CRU

October 13, 2021

CRU: U.S. HR Coil Prices Start to Fall

Written by Josh Spoores

By CRU Principal Analyst Josh Spoores, from CRU’s Steel Sheet Products Monitor

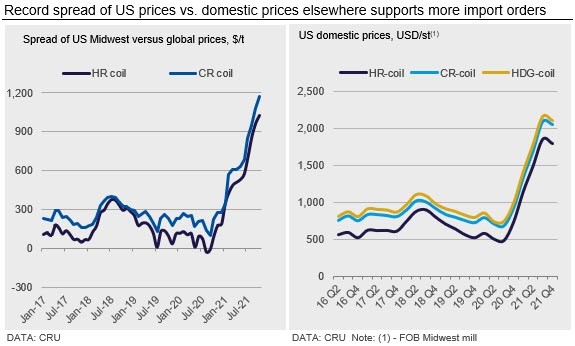

North American sheet prices are lower m/m as prices in the U.S. have finally started to fall, at least for HR coil. Over the past several weeks, the amount and overall volume of spot transactions between mills and buyers have slowed, yet we have recorded a wider spread of prices. We continue to see HR coil being transacted near $1,960 /s.ton, but we also have had numerous transactions below $1,900 /s.ton.

While HR coil prices are now 2.2% below the high recorded in late September, prices of CR and HDG coil have been slower to follow this trend. Yet prices for these value-added products have stabilized as new domestic supply has come online, but maybe more so due to the wide spread of U.S. sheet prices versus global prices. Buyers of CR and HDG coil products continue to book imports that, net of all logistical and tariff costs, are near $600 /s.ton cheaper than domestic offers.

Due to these massive price spreads as well as domestic mills keeping supply tight, some buyers have fully embraced imports to not only maintain supply, but also as a way to minimize their cost exposure to U.S. domestic sheet prices. This strategy has now extended to more than just a one-time purchase as some buyers have opted to supplement, or in some instances replace, annual domestic contracts with imports.

Prices on the U.S. West Coast were unchanged this week after December order books filled quickly. There was a slight pricing decline of less than 1% for December production versus November production on all sheet products. This decrease came about alongside the weaker prices emerging in the Midwest market. Despite availability increasing in the rest of the country, buyers on the West Coast have not seen an increase in offers from domestic mills outside of the region. Logistical issues continue to create a delay in delivery, despite material being produced on time from mill sources. Buyers have begun to see an increase in their inventory levels and are becoming more selective on the material they purchase.

In Mexico, sheet product prices fell for the second consecutive month. HR coil prices are around 3% lower m/m while CR coil fell by around 1% m/m. The reduction in prices was attributed to weaker domestic demand and ample supply, despite AHMSA’s two-week maintenance stoppage in its hot strip mill, which should be back to work this week. Like the rest of North America, sheet demand from the automotive sector in Mexico continues to be impacted by the shortage of auto parts. Ford announced a two-day full stoppage at its Hermosillo plant due to the shortage of material on Oct. 11-12, while Nissan also announced it will temporarily suspend production in various days in October due to the semiconductor shortage. According to Inegi, Mexican light vehicle production fell by 12% m/m and 33% y/y in September and has increased by only 6% YTD through September. Expectations for auto production and steel demand by the sector in 2021 Q4 are not positive, particularly following the recent production suspension announcements.

Outlook: Rapid Price Adjustment is Likely

Due to the record discount of imported sheet versus domestic prices, we expect that import arrivals will continue to come in at high rates. These arrivals are expected to remain high through most of 2022 Q1, a period of time when 5 Mt of new EAF-based production begins to ramp up. In addition, automotive production continues to be held back by supply constraints from electronic components, while seasonality will also limit some near-term demand, albeit at lower levels than in normal years.

While we expect sheet prices to quickly drop through 2021 Q4 to come back in line with global prices, further declines will then be fully dependent on raw material inputs. If key inputs such as iron ore, coking coal and energy costs remain at a higher level for longer, so too will finished sheet prices. However, excessive energy costs may quickly usher in slower industrial growth than we currently expect.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com