Prices

February 25, 2022

CRU: Sanctions on Russia to Shape Aluminum Dynamics

Written by Greg Wittbecker

By Matthew Abrams, Analyst, CRU Group

Now that we have seen the first steps of an invasion into Ukraine by Russian forces, the business concerns shift to the possibility of sanctions and how severe they might be. While initially the aluminum market itself is not expected to be directly targeted, there are various potential and indirect effects that could materialize in the coming days and weeks ahead.

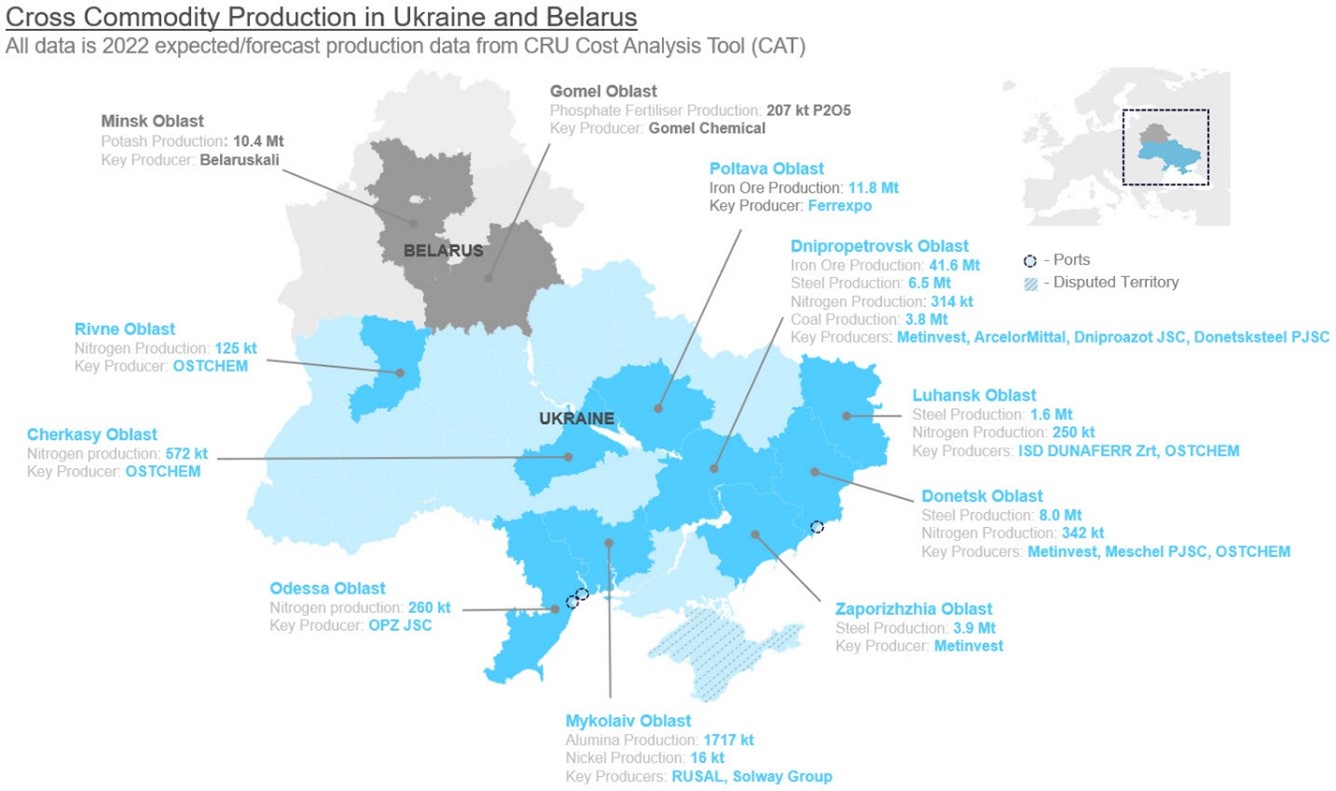

The web of connections across markets stem from Russia, stretch to Ukraine and beyond. To get a better look at things, the map below tells a very strong story (click to enlarge).

