Market Data

January 18, 2021

December PPIs Show Overall Growth Across Sectors

Written by David Schollaert

This report is an analysis of Bureau of Labor Statistics (BLS) data and is intended to provide subscribers with a view of the competitive positions of sheet steel, aluminum, plastic and wood. The analysis includes some downstream products and a comparison of truck and rail transportation.

On Jan. 15, the BLS released its series of Producer Prices Indexes for more than 10,000 goods and services through December 2020. For an explanation of this program, see the end of this piece. The PPI data is helpful in monitoring price direction as there is a lag between the BLS reports and spot prices for steel products. The actual index values of the PPIs of different products cannot be compared with one another because they are developed by different committees within the BLS, but are useful in comparing the direction of price changes in the short and medium term.

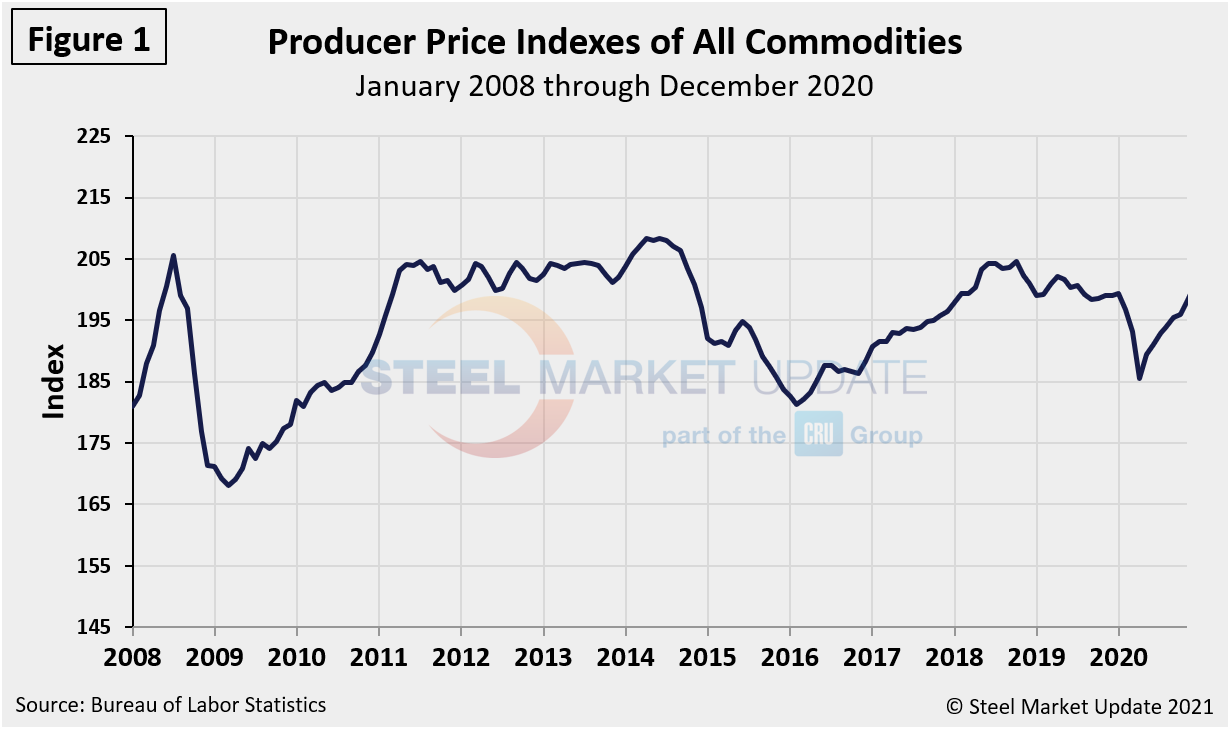

Figure 1 shows the composite PPI of all commodities since January 2008. The index has seen some noteworthy peaks and valleys over the past six years. Following a steady and at times sharp fall for two years through early March 2016, the index rebounded and rose steadily for two and a half years through October 2018. The upward move didn’t last as it tumbled by 4.0 percent through February 2020 with an acceleration through April, when the bottom was reached. The final demand increased 0.3 percent in December, seasonally adjusted, according to the BLS. This rise followed repeated increases through Q4 2020 with advances of 0.1 percent in November and 0.3 percent in October.

