Market Data

February 2, 2021

ISM: Manufacturing Continues its Recovery in January

Written by Sandy Williams

The manufacturing sector continued to expand in January posting a PMI of 58.7 in the latest Manufacturing ISM Report on Business. The PMI slipped slightly from December’s reading of 60.5, but indicated an eighth month of expansion for the overall economy, said the Institute for Supply Management.

“The manufacturing economy continued its recovery in January. Survey committee members reported that their companies and suppliers continue to operate in reconfigured factories, but absenteeism, short-term shutdowns to sanitize facilities and difficulties in returning and hiring workers are continuing to cause strains that limit manufacturing growth potential. However, panel sentiment remains optimistic (three positive comments for every cautious comment), similar to December levels,” said Timothy Fiore, chair of the ISM Manufacturing Business Survey Committee.

The indexes for new orders and production posted strong results of 61.1 percent and 60.7 percent, respectively, although easing from December results. The employment index gained 0.9 points to register 52.6 supported by order rates, longer backlogs and low customer inventories.

The backlogs index posted at 59.7, a 0.6 percent increase from December and expanding for a seventh month.

Raw material inventories, at an index reading of 50.8, continued to struggle with supply chain disruptions. “Inventory growth stability in light of ongoing supplier constraints indicates that supply chains are meeting near-term production demand, despite transportation and COVID-19 headwinds. However, delivery rates are not strong enough to grow inventory, as many panelists would prefer,” said Fiore. Customer inventories were deemed too low for the 54th month.

Prices for raw materials rose for an eighth consecutive month, reaching an index reading of 82.1 percent and the highest reading since 82.6 in April 2011.

Export orders grew at a slower rate in January, while the imports index rose 2.2 points to 56.8. Fiore pointed to higher factory demand and interest in increasing on-shore inventory. “Panelists continued to note record-breaking backlogs in ports of entry, as well as difficulty in arranging drayage and operating within the domestic transportation market,” he added.

Survey comments include:

- “Business is improving, but we are still struggling with a shortage of available labor.” (Primary Metals)

- “Our current business demand is going way past pre-COVID-19 [levels].” (Fabricated Metal Products)

- “Business is very good. Customer inventories are low, with a significant order backlog through April. Supply base is struggling to keep up with demand, disrupting our production here and there. Raw material lead times have been extended. COVID-19 continues to cause challenges throughout the supply chain. Huge logistics challenges, especially in getting product through ports and in getting containers. We are seeing significant cost increases in logistics and raw materials.” (Machinery)

- “2020 growth at 5% during a very challenging and volatile year. 2021 is expected to bring growth at a 7% or even greater pace. Logistics is the critical concern, but we are currently abating risk.” (Electrical Equipment, Appliances & Components)

- “Very strong demand with limitations in supply to meet increased demand.” (Transportation Equipment)

- “Supplier factory capacity is well utilized. Increased demand, labor constraints and upstream supply delays are pushing lead times. This is more prevalent with international than U.S.-based suppliers.” (Computer & Electronic Products)

- “We have had an increase in employees testing positive for COVID-19, negatively impacting manufacturing.” (Miscellaneous Manufacturing)

- “Business remains strong. Manufacturing running at full capacity.” (Chemical Products)

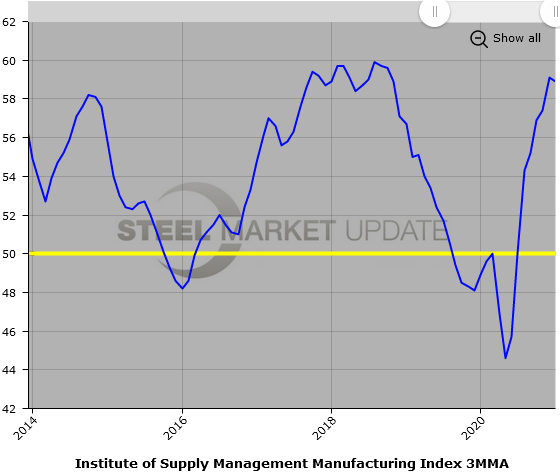

Below is a graph showing the history of the ISM Manufacturing Index as a 3MMA. You will need to view the graph on our website to use its interactive features; you can do so by clicking here. If you need assistance logging into or navigating the website, please contact us at info@SteelMarketUpdate.com.