Mexican auto production led to a sharp reduction in the country’s steel sheet imports from the U.S. (see chart). Auto production in Mexico was nil in April and May. As a result, U.S. sheet steel exports to Mexico were 58 percent lower y/y in May. From June, Mexican auto production started to resume and contributed to a pickup in sheet imports from the U.S. Such a support to U.S. exports is expected to continue in the near term as, in July, Mexican auto production was reported higher y/y and anecdotal evidence suggests that August output is back to February levels.

The auto sector recovery in the U.S. and in Mexico is expected to continue, but according to our estimates, 2020 vehicle production will off just over 20 percent in the U.S. and Mexico. The recovery is expected to continue through 2021 but will not be enough to offset 2020 losses as we estimate 2021 auto production in both countries still 8‑9 percent below 2019 levels.

HDG exports to Mexico fell more significantly than other sheet products since April. In 2020 Q2, HDG exports to Mexico fell by 48 percent y/y, the equivalent to 83,000t, according to IHS Markit data. However, it was also the product group that presented the most relevant recovery in June, lifting by 70 percent m/m.

Meanwhile, the U.S. market has also seen rising HDG imports from Brazilian producers who took advantage of the depreciated currency to partially offset the difficulties faced in the pandemic-hit domestic market by lifting export volumes. Brazil has now filled all its HDG import quotas to the U.S. under Section 232 and, therefore, imports from the country will not continue for the remainder of the year. High Brazilian HDG exports to the U.S. from Brazil may not resume in 2021 either because of expectations that the Brazilian economy and its currency value will recover somewhat.

On the other hand, U.S. CRC exports to Mexico were the least severely hit by the pandemic among sheet products. Even so, in 2020 Q2 CRC exports to Mexico fell by 34 percent y/y, the equivalent to 32,000t. Unlike HDG, though, CRC exports have not yet picked up and were still down m/m in June.

Despite the gains in HDG exports, overall sheet exports to Mexico represent a small share of U.S. production. Therefore, the Mexican recovery is not expected to have major effects on U.S. domestic prices. Moreover, despite the pickup from April and May lows, the Mexican auto sector is not forecasted to have a sustained growth path in the months ahead. Developments related to the pandemic may jeopardize and delay the Mexican recovery further as the country currently has the fourth largest number of new daily confirmed deaths because of Covid-19.

Mexican sheet imports from the U.S. are set to rise in the coming months

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com