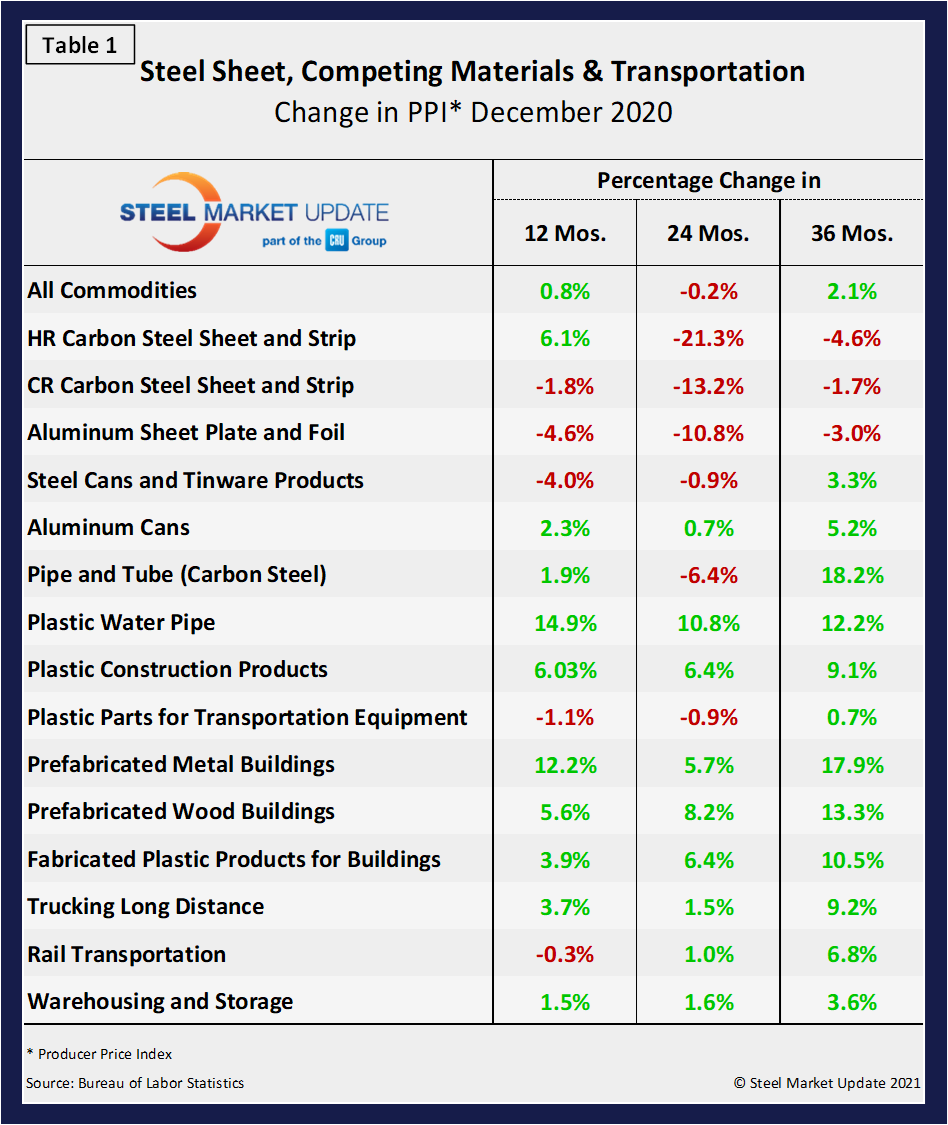

Table 1 is a summary of each segment that we examine on a year over one-, two- and three-year basis. The gain/loss pattern is shown by the color codes; we interpret rising prices as positive. We began this bi-monthly analysis in January 2016 and the table was predominantly green at the 24-month and 36-month level through September 2019. Since December 2019, eight of the 16 sectors had been in decline at the 12-month level. There was a turn that began in late third quarter, however, which has seen 14 of the 16 sectors report steady gains, with 11 of those now on a positive scale to close out the year. The table includes direct comparisons where possible between steel and competing products, some other plastic products for which there is no direct steel comparison, and a measure of price changes for transportation, warehousing and storage. Some