Market Data

August 12, 2021

SMU Market Trends: Change in the Wind for Steel?

Written by Tim Triplett

Do you have a sense that conditions in the steel market are changing? If so, you are not alone.

The majority of steel buyers polled by SMU over the last two weeks feel it won’t be until the fourth quarter, if not well into next year, before there will be any significant changes in steel demand and pricing. But a growing number report some subtle signs today that change is in the wind.

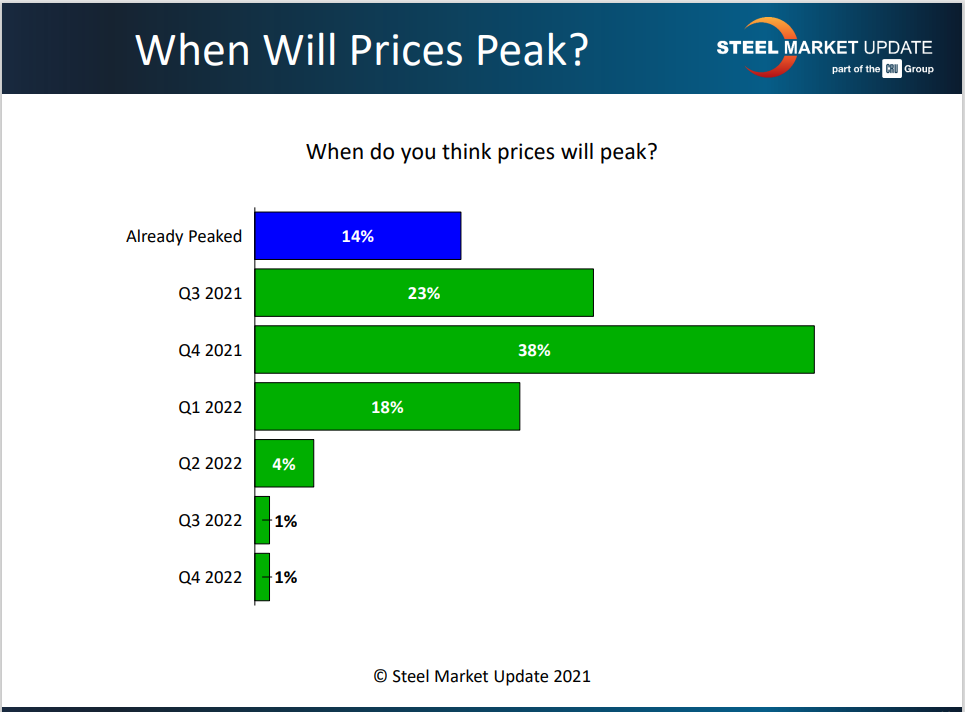

The benchmark price for hot rolled steel hit an astounding high of $1,900 per ton this week on the one-year anniversary of the price rally that began in August 2020. Begging the question: When will prices peak?

Spot prices continue to rise, report virtually all the service center and manufacturing executives responding to SMU’s recent questionnaires, though the pace and the size of each increase seems to be smaller. “We are seeing signs pointing towards slower increases, but we aren’t seeing anything signaling a reversal. This runup still has legs, and we will get to $2,000/ton HR in the indices,” predicted one service center exec.

