Market Data

January 8, 2021

Consumer Confidence Falls Further in December

Written by David Schollaert

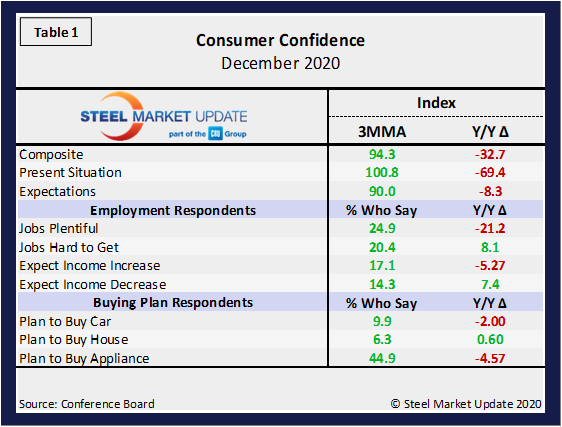

U.S. consumer confidence continues to fall as global pandemic fatigue sets in and genuine relief still seems far away. Despite a slight correction and stability throughout the summer months, the composite value of consumer confidence, reported by The Conference Board, has now slipped repeatedly during the fourth quarter from 101.8 in September to 88.8 in December. The three-month moving average (3MMA) fell to 94.3 in December compared to 98.5 in November. The 3MMA dipped notably from the recent high of 130.4 in February and 127.0 year over year. Since this indicator is quite volatile, the moving average is used to reduce monthly variability; however, consumer confidence is clearly on a downward move entering 2021.

“Consumers’ assessment of current conditions deteriorated sharply in December, as the resurgence of COVID-19 remains a drag on confidence,” said Lynn Franco, Senior Director of Economic Indicators at The Conference Board. “As a result, consumers’ vacation intentions, which had notably improved in October, have retreated. On the flip side, as consumers continue to hunker down at home, intentions to purchase appliances have risen. Overall, it appears that growth has weakened further in Q4, and consumers do not foresee the economy gaining any significant momentum in early 2021.”