specific comparisons of steel and steel products with their competition are as follows. Please note the Y axes on Figures 3 through 7 are not to the same scale.

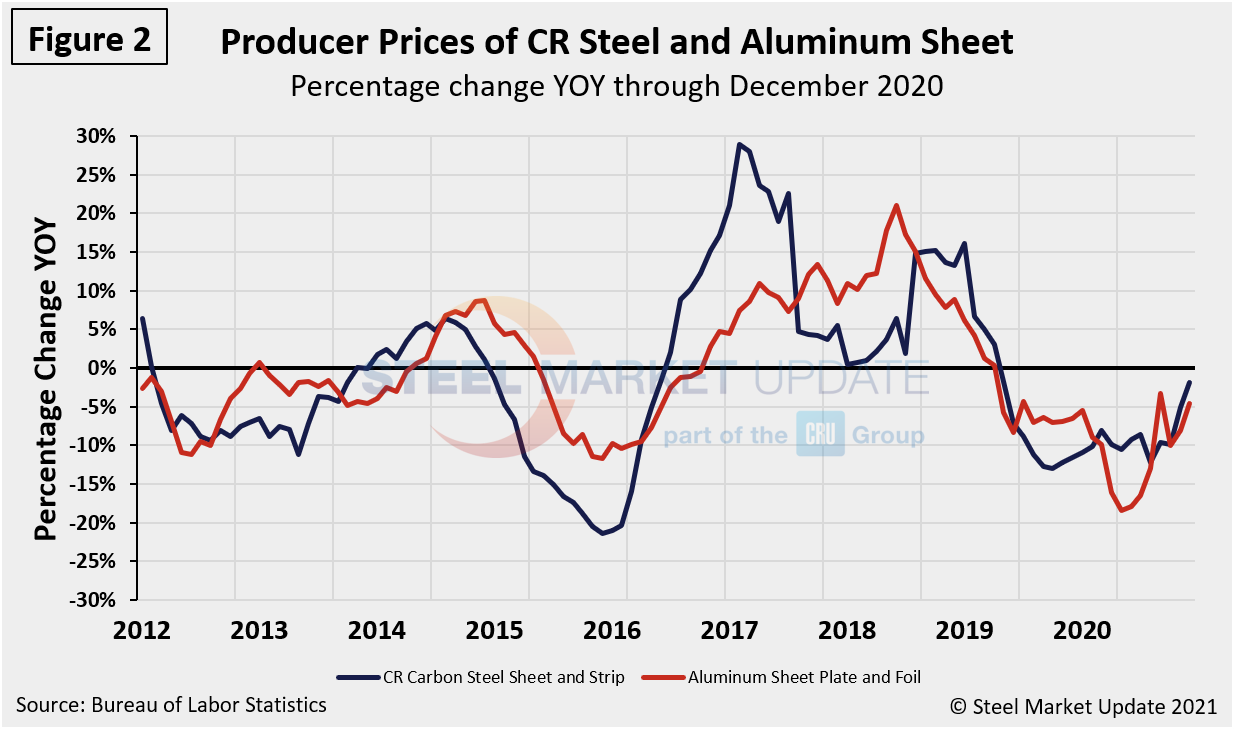

Figure 2 shows the year-over-year comparison of the price change of cold rolled steel sheet and flat rolled aluminum. The lines crossed in August 2018 when steel prices began to escalate faster than aluminum. This relationship reversed in July 2019 and for six months the price of cold rolled declined faster than that of aluminum sheet. Significant variations have been seen throughout 2020, however, as cold rolled steel sheet has recovered at a faster pace than flat rolled aluminum through December. Cold rolled steel was at negative 1.8 percent versus a negative 4.6 percent for aluminum. Although, both price indices remain in a negative state, they have both been improving month on month.

