Market Data

December 19, 2021

Energy Market Analysis through December

Written by Brett Linton

Steel Market Update is pleased to share this Premium content with Executive members. For information on upgrading to a Premium-level subscription, email Info@SteelMarketUpdate.com.

The Energy Information Administration’s December Short-Term Energy Outlook (STEO) remains subject to high levels of uncertainty because of the unique nature of a pandemic-era economic recovery and the uncertain impact of the Omicron variant. Combine that with potential winter weather impacts and ever-evolving consumer behavior, and the result is a wide range of possible outcomes for future global energy consumption. EIA forecasts oil prices to remain near current levels throughout 2022, while natural gas prices could experience volatility as winter temperatures drive demand and prices.

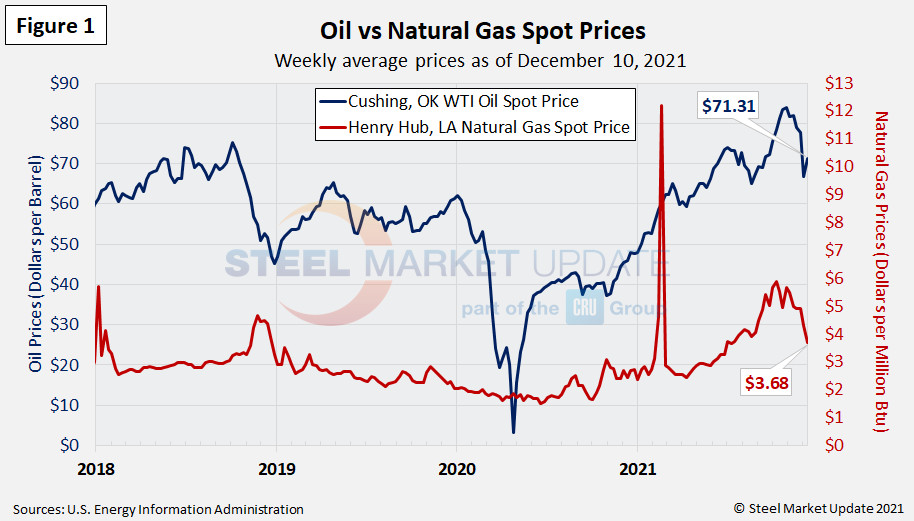

Spot Prices

The spot market price for West Texas Intermediate (WTI) was at $71.31 per barrel as of Dec. 10. Recall that six weeks prior, the spot price reached $83.84 per barrel, the highest weekly price since October 2014 when it hit $87.63. Natural gas prices continue to decline from recent highs, now at $3.68 per MMBTU (million British Thermal Units) as of Dec. 10. In early-October, natural gas spot prices reached a 7.5-year high, peaking at $5.87 per MMBTU (we are excluding the high spot-prices seen in February 2021 due to winter storms and supply scarcity). Figure 1 shows the weekly average spot prices for each product. The EIA now expects crude oil spot prices to average $73 per barrel during Q1 2022 and natural gas spot prices to average $4.58 per MMBtu over the next three months.

