Market Data

October 28, 2021

Consumer Confidence Improves in October

Written by David Schollaert

U.S. consumer confidence saw a surprise increase in October, after declining the three months prior, as concerns over the Delta virus improved, reported The Conference Board. The October index recovered by 4.0 points month on month after slipping 5.4 points in September.

“Consumer confidence improved in October, reversing a three-month downward trend as concerns about the spread of the Delta variant eased,” said Lynn Franco, senior director of economic indicators at The Conference Board. “While short-term inflation concerns rose to a 13-year high, the impact on confidence was muted. The proportion of consumers planning to purchase homes, automobiles, and major appliances all increased in October—a sign that consumer spending will continue to support economic growth through the final months of 2021. Likewise, nearly half of respondents (47.6%) said they intend to take a vacation within the next six months—the highest level since February 2020, a reflection of the ongoing resurgence in consumers’ willingness to travel and spend on in-person services.”

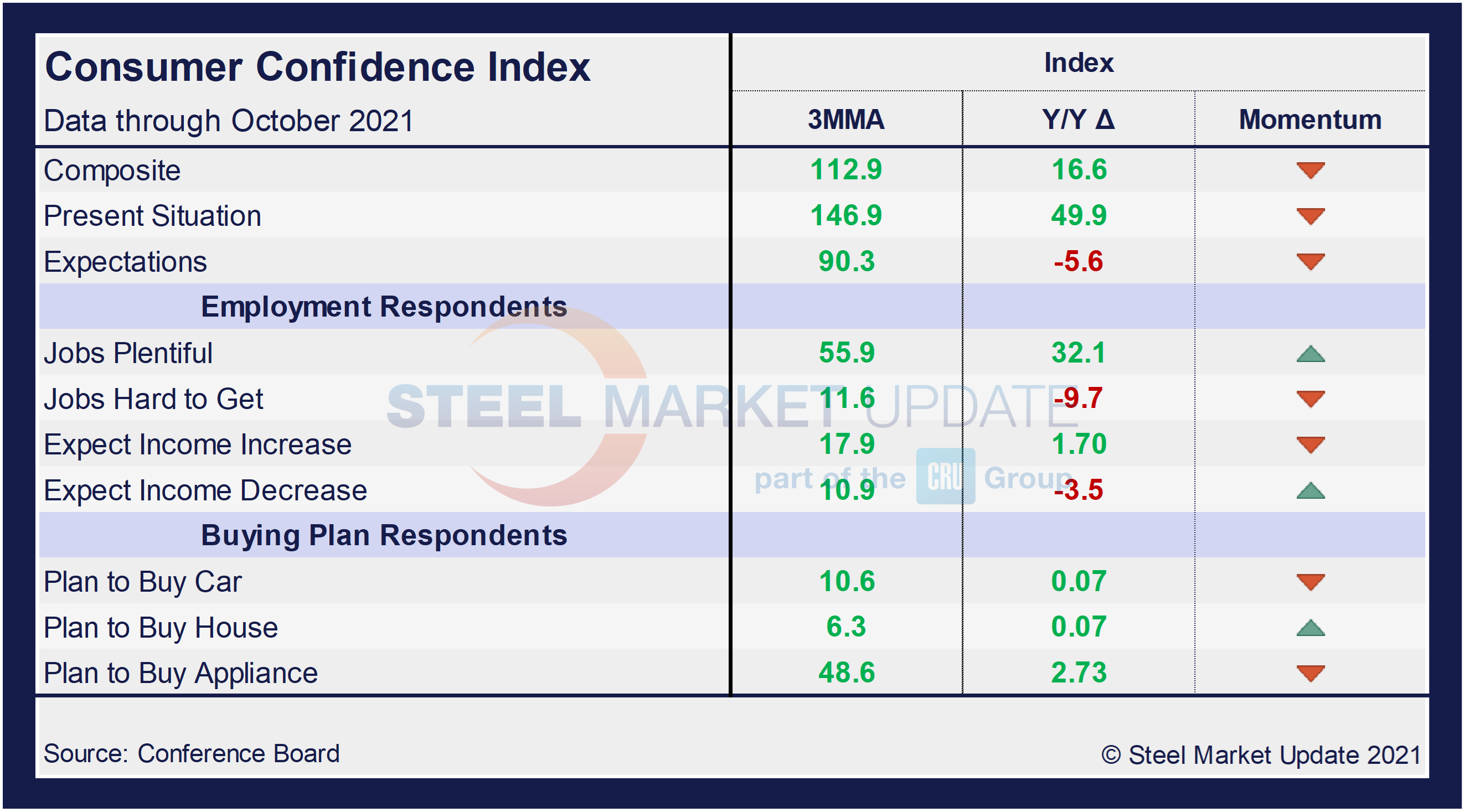

October’s present situation index, which is based on consumers’ assessment of current business and labor market conditions, saw a 3.1-point improvement month on month to a reading of 147.4, following a revised decrease of 4.6 points in September. The expectations index, which is based on consumers’ short-term outlook for income, business and the labor market, saw the strongest increase, growing by 4.6 points to 91.3, yet still the third-lowest mark all year.

