Prices

October 15, 2020

CRU: U.S. Zinc Demand Stable This Month

Written by Helen O’Cleary

By CRU Senior Analyst Helen O’Cleary

The U.S. economy saw an impressive overall rebound through Q3, following severe Covid-19 disruption in Q2. We estimate that U.S. industrial production contracted 7.5% y/y in Q3, following a decline of 14.4% y/y in Q2. However, the momentum of the recovery is slowing as fiscal stimulus and the effects of pent-up demand wane. We currently do not expect Congress to agree on another stimulus package before November’s election, and our base case is for additional stimulus in 2021. In terms of the zinc market, we continue to hear that U.S. demand is gradually improving, with consumers generally taking contract volumes and starting to plan for 2021, although flexibility is likely to be key in next year’s contracts given the high level of uncertainty in the market.

U.S. steel mills have continued to see better levels of demand this month as end-use orders from the automotive sector have continued to improve and inventories have been rebuilt. We understand that most mills are taking their contract volumes, with no significant deferrals reported this month. Overall, this has been taken as a positive sign by the market and the recovery in steel mill demand is expected to continue throughout the remainder of the year. We estimate that U.S. steel sheet output contracted by 31.4% y/y and 30.1% y/y, respectively, in Q2 and Q3 and forecast a less severe contraction of 10.3% y/y in Q4. HDG coil prices have also remained stable over the past few weeks, rising in early October before coming off slightly this past week.

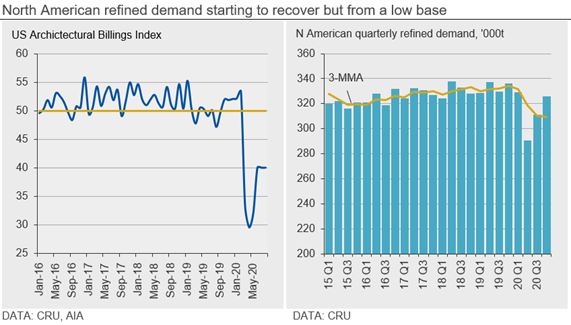

We understand that demand from general galvanizers has continued to be stable over the past month, having remained far more robust than demand in other sectors throughout the pandemic. Covid-19 disruption has had little impact on residential housing, and we expect starts to be 0.8% higher in 2020 than in 2019. Commercial construction has taken more of a hit, with the U.S. Chamber of Commerce Commercial Construction Index remining far below pre-Covid-19 levels in Q3. The forward-looking AIA Architectural Billings Index remained in contraction in August for the sixth consecutive month. Again, commercial construction was highlighted by the AIA as a point of weakness and it noted that the ongoing pandemic has impacted the number of proposals becoming active projects. A key risk is that delayed and cancelled projects in the U.S. will impact end-use zinc demand in coming months.

North America Refined Production Has Been Strong in 2020

Overall, North American smelter output has been strong this year, especially in H2. We estimate that output increased 4.6% y/y in Q2 and 14.7% y/y in Q3, despite weaker Q2 output from Peñoles’ Torreon smelter in Mexico and concentrate market tightness in Q3. This strong Q3 forecast assumes that Peñoles will increase output in line with their expanded capacity and that AZR will be producing as expected. We understand that the latter was having some issues earlier in the year regarding the quality of refined zinc produced, but these issues have now been overcome. We still have a 4% ex-China smelter disruption allowance in Q3 to capture the risk posed by Covid-19 disruption to mine supply. We forecast that in Q4, North American smelter output will increase by 10.5% y/y.

U.S. refined imports remained strong in August, increasing 40.6% y/y and bringing the year-to-date increase to 19.1% y/y. Imports from Canada and Peru declined 8.3% y/y and 16.8% y/y, respectively, in January-August, yet these losses have been more than offset by higher imports from Mexico, Brazil, Spain and Belgium with 20,000 t coming from Spain in July and 24,000 t from Belgium in August. We have not heard of any tightness in the U.S. market over the past month, and we understand there is plenty of refined metal available. There have been only a handful of spot deals reported to us over the past month and we have kept our assessment of premia flat at 7.5 c/Ib.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com