Just How Far Do These Connections Run?

The invasion into Ukraine will stretch far beyond the sanctions and the loss of production in Russia and across the region. The incremental effects coming from inside Ukraine itself, as well as other countries affected, such as Belarus, all add up. While already in a tight supply market, any potential loss of production from the region will be substantial.

Right now, Russia accounts for a significant amount of aluminum trade with the EU nations. They are one of the top five trade partners with the EU in terms of both imports and exports, accounting for over 1 million tons of aluminum trade. Overall, Russia’s share of the global aluminum supply is roughly 6%. Companies like Rusal also have operations throughout Europe and their operating status will be uncertain with travel and financial institutions being a target in the first few rounds of sanctions.

With supply chain issues already problematic, this military action will add more stress in the region. A recent WSJ article mentions freight costs rising by $3 to $5 per metric ton on Black Sea shipments, according to Kyiv-based shipping consulting firm, the Charterers. Just one more layer of expense added to the market.

There is also the issue of energy costs. With smelters curtailing capacity this past year due to high power costs, the much-needed relief expected after the winter heating season will be pushed back even further. In fact, one of the first fallouts of the conflict is the halting of the anticipated Nord 2 pipeline into Germany that was expected to ease these power concerns. With Russia providing 70% of thermal coal, 44% of LNG and 25% of oil imports into the EU, the potential for more energy disruptions remains high.

A Reuters article recently commented that the EU may have difficulty sanctioning Russia given their interdependency on energy and materials. Looking at the Rusal sanctions in 2018 which caused the price to skyrocket, a very similar situation may arise in 2022 although amplified on scale and multiplied by the already existing energy conditions.

This On Top of an Already Strained Market

Inflation. Perhaps overused in press conferences, the word “transitory” has completely disappeared from the conversation. Inflation will remain a key force in the markets. As companies have started reporting their Q4 2021 results this month, inflationary constraints are identified across the board. Not only in energy and for alloys, but also with a record number of call offs in plants around the world adding to producers’ costs. Most recently, Arconic reported that the effects of inflationary pressures totaled $71 million in the last quarter.

Freight and the supply chain have been an issue since the beginning of the pandemic and remain on watch as a significant component of the Midwest premium, which also continues to steadily increase. Compounding the freight picture there is the ongoing congestion at the ports and the driver shortages, both continue to be a challenge. The flatbed and van rates remain elevated, and the load-to-truck ratios remain near the record highs reached in Q2 2021.

Supply chain issues persist beyond logistics. The semiconductor bottleneck in the automotive supply chain is causing many rolling mills to reposition their products into other markets such as HVAC or packaging to keep production and shipments aligned.

Where Does That Leave Us?

Metal prices will undoubtedly stay high, reaching new record levels of $3,449 /t on the LME this week and the U.S. Midwest premium hitting $0.37 per pound.

Unsure exactly how long any sanctions will last, the effects of Section 232 passed in 2017 may provide a view as to how greater sanctions will impact the metals markets. The result then was higher prices and subsequently a shift to onshoring, with investments to increase domestic capacity in the U.S.

Couple this with other key themes…

• Consumer preference for low-carbon aluminum

• Nationalistic aversion to Russian supply

• De-risking global supply chains and logistics costs

…and the reshaping of domestic supply chains comes into view.

CRU concludes that upward price risk remains a pressing concern and the restarting of some aluminum smelting capacity in the EU will very likely be delayed. Also, looking back to last week, those unaccounted-for stocks held by financial institutions could very likely come into play sooner than expected. A last trend to consider will be how trade flows adapt, with potentially more Canadian primary production being sent to the EU. With Japan also voicing their support for sanctions, Russian metal will also have to find a new home, with China being a possible route.

Editor’s note: CRU’s Matthew Abrams is filling in for our regular correspondent Greg Wittbecker, who is traveling.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com