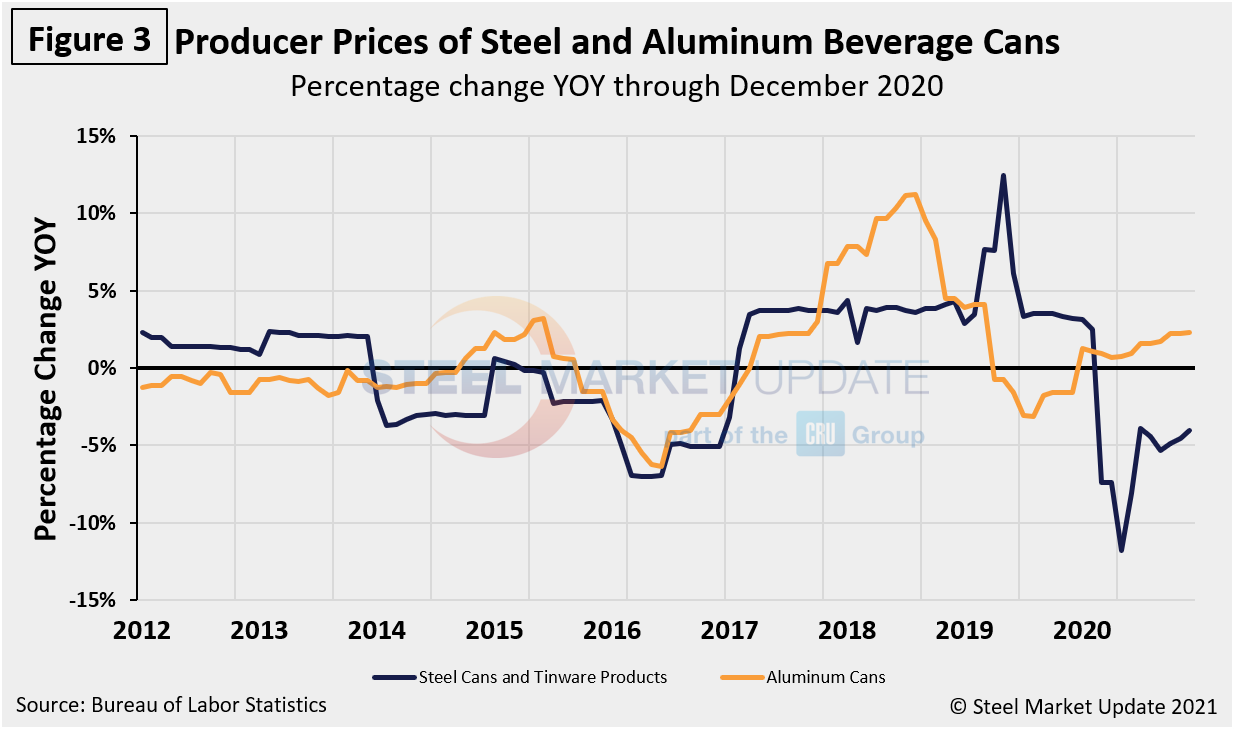

Figure 3 shows the same comparison for steel tinware products and aluminum cans. Since 2016 there has been no relationship between the price change of either type of can with their raw materials prices. This year has brought about vastly varying changes as aluminum cans have recovered to a positive 2.3 percent through December 2020, while steel tinware products plummeted through April to a negative 11.8 percent, but have since fluctuated, finally rising to a negative 4.0 percent to close out the year.