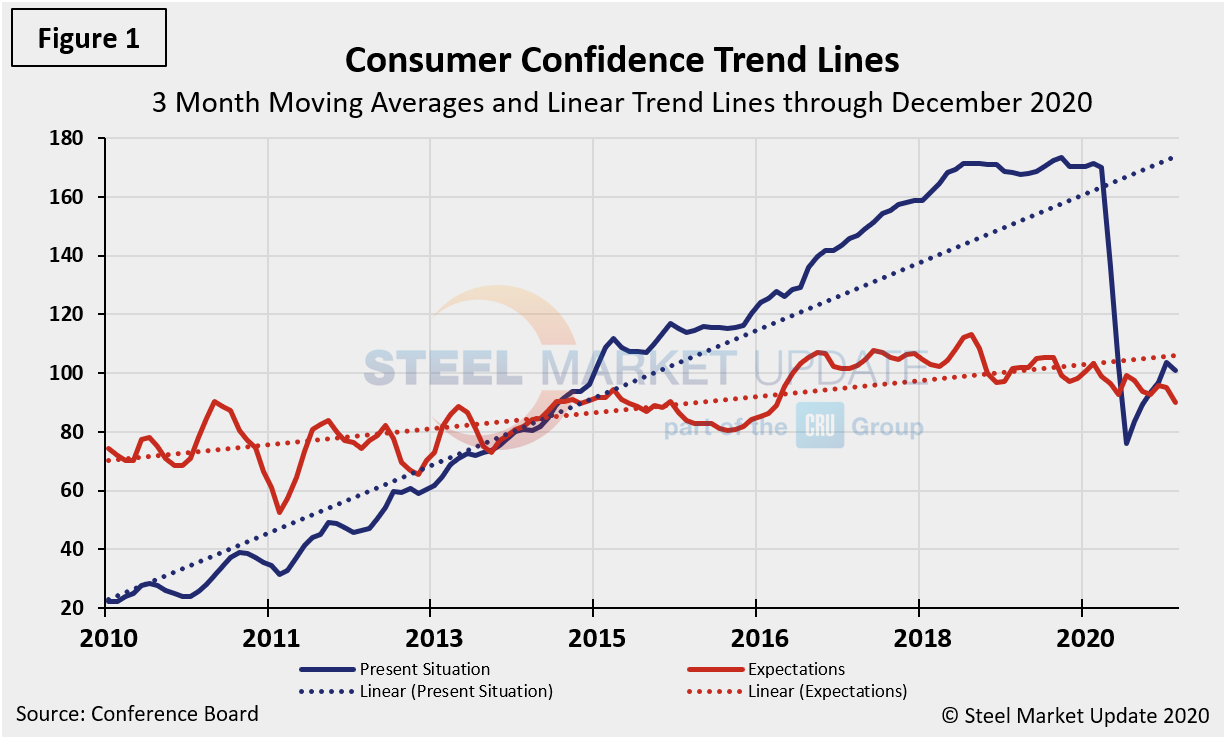

The composite index is made up of two sub-indexes: the consumer’s view of the present situation and his or her expectations for the future. Figure 1 notes the 3MMA linear trend lines from January 2010 through December 2020. Despite the present situation suffering from COVID-19, the market is still poised to rebound.

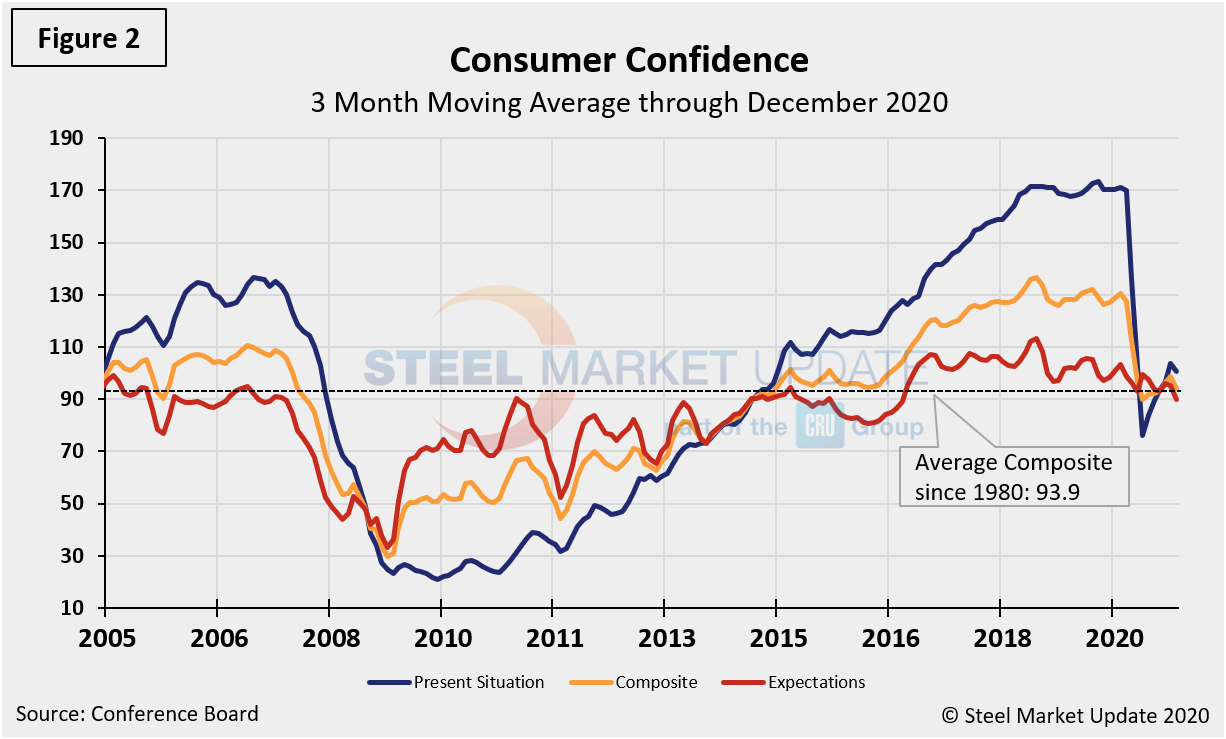

The 3MMA of the consumer’s view of the present situation dropped from 171.2 in February to 76.0 in June, but subsequently recovered to 106.2 in October. Since then it has dropped by 15.9 points to 90.3 in December. Expectations were less dramatically affected by the pandemic and declined from 103.2 in February to 92.9 in May, though rebounding and holding in the mid-90s through November. Expectations fell by nearly 6 points in December, also on a 3MMA basis. Figure 2 shows the trend lines of both subcomponents. The view of the present situation has edged back up after collapsing below trend, but expectations are now below trend and are projected to fall further in the near-term (Figure 2).