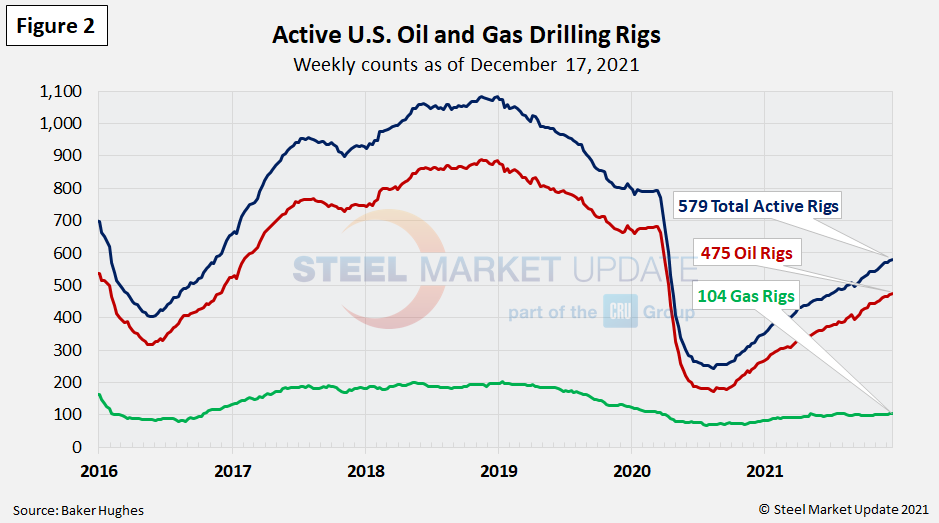

Rig Counts

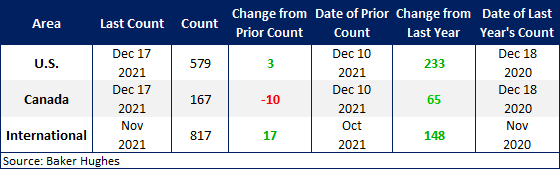

The number of active U.S. oil and gas drill rigs continues to slowly recover from the mid-2020 low. The latest count was 579 active drill rigs as of the end of last week, according to Baker Hughes, comprised of 475 oil rigs and 104 gas rigs (Figure 2). While up over recent months, active drill rigs are still down 30% from the 793 count in March 2020, just prior to the coronavirus shutdowns. EIA expects rig counts to increase into 2022 as tight oil production rises in the U.S. The table below compares the current U.S., Canadian and international rig counts to historical levels.

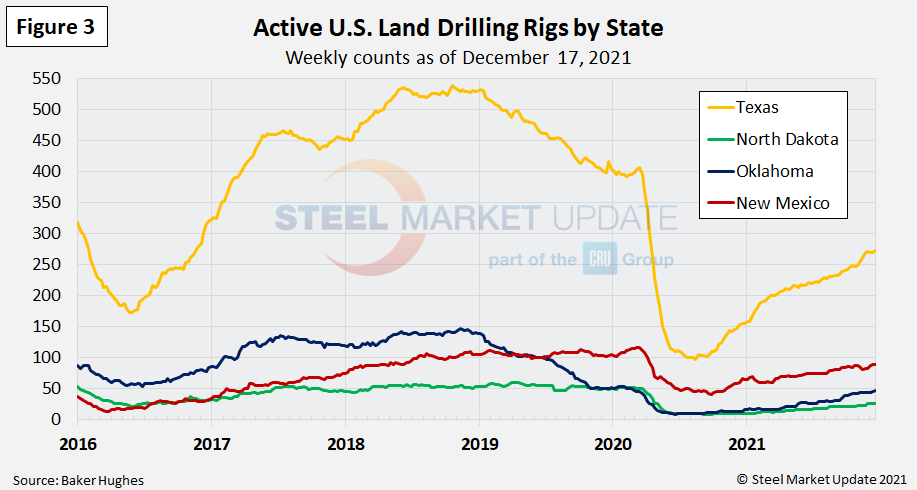

U.S. oil and gas production are heavily concentrated in Texas, Oklahoma, North Dakota and New Mexico. Production is still down as much as 48% compared to levels in March of last year. The most active state, Texas, now has 273 rigs in operation, the highest level seen since April 9, 2020. Recall that in just five months last year, Texas rigs had plummeted 76%, falling from 407 in March 2020 to 97 rigs in August 2020 (Figure 3).

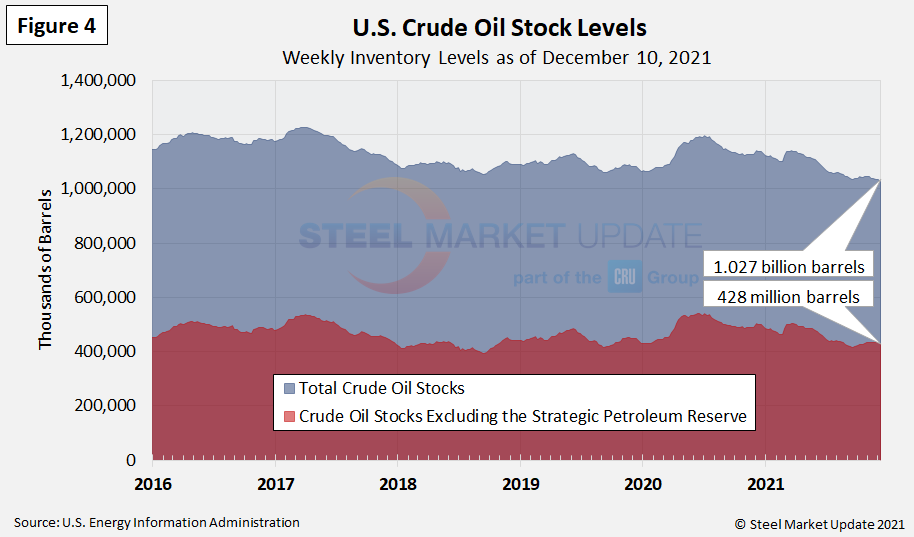

Stock Levels

U.S. total crude oil stocks continued to decline from the July 2020 high, reaching a new multi-year low of 1.027 billion barrels as of Dec. 10. This time last year stocks were at 1.138 billion barrels (Figure 4).

Trends in energy prices and rig counts are a predictor of demand for oil country tubular goods (OCTG), line pipe and other steel products.

By Brett Linton, Brett@SteelMarketUpdate.com