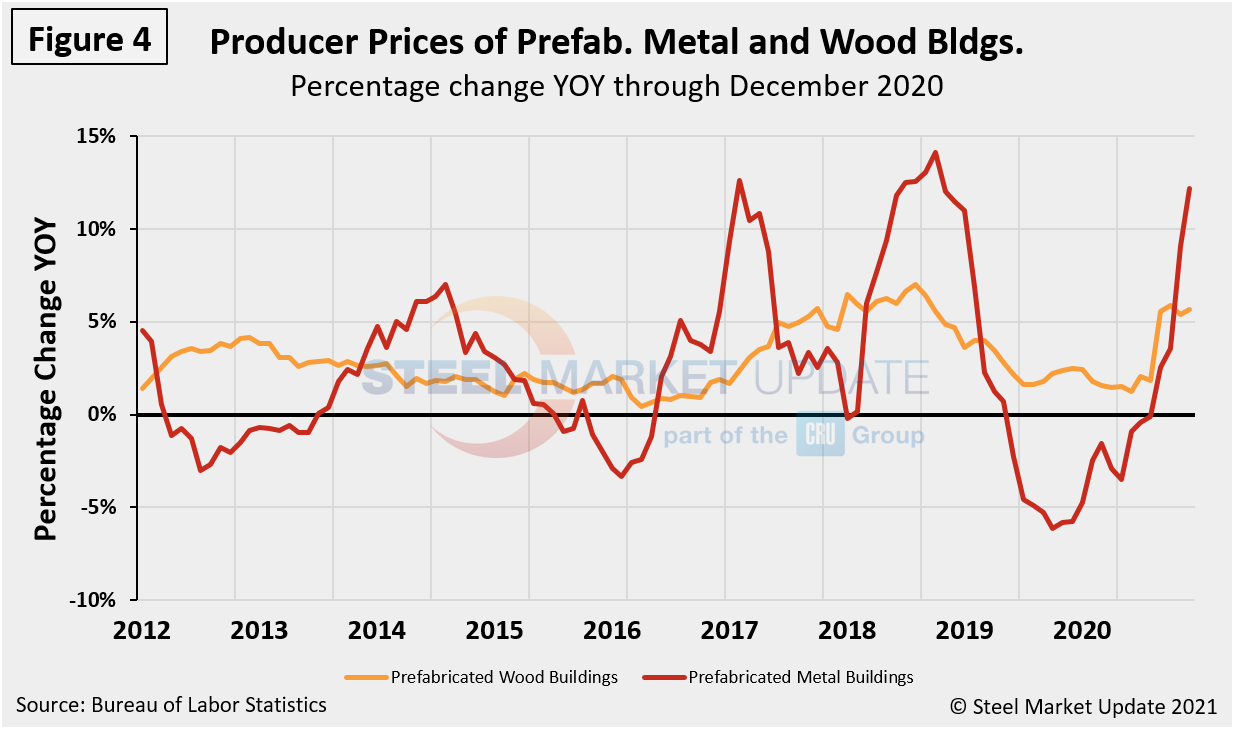

Figure 4 compares prefabricated metal buildings with prefabricated wood buildings. In this analysis, steel lost ground from a competitive point of view in 2018 and made it up in 2019. Similar to Figure 3, prefabricated steel buildings fell to a negative 3.1 percent in June, but have since rallied to a positive 12.2 percent through December, outpacing prefabricated wood buildings, which now stand at a positive 5.6 percent. The price of steel buildings has escalated by nearly 10.0 percent since September, while the price of wood buildings has varied inconsistently during the same period.