On a 3MMA basis comparing December 2020 with December 2019, the present situation was down by 69.4 points and expectations were down by 8.3 points (Table 1). The consumer confidence report also includes both employment data and some purchase plans and these are summarized in Table 1. The color codes show improvement or deterioration of the individual components. Although they remain positive on a 3MMA basis, they are all on a downward move, while year-over-year results are noticeably down across most markets.

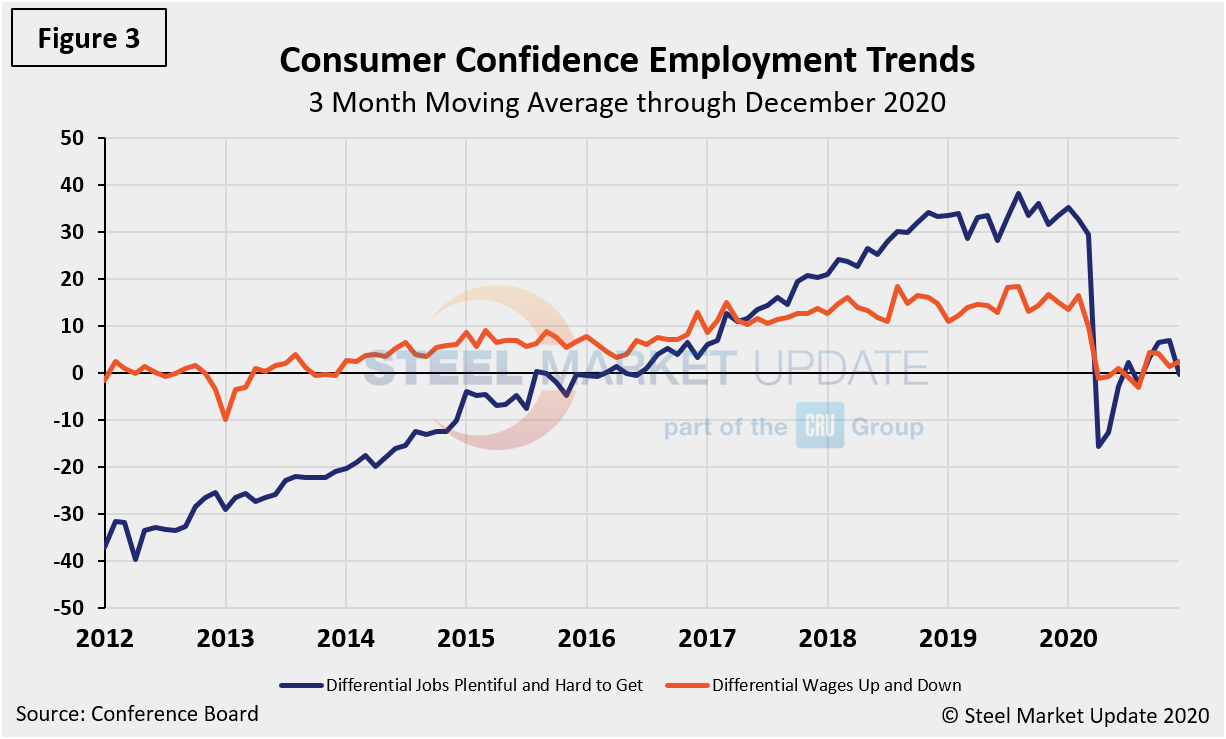

In December last year, the differential between those finding jobs plentiful and those having difficulty was positive 33.5. As a result of the pandemic, it fell to negative 15.7 in April. Despite some improvements since, it has dropped 7.4 points month on month to a negative 0.2 in December (Figure 3). Expectations for future wage change were similarly affected. In December last year, the differential was positive 15.1 and in December of this year was positive 2.5.

