Overseas

March 17, 2022

CRU: War in Ukraine and Covid Create Divergent Sheet Price Paths

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Sheet Products Monitor, March 16

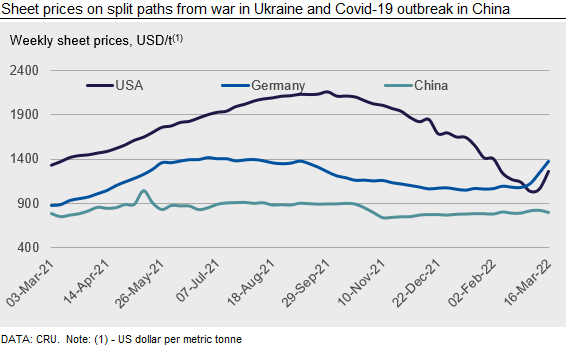

Global sheet prices took notably different directions this week as the war in Ukraine caused record w/w increases in Europe and the USA, while a fresh outbreak of Covid-19 in China pushed domestic prices lower and prevented increases in other Asian markets. Large European price increases prompted Indian exporters to target buyers in that region, resulting in notably higher domestic prices in India. However, domestic buyers in other parts of Asia have been hesitant to accept higher offers after Chinese domestic prices underwent their most significant weekly decline in months. We expect to see high levels of price volatility in the coming weeks as a result of these two developments.

USA

Sheet steel prices in the USA soared this week after the war in Ukraine caused prices of steelmaking raw materials to climb dramatically. HR coil jumped by 19% ($182 /s.ton) w/w, which is the largest weekly change CRU’s index has recorded. Still, buyers report that their inventories are either in balance with current demand or a bit heavy and will wait 45-60 days before they are comfortable purchasing larger amounts of material. Many buyers with mill contracts said that their allotted tonnage will be enough to cover their needs and that they are not looking to purchase extra tons. There are rising concerns that rapidly rising inflation along with uncertainty over future economic conditions will begin to dampen consumer spending on steel-intensive goods like automobiles and appliances.

Prices for sheet steel remained stable on the U.S. West Coast this week, although there were some reports of increases for HR coil and HDG coil ranging between $80-100 /s.ton for spot transactions. Buyer inventories are still relatively large, and there is imported material waiting to be unloaded at the ports.

Europe

European sheet prices have shot up once again this week with all German sheet products up by €110–162 /t w/w. Prices in Italy rose by €99–112 /t w/w. Steel supply chains have been greatly impacted by the war in Ukraine, especially for semifinished steel and raw materials. In our latest assessment, German and Italian HR coil were assessed at €1,253 /t and €1,183 /t, respectively. These prices are well above any absolute highs seen in the summer of 2021 during the peak of the pandemic.

One leading European producer has hiked their sheet prices by around €150 /t w/w for a second week in a row. Prices are increasing on an almost daily basis and this instability has led to panic among some market participants. Many customers are not able to confirm or commit to deals because of this uncertainty. The main concern of many market participants in today’s market is how these high steel and energy costs will be passed through to customers. Italian flat producers have already taken the approach of including an additional energy surcharge in their existing contracts made before the start of March.

China

Chinese domestic sheet prices recorded the most significant weekly decline in months. Sheet prices fell by RMB70-180 /t across the board over the past week as sentiment collapsed on the recent Covid-19 outbreaks across the country. Although the latest released macroeconomic indicators in January and February are better than market expectations, participants become pessimistic due to slower underlying demand recovery given strict regional lockdowns. Shipping and truck delivery will also be extended given stricter quarantine requirements. Consequently, sheet inventories quickly dropped by 3% w/w as traders rushed to the spot market and clear stocks given market uncertainties. On the supply side, production is expected to increase as the government’s two sessions and air quality control due to the Winter Paralympics has now ended. With the expected production increases but slower demand recovery, steel mills will face a tough period again with a “double squeeze” ahead, referring to the push from elevated production costs but reluctance from end-users to accept any price increases. Therefore, we expect sheet prices to stay volatile in the coming weeks.

Asia

Prices of imported sheet products in the Asia market were stable last week as market sentiment grew increasingly bearish amid a drop in Chinese domestic prices. For HR coil SAE1006, Chinese material remains the least expensive with steady offers at $910-920 /t CFR Vietnam. Even so, buyers were not keen to bid as they would prefer to wait for price updates from Vietnamese mills. Mills from South Korea, Japan and India were not keen on selling to Vietnam because they were able to achieve higher prices by selling to the European market.

For HR coil/sheet SS400, there was a sharp fall in the Chinese futures market. Therefore, offers for Chinese material of this grade slightly fell this week. In addition, some small mills were worried about domestic demand due to the recent Covid-19 outbreak in China and were eager to get more volumes on in the export market.

CRU assessed HR coil prices at $910 /t CFR Far East Asia, flat w/w. CR coil prices were assessed at $1120 /t CFR Far East Asia, up by $60/t w/w, while HDG prices were assessed at $1,140 /t CFR Far East Asia, a $50 /t increase w/w.

India

The CRU-assessed Mumbai delivered HR coil price increased by $73 /t (or 6.8%) w/w to surpass the previous historically high level during in the third week of November 2021, with similar price hikes being recorded for downstream sheet products. These prices are being driven up by strong export orders to Europe at premium prices (with the latest HR coil export price being just over $1,100 /t FOB against the latest domestic price of $971 /t excluding taxes). Sharp increases in input costs due to costlier coking coal and low threat of imports because of non-tariff trade barriers are also aiding these price increases.

Sheet market activity has increased in the last few weeks as bullish sentiment has buyers concerned about near-term supply shortfalls. Local traders have also been actively restocking to gain from sharp price upswings, leading to a reduction in mill inventories. Consequently, steelmakers are promptly passing rising coking coal costs to the market, allowing them to maintain margins. Given that EU officially banned Russian steel imports earlier this week, there is a likelihood of higher volume of Indian sheet making its way into Europe in the near term, which has the potential to keep Indian export and domestic price offers elevated. A possible risk to Indian export prospects is Chinese steelmakers deciding to increase their export allocation to gain from the ongoing price rally.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com