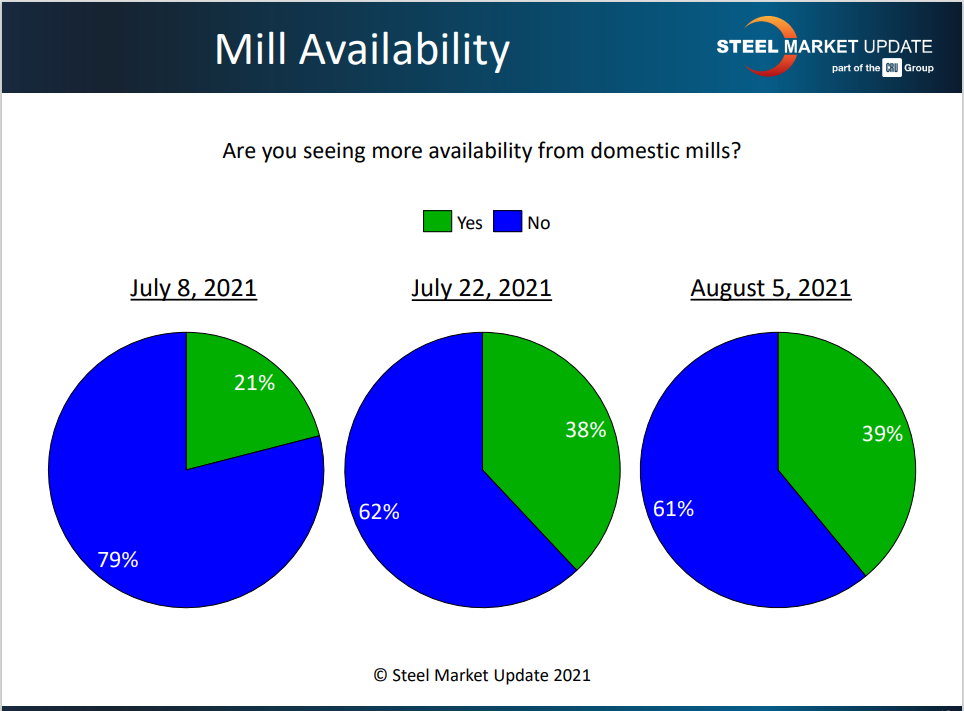

A significant number do confirm they have seen some loosening in the availability of spot tons on the market and some have been able to max out their contract levels. “It depends on the mill. In general, automotive-centric mills have some limited availability. EAFs and conversion mills have little or no spot,” said one respondent.

Certainly not every buyer is reporting an improvement in supplies. “There’s no new availability whatsoever. We get told not to ask anymore,” said one disgruntled source. “We’ve heard rumors and read the headlines, but we haven’t seen any extra tons being floated around,” added another. “We remain in one of three lanes, depending on the mill: (1) on strict allocation, (2) not getting offered anything, or (3) not getting the full ask off contracts (ie. being kept to the minimums).”

