CRU

June 13, 2021

CRU: Global Sheet Prices Have Now Fallen in Most Regions

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Sheet Products Monitor

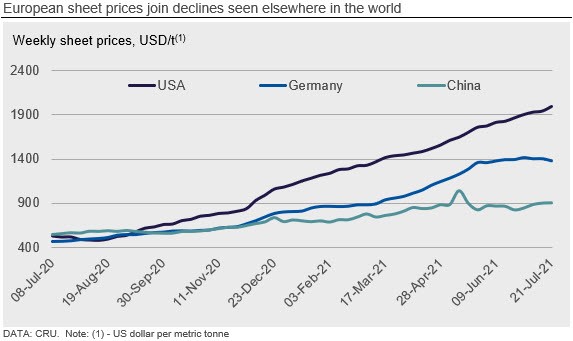

Sheet prices in northern Europe, like in other areas of the world, have begun to decline – although prices in the USA have yet to follow this trend. Still, it appears that this upward trend in the U.S. market is nearing an end. Although domestic prices in Europe have fallen slightly this week, they are still relatively expensive compared to imports even when factoring in applicable duties, and domestic prices in the USA are also well above those internationally. In China and Southeast Asia, prices rose w/w amid speculation that the Chinese government will introduce production restrictions, although seasonally weak demand in India has weighed on pricing there.

![]()

USA

In the USA, HR coil prices rose by $47 /s.ton w/w despite the fact that inventories are slowly rising. Buying patterns in general have also become less frenzied and more strategic. Buyers are optimizing contract tons and choosing to only purchase spot material that has been requested by a customer and can be moved quickly. While many companies are importing larger quantities than in the past, there are still some unwilling to because of concerns that the purchased price may not be advantageous when the material arrives or because the required minimum purchase tons are too large. Automotive production was expected to begin increasing during this portion of the year, but supply shortages have extended production delays into August.

Sheet prices on the U.S. West coast continued to increase this week as mills began accepting orders for October delivery. HR coil prices rose to $1,910 /s.ton, an increase of $60 /s.ton m/m. Order books remained tightly controlled, with customers receiving less tonnage than they preferred. Buyers’ hopes that the start-up of Ternium’s new mill in Mexico would offer relief have been tempered by an inability to obtain quotes for light-gauged HR coil or temper-passed material and warnings that deliveries may be delayed.

Europe

Upward momentum for European sheet prices slowed this week as more uncertainty emerges in the market. German HR coil has fallen by €5 /t to €1,180 /t w/w, narrowing the differential seen with Italian HDG coil to €30 /t. German HDG coil and Italian CR coil have also slipped somewhat following recent falls in China. European sheet prices overall appear to be expensive even when factoring in import duties.

Steel service centers are heard to only be buying material that they can sell because of financial issues, while end-use buyers and processors in northern Europe now demand more material. Rumors emerged this week of a potential anti-dumping investigation into arrivals from India after large volumes have been imported into Europe over the last few months. This follows the news that approximately 300,000 tonnes of HR coil are allegedly already awaiting custom clearance after the new July-September quotas opened on July 1.

Market feedback reports that real consumption of steel is strong in the Italian market, supporting price increases seen in southern Europe. Material for import from Asia has been offered to Italy for September shipment, but in limited quantities. Meanwhile, India, which has exhausted its HR coil quota for Europe, was heard to have sold large volumes of HR coil to Turkey instead at around $100 /t below Turkish domestic prices. This material has the potential to be rerolled into CR coil or HDG coil and sold into Europe. Current import volumes into Europe are unlikely to be substantial enough to change the direction of price levels today when balanced against demand. Lead times in southern Europe are around a month shorter than in the north.

China

Chinese domestic sheet prices rose significantly this week on speculation surrounding government-led production cuts later this year. Currently, local government meetings in Anhui and Gansu regarding production controls in H2 have lifted market sentiment as some participants believe that tightening supply in these provinces, and possibly in other provinces, will push prices higher. Moreover, increasing mill maintenance activity given falling mill profitability will also lead to tighter supply conditions. Compulsory operation restrictions around Beijing-Hebei-Tianjin to reduce pollution and the risk of accidents prior to the Chinese Communist Party’s 100-year celebration had led to a dramatic drop in BF utilization rates in Tangshan. However, operations quickly resumed this week. Even so, end-use demand has been slow seasonally. Sheet inventories continued to rise at a weekly rate of 2%, demonstrating this weakness in underlying demand. In addition, there are increasing financial burdens for participants who hold inventory, and they have reduced purchase volumes as a result. We expect sheet prices to stay volatile in the coming weeks with the market seeking clearer policy direction.

Asia

Prices of imported sheet products edged up this week because sellers raised offers despite quiet demand. CRU assessed HR coil prices at $930 /t CFR Far East Asia, a $20 /t rise w/w. CR coil prices were assessed at $1,100 /t CFR Far East Asia (flat w/w), while HDG prices were assessed at $1,120 /t CFR Far East Asia, also flat w/w.

For HR coil SAE1006 grade, Indian material was offered at $935-945 /t CFR Vietnam, while the highest bid in the market was at $930 /t CFR Vietnam. Offers of Chinese material were very limited, and most mills were not willing to sell lower than $1,000 /t CFR Vietnam.

The Formosa Ha Tinh steel mill also announced its offer for September shipment this week, and HR coil was offered at price equivalent to $970-975/t CFR Vietnam to their domestic customers. This new offer is a $60/t decrease from the previous month.

India

In India, the onset of the rainy season across major states has impacted sheet demand. Offtakes are low due to weak buying intent from key end users in the automotive and ancillary, construction, industrial packaging, and general engineering sectors. Meanwhile, in the spot market, trade inventory is growing due to low activity and retailers/distributors are deferring restocking from mills. It is because of this weak offtake (both from end users and traders) that steelmakers have started offering quantity-based discounts to local buyers, while also reducing their export offer prices to attract buyers in SE Asia.

CRU understands that in the last week, Indian mills have booked HR coil for export to Vietnam at $915-925 /t CFR (down by $25-30 /t w/w), while offers to Turkish and UAE-based buyers are at $945-950 /t CFR and $960-970 /t CFR respectively. These lower-priced export deals have caused a further drop in domestic sheet prices, which are down by INR500-800 ($7-11) /t w/w. In the near term, Indian sheet prices may find some support from a maintenance shutdown underway at JSW Steel’s 12 Mt /y Vijayanagar Steel Plant and a possible export pull back from Russian and Chinese suppliers due to export tax policy-related developments.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com