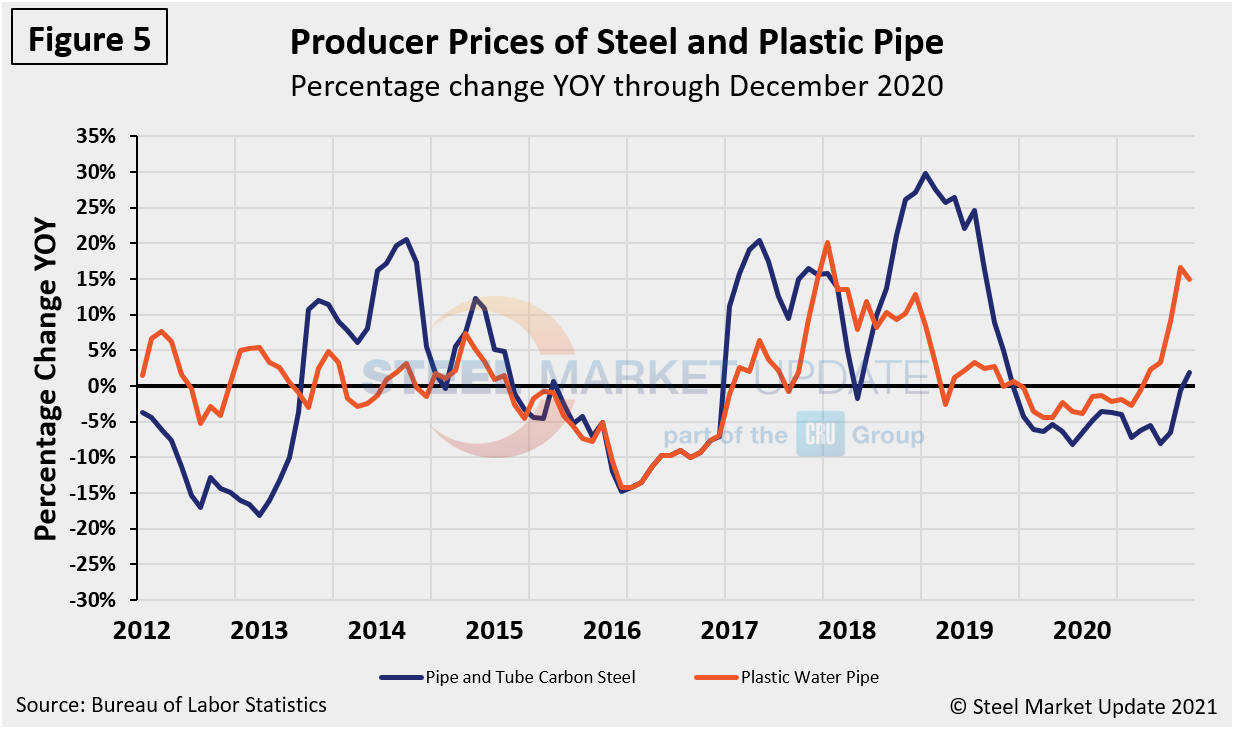

Figure 5 compares the price changes of steel and plastic pipe, which moved in opposite directions to the detriment of steel in 2018. In 2019, the rates of price escalation came back in line by July where they stayed through February 2020. The global pandemic had a greater impact on steel pipe, dropping to a negative 8.0 percent through September, but rallied to a positive 1.9 percent in December. By comparison, plastic pipe had rallied by more than 14.0 percent since September, reaching a positive 16.5 percent in November, but slipped to a positive 14.9 percent in December.