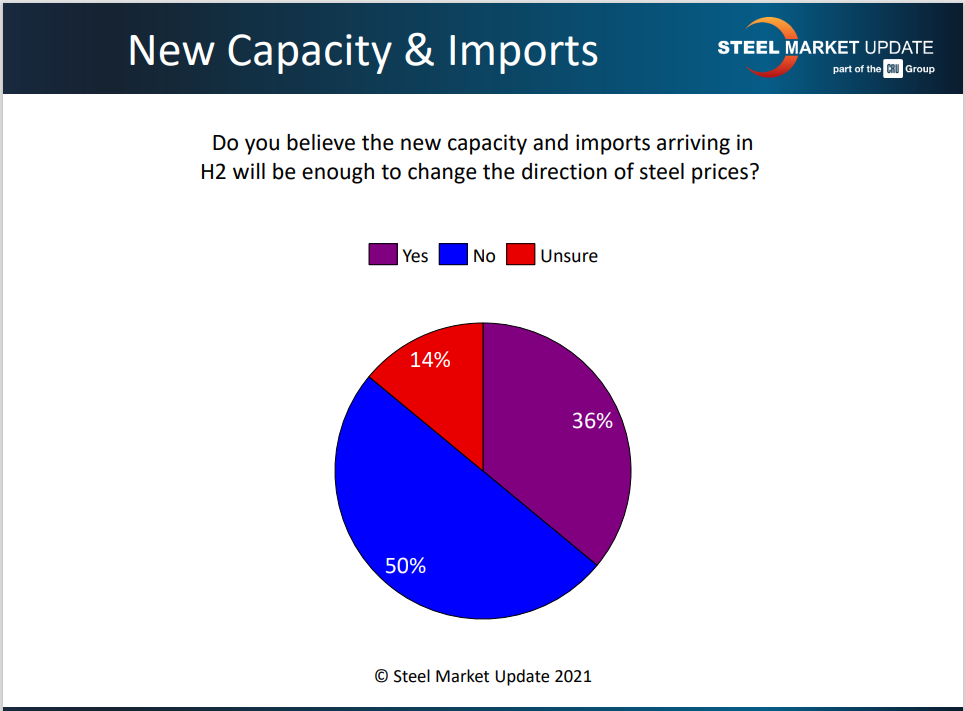

Buyers appear split on the question of whether the new capacity and imports that are coming will be enough to change the direction of steel prices this year. Many predict it will be the first or second quarter next year before supply begins to catch up with demand. “I think the market could certainly plateau or ease, but I don’t sense any sort of major correction this year,” said one. “More import is coming, but not enough to put a dent in inventories,” said another.

There’s no chance that capacity expansions and foreign steel on route to the U.S. will have any effect on steel prices this year, asserted one adamant individual. “The experts/pundits/analysts whiffed on that theory. I have no issue with the fact that their initial thesis got thrown a curveball thanks to COVID – that is not their fault – but their blind insistence and double down on it was reckless. I mean $600/ton by the end of the year? Yeah, right! And that is what they said back in mid-June! The overcapacity is coming, but it’ll be a 2H 2022 phenomenon, definitely not this year.”

Others hope the mills will “be responsible” and “take the pricing down slowly.” Automotive demand may prove decisive. “If problems persist in the auto sector, then [a downturn in prices] is very possible. This auto supply chain disruption story continues to get worse (chips and COVID restrictions overseas). Frankly, there’s a growing possibility that unless it improves quickly, it could cause things to unravel here sooner than people think.”

Do You Sense a Change in the Air?

Everyone is on heightened alert for signs of changing market conditions that may be a precursor to the inevitable price correction to come. Indeed, several respondents to SMU’s survey this week reported small changes that may hint that the downturn is approaching:

“For the first time in many months, we are able to secure more tons than needed. Steel prices outside of the U.S. are mostly heading lower. And the Delta variant is becoming a bigger concern.”

“I am seeing more tons available from every mill, not large tons but each month there seems to be 15-20% more available.”

“Customers are now starting to balk at prices, whereas they had been willing to pay any price as long as you could provide the steel.”

“The mills are more current, and inventories are generally higher vs. record low levels. The other issue is the widening gap between U.S. sheet prices vs. everywhere else. Asia and the EU appear to have peaked and are seeing some slight corrections/stability, while the U.S. continues to climb. It feels like the U.S. is getting close to peaking soon, but we’re not expecting any dramatic drop when it does.”

“Based on increases in foreign offerings it appears the global steel market is seeing small reductions in demand/price.”

“One of our vendors is floating ‘more favorably priced’ import HR, but for December-January delivery. This could start to weigh on prices over the next couple of months.”

“Not sure how long this march upwards is going to last if automotive doesn’t start picking up, but I think the mills are banking on upcoming outages to offer stability. With capacity utilization high, mills catching up, input costs relatively stable and more spot opportunities, I believe we will soon see if there’s true demand out there or if companies are over-forecasting just so they can stay in supply.”

“I still believe there are a lot of duplicate tons placed for insurance. This will surface as soon as prices falter – and falter they will. Between steel prices, credit demand and cost of goods, this has to end.”

“I think we are just dollars away from the top, but we will stay at the top for a while before we see a softening.”

A gradual softening of steel prices may be wishful thinking. Some analysts expect a sharp correction at some point. When and how much is anyone’s guess. As one buyer commented: “Reading the proverbial tea leaves has me thinking I need to read other types of leaves, because these aren’t working.”

By Tim Triplett, Tim@SteelMarketUpdate.com