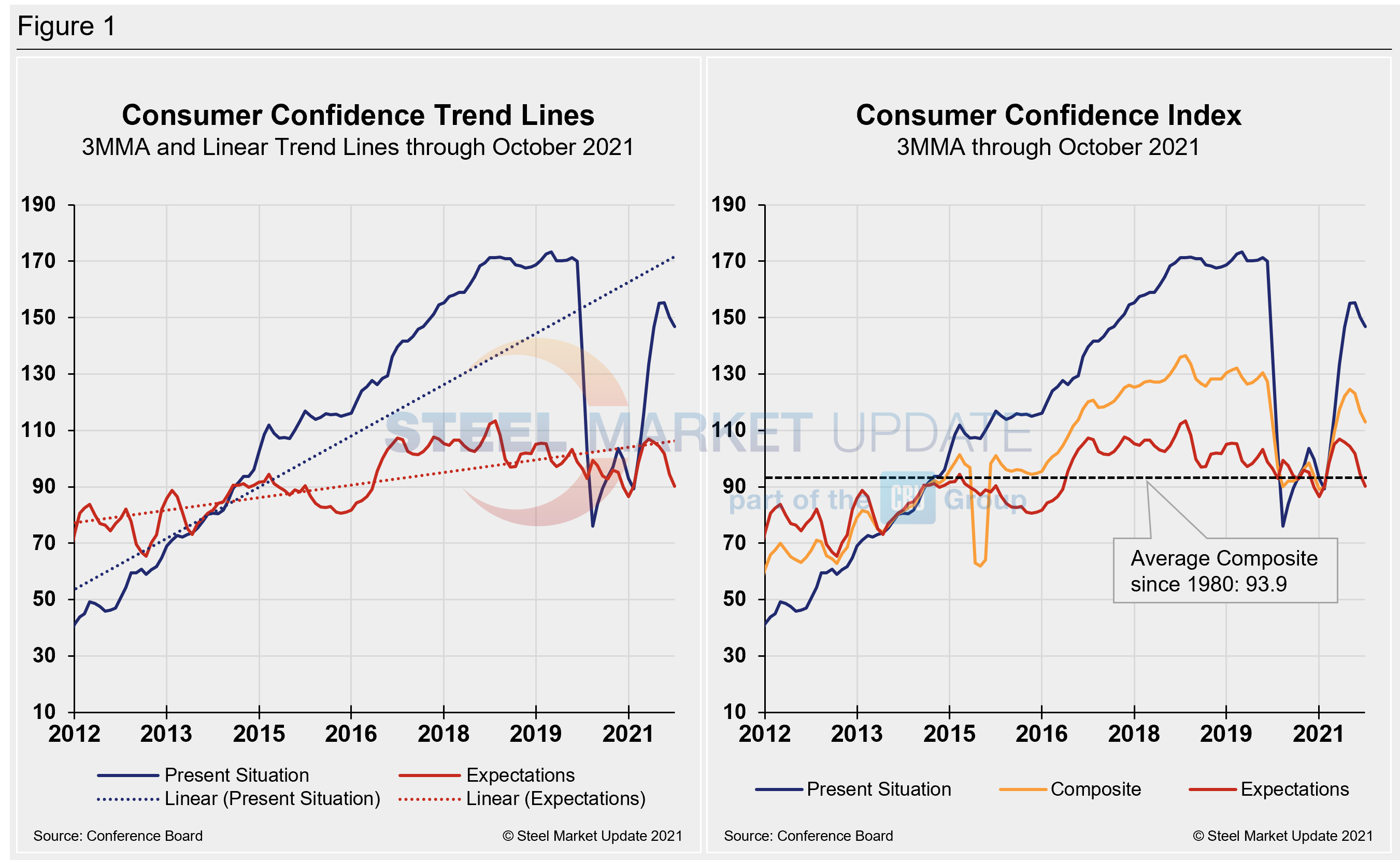

Calculated as a three-month moving average (3MMA) to smooth out the volatility, The Conference Board’s composite index slipped in October to 112.9 versus 116.5 in September – still well below the pre-pandemic high of 130.4 last February. Despite the negative turn, the index remains higher than the 96.3 seen a year ago. The composite index is made up of two sub-indexes: consumers’ view of the present situation and their expectations for the future. Figure 1 below notes the 3MMA linear trend lines from January 2012 through October 2021 versus the trend lines of all three subcomponents of the index: present situation, composite and future expectations. All three were above the average composite line in October 2020 before falling consecutively through February. The surge from March through June pulled all three indexes above the composite line once again, but all have started to erode, pulling expectations below the average composite line.

On a 3MMA basis comparing October 2021 with October 2020 in the table below, the present situation has an index reading of 146.9, a 3.3-point dip from the month prior but still 49.9 points above the year-ago reading. Expectations are at 90.3, down 4.2 from September, and just 5.6 points below year-ago levels. Even though two out of the three indexes show positive gains against year-ago measures from the fallout of the initial COVID-19 wave, the momentum indicator is still moving down despite the slight recovery in October. Consumers are less optimistic and hesitant when it comes to current market dynamics.

When comparing current 3MMA totals to the 2019 pre-pandemic year, the composite is still down 15.4 points, while the present situation is down 26.5 points. The expectations reading is down 9.0 points in October when compared to the same 2019 period. The consumer confidence report also includes both employment data and some purchase plans and these are likewise summarized in the table below. The color codes show improvement or deterioration of the individual components.

The composite, present situation and expectations indices had been trending up, recovering much of what was lost in the fallout from the global pandemic, but momentum has shifted downward over the past three months.

