Market Data

October 15, 2021

WSA: Steel Demand Recovery Stronger than Expected in 2021

Written by David Schollaert

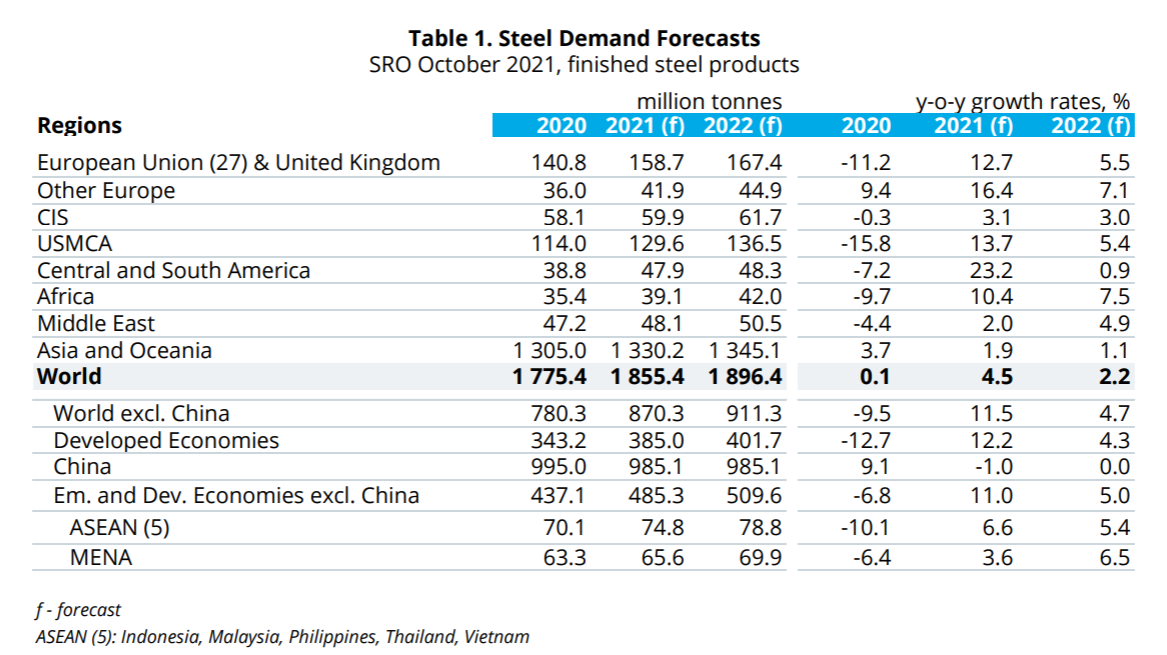

Global steel demand will grow by 4.5% in 2021 and reach 1.855 billion metric tons following a 0.1% growth the year prior, according to World Steel Association’s (worldsteel) October 2021 Short-Range Outlook (SRO).

An additional increase of 2.2% to 1.896 billion metric tons in 2022 is forecast for steel demand worldwide. The current forecast assumes that the universal progress of vaccinations will lead to a less damaging and disruptive global spread of COVID-19 variants than seen in previous waves, said worldsteel.

“2021 has seen a stronger than expected recovery in steel demand, leading to upward revisions in our forecast across the board except for China,” said Al Remeithi, chairman of the worldsteel Economics Committee. “Due to this vigorous recovery, global steel demand outside China is expected to return earlier than expected to its pre-pandemic level this year.”

Remithi said the main contributor to such growth is strong manufacturing activity bolstered by pent-up demand, notably in developed economies. According to worldsteel’s analysis, developed economies have outperformed previous expectations by a larger margin over developing economies. A direct reflection on the positive benefit of higher vaccination rates and government support measures. In the emerging economies – especially in Asia – the recovery momentum was interrupted by the resurgence of infections.

“While the manufacturing sector’s recovery remained more resilient to the new waves of infection than expected, supply-side constraints led to a levelling off of the recovery in the second half of the year and are preventing a stronger recovery in 2021,” said Remithi. “But with high backlog orders combined with a rebuilding of inventories and further progress in vaccinations in developing countries, we expect steel demand will continue to recover in 2022.”

Remithi cautions, however, that persistent rising inflation, coupled with ongoing slow vaccination progress in developing countries, and further growth deceleration in China, will all pose risks to worldsteel’s latest SRO.

China

The Chinese economy sustained its strong recovery momentum for much of 2020 into the early part of 2021. Since June it has slowed, however, with marked signs of deceleration in the steel-using sectors since July, leading to a steel demand contraction of -13.3% in July and -18.3% in August.

The sharp deceleration is partly attributable to occasional factors such as the recent adverse weather and small waves of infections through this summer. However, more substantive causes include the slowing momentum in the real estate sector and the government cap on steel production, said worldsteel.

Chinese steel demand will have negative growth for the rest of 2021 due to poor infrastructure development and weakening real estate activity. As a result, while the January to August apparent steel use still stands at a positive 2.7%, overall steel demand is expected to decline by -1.0% in 2021.

No growth in steel demand is expected in 2022, with the real estate sector remaining depressed in line with the government policy stance on rebalancing and environmental protection.

Developed Economies

Targeted and localized lockdowns helped curb the impact of the latest infection waves on economic activities in developed economies. Yet supply chain bottlenecks and labor disruptions are preventing a more robust recovery, worldsteel said.