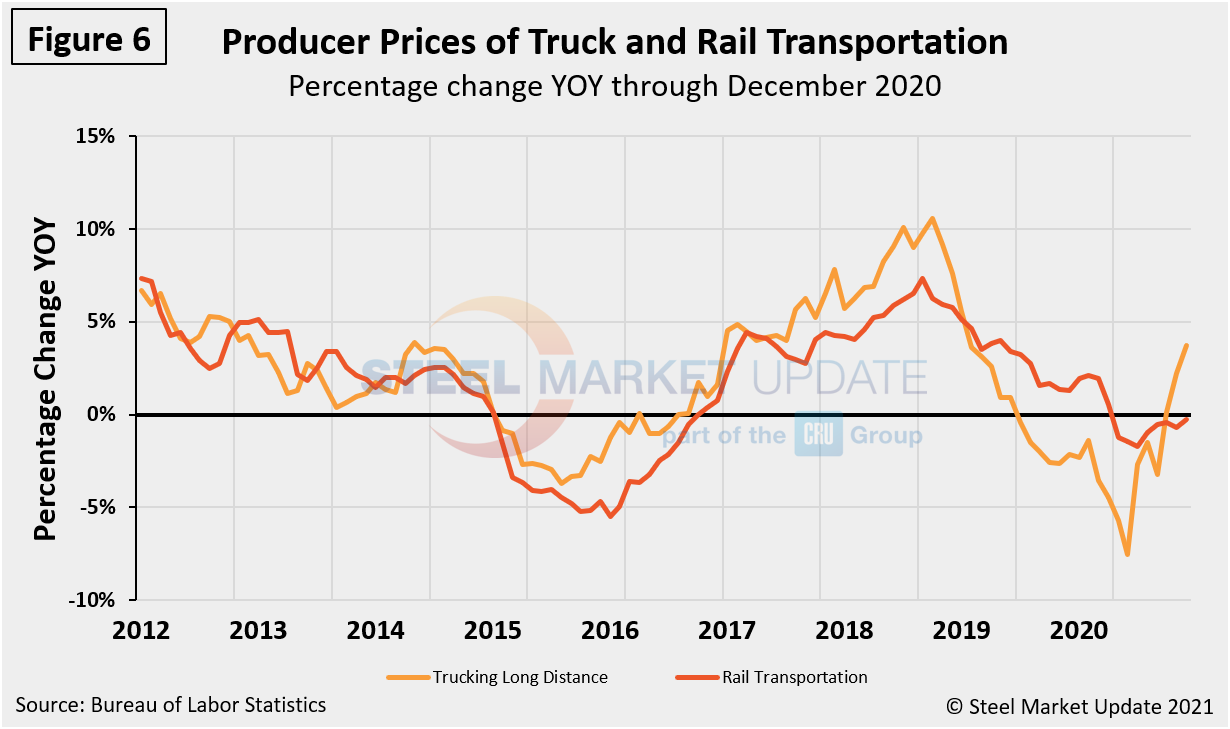

Figure 6 compares the changes in the price of truck and rail transportation. The escalation of truck transportation prices exceeded those of rail almost every month from January 2015 through April 2019 when the lines crossed. Trucking saw negative price escalation since August last year as rail prices continued to increase. Both experienced additional decreases through Q3 2020; however, trucking rallied to a positive 3.7 percent in December while rail fell to a negative 0.3 percent during the same period.

