CRU

November 11, 2021

CRU: Chinese Price Collapse Leads Global Sheet Market Lower

Written by Josh Spoores

By CRU Principal Analyst Josh Spoores, from CRU’s Steel Sheet Products Monitor, Nov. 10

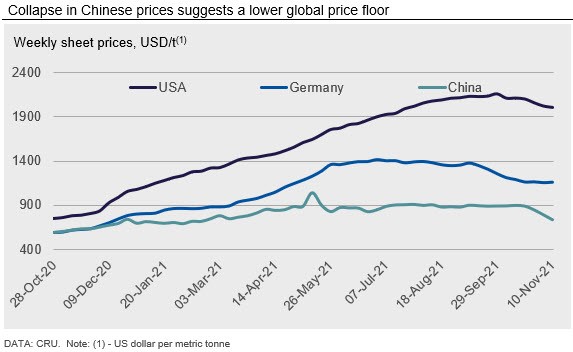

Global sheet prices have continued to fall, though declines have not been consistent across all regions. Overall, CRU’s Global Flat Products Steel Price Indicator (CRUspi flats) fell for the second consecutive month, declining by 2.9% and is now at its lowest level since May.

Declines were recorded for all three regions: Asia, Europe and North America. But Asian markets (Far East import) showed only limited declines from October. In fact, if we were to include China instead of the broader Asia market, the CRUspi flats would have fallen at a significantly faster rate. This is because prices in China have collapsed in the four weeks since our last report published. During the span of these four weeks, our domestic weekly Chinese HR coil price fell by 19% from RMB5810/tonne on Oct. 13 to RMB4700/tonne this month.

These declines in China have followed stringent cuts to electricity usage. These cuts have curtailed demand for sheet products and overall manufacturing demand. However, due to these cuts to industrial activity, the Chinese energy market is now better balanced and more capable of serving winter-related demand for heat and electricity.

Elsewhere, prices in the U.S. market have continued to fall back. But the declines have accelerated slowly. Current HR coil prices are only 7% off their peak, and U.S. prices remain at extremely high levels compared to global prices. These wide spreads have allowed buyers in the U.S. to substitute imports for a portion of their purchases and still cover various tariffs, including the S232.

However, there are now changes to the S232 tariff for Europe as it will be replaced from Jan. 1 with a tariff rate quota (TRQ). The TRQ was set at 3.3 million metric tonnes (3.6 million short tons), excluding any existing S232 product exclusions that could total an additional 1 million tonnes (1.1 million tons). That suggests the U.S. can offer a significant outlet for surplus EU steel. Note, however, that the TRQ includes not only carbon finished steel but also semis, stainless and tubes – and all of those products will compete for the total available volume. Additionally, the U.S. has announced that it is in talks with both the UK and Japan with the goal of adjusting S232. South Korea, meanwhile, has asked Washington to revisit their quota.

As Automotive Components Improve, Will Producers Focus on Smart Production Rather Than Full Production?

Across all markets, automotive production has been severely curtailed by the lack of electrical components while high material costs have hurt automakers’ bottom line. Due to slower production, vehicle inventories are extremely low and are negatively affecting sales. Yet some automakers are reporting better-than-expected earnings. These earnings have come because automakers are focused on smart production – building and selling the vehicles that provide them with the best profit margins.

As the supply of electronic components starts to improve (granted a return to normal is possibly more than a year away), perhaps automakers will refrain from ramping up production as fast as they could. In the steel industry, we have seen this same situation unfold for both the supply side at steelmakers as well as for demand in the oil and gas market. Maybe automakers can take this opportunity to improve not only which vehicles they produce but also in what quantities. Regardless, we expect that production will rise as the supply of components improves. But we are curious if automakers are able to use this as an opportunity to improve margins. Especially if other component shortages emerge due to the sudden industrial cuts that have occurred recently in China.

Outlook: Most Prices to Fall Further

Barring any new supply disruptions, we expect most global sheet prices to fall over the near term. Indian prices have countered this trend in November. And the recent, rapid drop in Chinese prices may serve as a base for a limited uptrend. But with Chinese steel production still limited by the government over the near term, prices of steelmaking raw materials may fall enough to support profitability at sheet mills. Yet, in China, it remains difficult to see any material end-use demand improvement that would support a significant sheet price rebound over the near term.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com