Market Data

October 15, 2020

CRU: China’s Reported Ban of Australian Coal Imports

Written by Ben Carstein

By CRU Analysts Ben Carstein and Lize Wan

On Oct. 9, it was reported that Chinese state-owned power plants and steel mills had received verbal notice from China’s customs to stop importing Australian metallurgical and thermal coal with immediate effect. In this article, we review the announcement and its potential implications.

Has the Announcement Been Confirmed?

Coal import restrictions have been sporadically implemented in China since 2018. However, the latest announcement has unsurprisingly garnered a lot attention, particularly given the potential implications for Australian coal producers, trade flows and prices generally. We have spoken to several industry contacts within China who have said they were aware of the latest news, but none had personally received this notice. While there is some ambiguity around what has been announced, and it has not been possible to formally verify it, our sources do believe that the notice has been made. Further, when asked about the reports of an Australian coal ban, Chinese customs spokesman Li Kuiwen responded that customs authorities will “further strengthen import supervision on related goods,” both not denying the reports and implying stricter import controls.

What is Behind the Announcement?

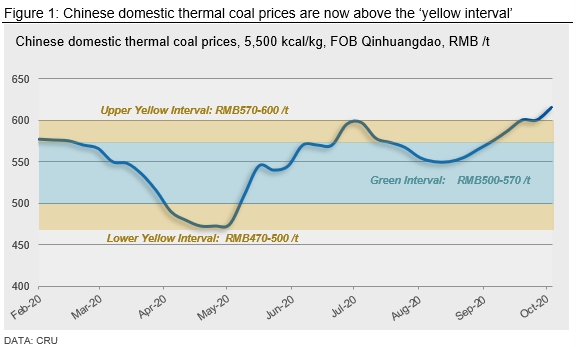

Given the current strength of Chinese domestic thermal and metallurgical coal prices and the overall tightness in the Chinese domestic thermal coal market, a new restriction on imports runs contrary to our expectations and is difficult to explain. This is particularly true given that import orders made today would go towards 2021 import quotas, as opposed to already filled 2020 quotas. As an example, Chinese domestic thermal coal prices are now above the government’s “yellow interval” range, with domestic supply constrained by mining permit and safety checks and falling port stocks just as the country approaches the peak winter heating season demand period. This points to the need for increased imports to meet domestic requirements, rather than further restrictions.

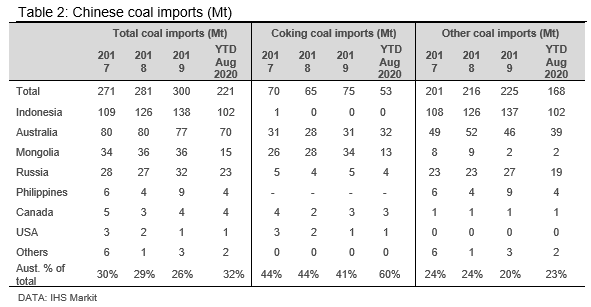

Australia typically accounts for ~40% of Chinese coking coal imports and ~20% of Chinese thermal coal imports and the strong year-to-date performance of imports from Australia, as well as the expectation of rising import demand going into 2021, will be a factor in this announcement. Further, whether deliberate or not, this announcement has the effect of dampening sentiment and prices in the seaborne market just as Chinese import demand is picking up.

While there are no official figures for annual Chinese coal import quotas, we believe prior year levels can be used as a guide to quota levels in the current year. Imports from Australia were very strong in 2020 H1 due to temporary Covid-19 disruptions to domestic coal production and Mongolian exports. In fact, year-to-August Australian coking coal imports are already above annual levels for 2019. Further, year-to-August total coal imports from Australia were 70 Mt, compared with 77 Mt for 2019, and are on track to surpass 2019 levels by October. In addition, while the overall figure for Chinese coal imports year-to-August from all countries is 221 Mt, and below 2019’s level of 300 Mt, after taking account of reporting delays, as well as vessels currently waiting to be unloaded, it is likely that China has already reached its annual import quota for 2020.

As a result, excluding any possible geopolitical factors, it is plausible that a desire to constrain imports going into 2021 is a factor for the announcement.

Implications of a Ban on Coal Imports from Australia

In response to the announcement, both seaborne metallurgical and thermal coal spot prices have fallen (n.b. premium hard coking coal, FOB Queensland, is down $7 /t and 5,500 kcal/kg thermal coal, FOB Newcastle, is down $2.5 /t from a week ago), while Chinese domestic prices remain supported, resulting in a further widening of the import arbitrage. In addition, the risk premium for Chinese buyers importing Australian coal has further increased, meaning that Chinese buyers will be seeking substantial discounts to justify purchases from Australia. Indeed, a thermal coal buyer told us that, given the announcement, their Australian coal purchase plan had been suspended and they will prioritize imports from other countries.

Imports from Australia represent a relatively small share of overall Chinese consumption, at 2% for thermal coal and 5% for coking coal. If the ban is fully enacted, China firstly could rely on its domestic coal resources that, while not as high quality as Australian coal and higher cost than current seaborne prices, are sufficient to meet Chinese requirements.

From the import market, at 20% of total imports, Australian thermal coal will be easier to substitute than coking coal, which represents 40% of import requirements. Mongolia can offset some Australian metallurgical coal supply. However, it could not expand at a rate to fill the gap. Indeed, we have already heard reports of Chinese buyers turning to Mongolian supply in response to the announcement. Further, Russia stands to benefit both in terms of metallurgical and thermal coal exports, however, again, given infrastructure constraints in Eastern Russia, we do not expect them to be able to fully offset any gap in Australian supply in the near term. Indonesian thermal coal exports to China could also increase, however, on quality grounds, buyers would likely prioritize Russian coal, followed by Columbia and South Africa, although the latter two sources face a freight disadvantage.

As a result, if fully implemented, the ban on imports from Australia will result in:

- Discounts for Australian coals to either justify the risk for a Chinese buyer to purchase Australian material or to reallocate material to a buyer in a different country.

- A change in trade flows, whereby Chinese imports of Australian coal will need to be substituted by Russian, Mongolian, Indonesian, Colombian, South African or U.S. material. This, in turn, means that imports from these countries to other markets, such as Japan, India and the rest of Asia, will need to be replaced by Australian material.

- Higher Chinese domestic coal production and prices, where the loss of Australian supply for Chinese buyers cannot be effectively met by alternative sources of imports

- Continued large differentials between Chinese and seaborne prices that, in turn, will disadvantage the cost competitiveness of the Chinese steel and power industry.

As already mentioned, coal import restrictions have been sporadically implemented in China since 2018, however, the recent announcement could have a further material impact on the seaborne market, particularly for Australian producers. Having said that, the announcement has not been officially confirmed and remains ambiguous. As such, we will continue to monitor for further information and will update clients accordingly.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com