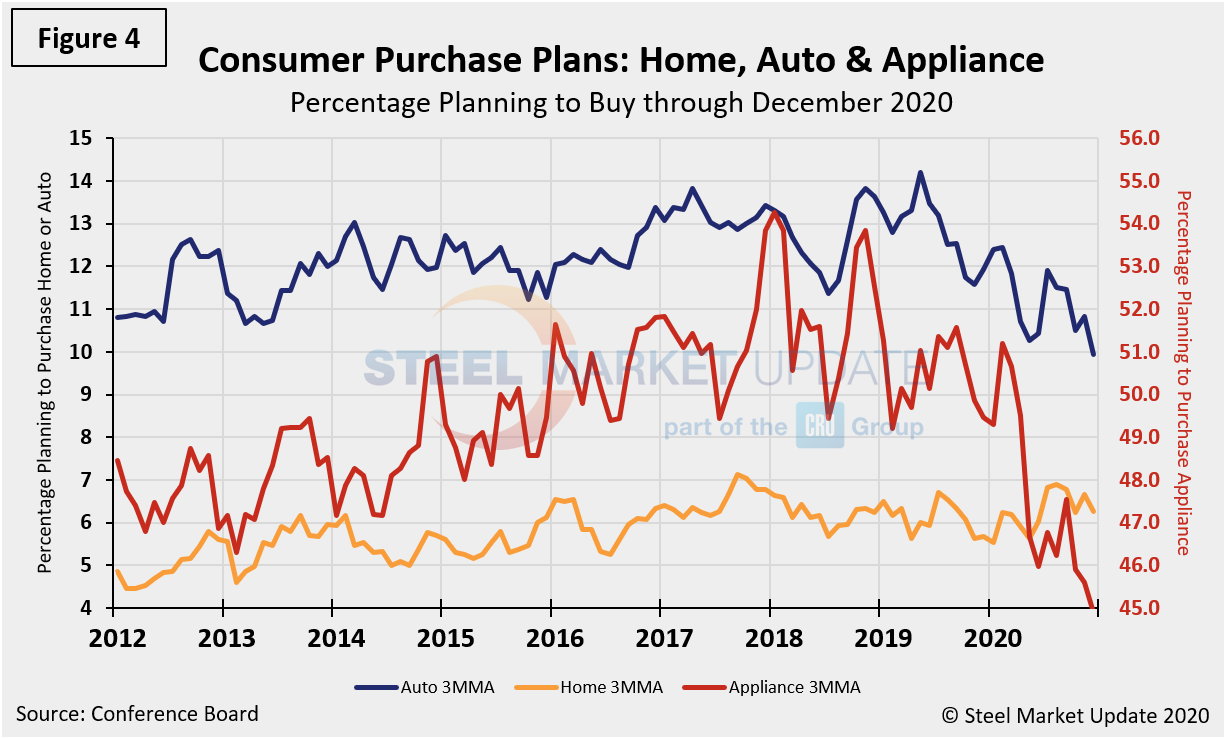

The trend across spending plans for consumer goods as measured by automobiles and appliances has seen a similar outcome; some positive improvements were seen over the summer months, yet they are still behind pre-pandemic levels (Figure 4). These results continue to indicate that buyers are still largely taking a cautious approach when spending on consumer goods. Automobiles and appliances registered a negative 2.0 and negative 4.6, respectively, compared to the year prior, while home buying reported just a marginal positive result of 0.6 year over year.

SMU Comment: Consumer confidence is still lagging behind year-ago levels, as expected, due largely as a response to the global pandemic. As questions surrounding the impact Covid-19 may have over the winter months, overall sentiment has edged down over the past couple of months after some steady improvement throughout the summer. Even though consumer confidence has been a bit shaky of late, steel prices continue to rise due to steady demand and tight supply. Improved consumer confidence, albeit tempered, has aided the recovery seen in steel demand, which is dependent on the growth of GDP and consumers’ willingness to spend. Consequently, should consumer confidence continue to edge down, that may contribute to a coming reversal in steel prices. Consumer confidence should be treated as a leading indicator in steel industry corporate planning.

About The Conference Board: The Conference Board is a global, independent business membership and research association working in the public interest. The monthly Consumer Confidence Survey®, based on a probability-design random sample, is conducted for The Conference Board by Nielsen. The index is based on 1985 = 100. The composite value of consumer confidence combines the view of the present situation and of expectations for the next six months.

By David Schollaert, david@steelmarketupdate.com