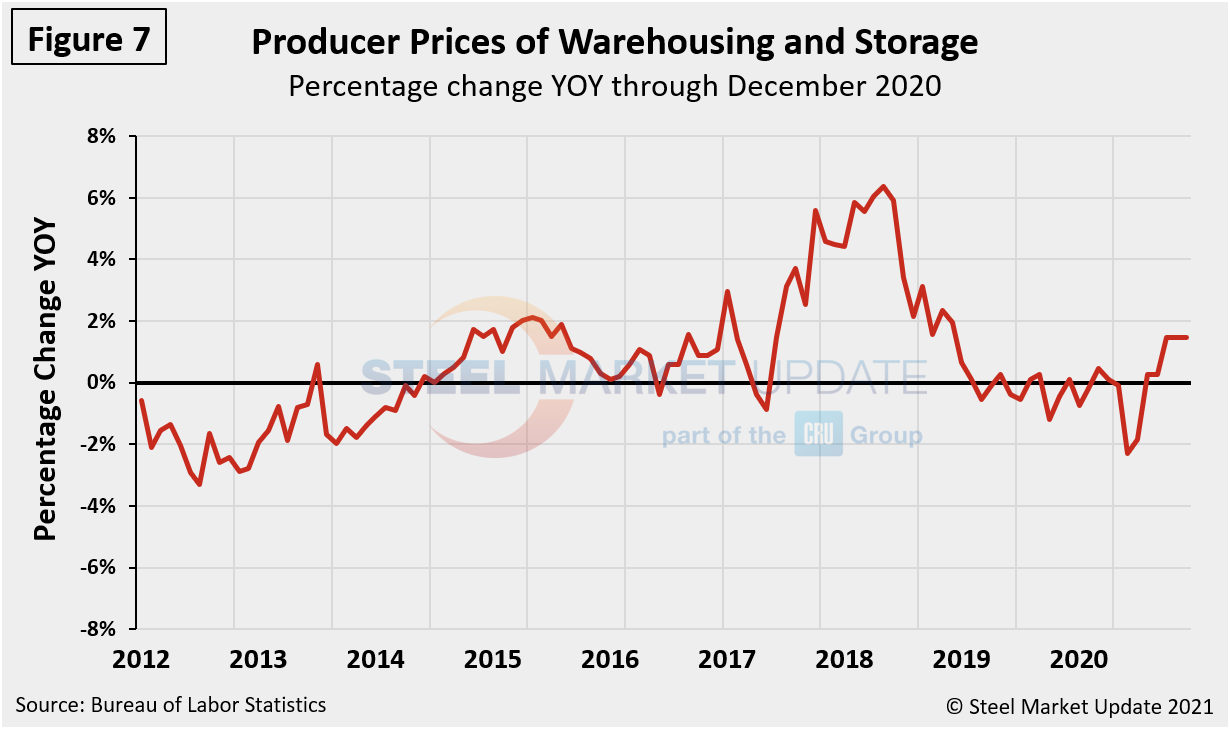

Figure 7 shows that the rate of change of the price of warehousing and storage declined steadily from April 2018 through March 2019. Despite largely holding stable throughout 2019, warehousing and storage were noticeably impacted by the global pandemic, falling to a negative 2.3 percent through June. They have since steadily rebounded to a positive 1.5 percent in October and have held there through the fourth quarter.

SMU Comment: The trend seen across all indices continues to point to an overall rebounding market that–despite notable near- and mid-term uncertainty–is pushing forward. The evidence doesn’t just lie within the sectors highlighted above but is certainly supported by rising demand across the steel market, soaring record steel prices, extended lead times, and rising raw steel production to name a few. Although a peak is expected in the next few months, there is still some room to grow in the meantime, and the January PPIs should further confirm this speculation.

The official description of this program from the BLS reads as follows: “The Producer Price Index (PPI) is a family of indexes that measure the average change over time in the prices received by domestic producers of goods and services. PPIs measure price change from the perspective of the seller. This contrasts with other measures, such as the Consumer Price Index (CPI). CPIs measure price change from the purchaser’s perspective. Sellers’ and purchasers’ prices can differ due to government subsidies, sales and excise taxes, and distribution costs. More than 10,000 PPIs for individual products and groups of products are released each month. PPIs are available for the products of virtually every industry in the mining and manufacturing sectors of the U.S. economy. New PPIs are gradually being introduced for the products of industries in the construction, trade, finance, and services sectors of the economy. More than 100,000 price quotations per month are organized into three sets of PPIs: (1) stage-of-processing indexes, (2) commodity indexes, and (3) indexes for the net output of industries and their products. The stage-of-processing structure organizes products by class of buyer and degree of fabrication. The commodity structure organizes products by similarity of end use or material composition. The entire output of various industries is sampled to derive price indexes for the net output of industries and their products.

By David Schollaert david@steelmarketupdate.com