Momentum could strengthen in 2022 driven by consumer confidence, should supply chain bottlenecks ease and pent-up demand continue. Worldsteel estimates that steel demand in developed economies will increase by 12.2% in 2021. With an additional 4.3% growth in 2022, steel demand will reach its pre-pandemic level, after falling by -12.7% in 2020.

In the U.S., the economy continues its robust recovery, driven by pent-up demand and a vigorous policy response. Steel demand was aided by the strong performance of the automotive and durable goods sectors, but shortages of some components are undermining this recovery. The momentum in the construction sector is weakening with the end of a residential construction boom and sluggish nonresidential sector activities. The recovery in oil prices is supporting a recovery in energy sector investment, however. There could be more upside potential should the Biden administration’s infrastructure stimulus program pass, but this would not feed through until late 2022.

In the EU, the recovery in steel demand that started in the second half of 2020 is gathering pace, with all steel-using sectors exhibiting a positive recovery despite continuing waves of infection. The automotive, manufacturing and construction sectors have been the primary drivers of growth in Europe. Supply chain bottlenecks, particularly in the automotive sector, are causing a loss of momentum. Construction and domestic appliances are expected to recover to a pre-COVID level in 2021.

In developed Asia, the COVID situation worsened in 2021, exacerbated by slower vaccination progress, but steel demand recovery was not interrupted, and the forecast has been revised up, helped by the strong rebound in global trade and government infrastructure programs.

In Japan and Korea, steel demand is recovering gradually, potentially matching pre-pandemic levels by the end of the year. Steel consuming sectors are expected to benefit from recoveries in manufacturing and automotive, driving investment and positive growing in 2022, worldsteel said.

Developing Economies

Aided by the recovery in commodity prices and international trade, steel demand in developing economies rebounded well in 2021. Waves of new COVID variants combined with low vaccination levels and limited international tourism restrained their overall growth, however. Although vaccination progress and conditions in developing economies are expected to improve in 2022, the pandemic will leave a lasting impact on these economies through weakened financial positions and accumulated structural challenges, worldsteel said.

India’s initial economic recovery from the first COVID wave was tested by the more severe second wave, but was much less severe due to concentrated lockdowns. Since July, a healthy recovery has resumed for all sectors, resulting in only a minor downward revision in worldsteel’s forecast of India’s steel sector. India will reclaim the 100 million metric tons mark in its steel sector this year.

Only a moderate recovery is expected for ASEAN countries. Vietnam had successfully escaped the serious economic impact in 2020, but due to a recent infection surge the 2021 outlook has been scaled down. Surprisingly, the Philippines has managed to implement construction projects despite COVID restrictions.

Steel demand in Latin America, except Brazil, was severely hit by the pandemic in 2020. But in 2021 a surprisingly strong recovery has been taking place due to the construction and automotive sectors rebuilding inventory. Markedly weakened momentum could be seen in 2022, however, due to high inflation, heightened fiscal deficits and political uncertainty.

After recording positive growth in 2020, Brazil’s steel demand continues to grow strongly in 2021, driven by government stimulus and strong construction activity, which stood above its pre-pandemic level in the first half of the year. High interest rates, fiscal weakness, and political tensions will drive the outlook for 2022 down. Mexico also saw a stronger than expected recovery driven by industrial activities, especially the automotive sector.

Despite a moderate fall in 2020, Russia’s steel demand recovery is supported by a strong rebound in the automotive sector. The construction sector is supported by the government mortgage subsidy program. Turkish steel demand will continue to show high double-digit growth in 2021, driven by infrastructure projects and industrial activity. Turkey’s steel demand will exceed the pre-currency crisis level of 36 million metric tons in 2022, worldsteel said.

Steel-using Sectors Likely to Drive Growth

In general, construction has remained more resilient to the pandemic shock than manufacturing. Construction activity was severely disrupted by total project stoppages in many developing economies, setting up a robust recovery fueled by low interest rates and government infrastructure spending, said worldsteel.

Low vaccination rates have curbed the sector’s recovery in some regions compared to others. In China, the construction sector is facing a turning point and the real estate sector is likely to enter a correction period as the government tries to tackle the sector’s structural problems.

The outlook for global infrastructure projects will vary as developed economies leverage infrastructure as a recovery tool, while developing economies will have reduced ability for financing infrastructure investment due to the pandemic’s impact. The residential sector has benefited from accumulated savings during the lockdown. The nonresidential sector, however, will see a sluggish recovery due to reduced demand for office space.

The automotive sector recovered strongly in the second half of 2020 after seeing the sharpest decline among steel-consuming sectors during initial lockdowns. Although supply-chain disruptions are still evident in some markets, the recovery is driven by pent-up demand and increased household savings.

In the U.S., light vehicle production regained its pre-pandemic level by the third quarter of last year, but it has been trending down since then, partly due to supply-chain disruptions. The EU automotive sector is expected to rebound by 15.3% in 2021 as a strong recovery is under way. Doubts remain, however, due to component shortages and a weak prospect of demand due to general economic uncertainty. In China, auto production soared in the first half of this year. Electric vehicle production led the way, surging by almost 200% from January to August, accounting for 11.2% of total vehicles produced over the period.

Supply-chain bottlenecks and shortages are significantly undermining the global automotive industry’s recovery. With demand dissipating, auto production growth will decelerate in 2022, though high order backlogs could provide support, worldsteel said.