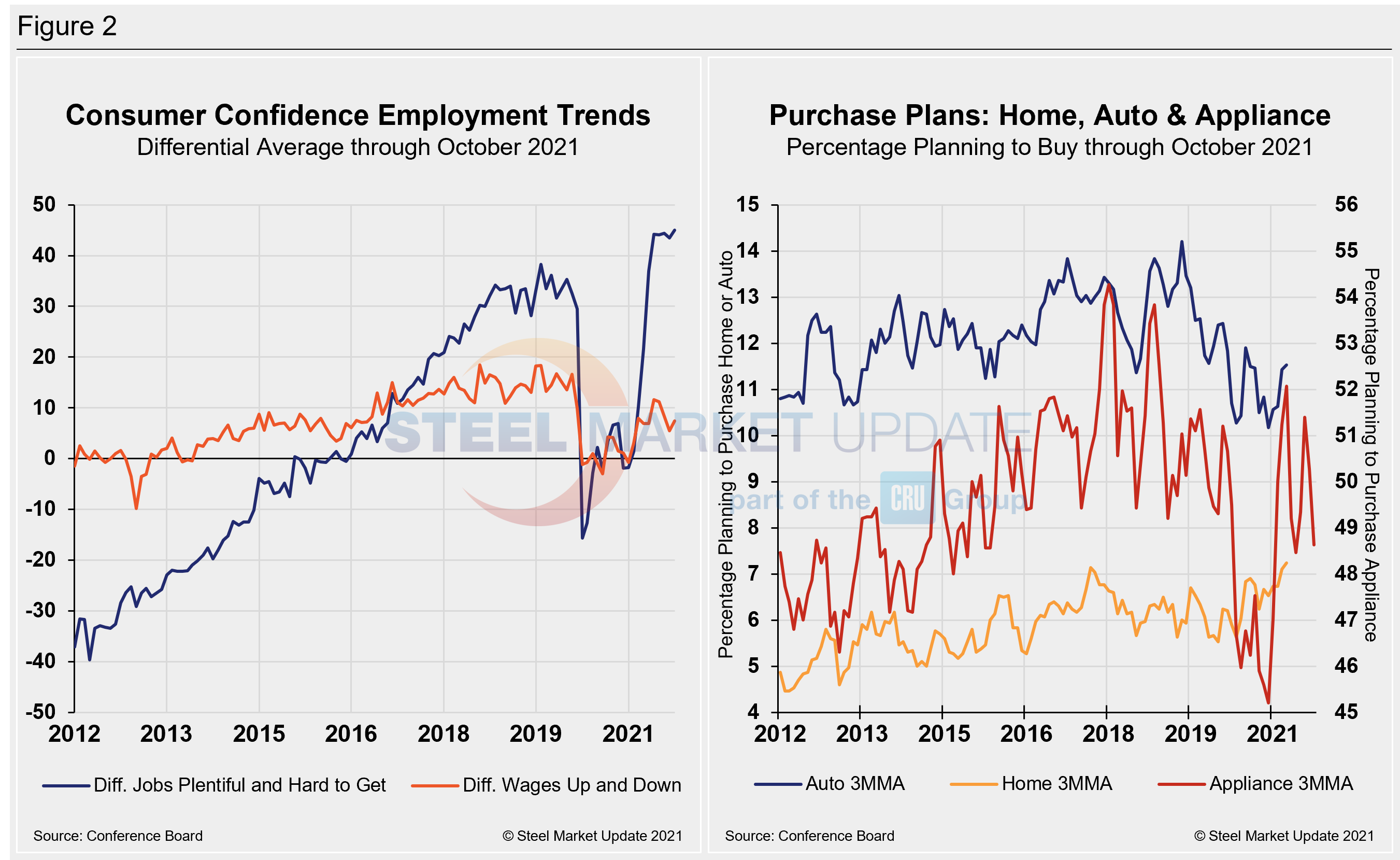

The unexpected increase in October came as concerns about high inflation were offset by improving labor market prospects, suggesting economic growth was picking up after a turbulent third quarter. Buying plans for autos, homes and appliances were uneven on a 3MMA basis and when compared to the same year-ago levels due to recent fluctuations. The only index showing some growth, was home buying, up 0.3 points month on month, and up 0.2 points year on year.

The labor market landscape has shifted of late. Job openings continue to rise, but optimism regarding the prospect of increased wages has dipped when compared to the same year-ago period.

People found jobs slightly less plentiful in October, but were a bit more optimistic about wage increases compared to the month prior. The differential between those finding jobs plentiful and those having difficulty was 45.0 in October, up marginally from 43.5 in September. The measure has easily eclipsed the most recent pre-pandemic high of 35.3 in January 2020, and is a strong rally from the -1.8 seen at the beginning of the year. The differential between those expecting wages to rise versus those expecting wages to fall is presently 7.4, up 1.9 points month on month and down from the recent high of 11.6 in June.

Spending plans for consumer goods as measured by automobiles, homes and appliances had been trending up through June, but started slowing in July. Since then, figures had moved down with consumer goods spending declining, but October brought about a slight recovery. Buying had contracted across all three categories successively in August and September, but all advanced in October. Automotive buying plans edged up 0.9 points to 10.7, home buying rose 2.0 points to 7.3, while appliance buying advanced 2.6 points to 49.0 in October. These recent dynamics and historical movements are illustrated below in Figure 2.

About The Conference Board: The Conference Board is a global, independent business membership and research association working in the public interest. The monthly Consumer Confidence Survey®, based on a probability-design random sample, is conducted for The Conference Board by Nielsen. The index is based on 1985 = 100. The composite value of consumer confidence combines the view of the present situation and of expectations for the next six months.

By David Schollaert, David@SteelMarketUpdate.com