Overseas

March 24, 2022

CRU: Raw Material Price Increases Cause Global Sheet Price Hike

Written by Ryan McKinley

By CRU Senior Analyst Ryan McKinley, from CRU’s Steel Sheet Products Monitor, March 23

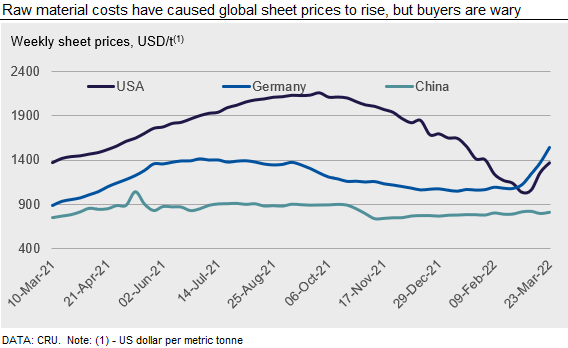

Persistently high steelmaking raw material prices and restricted global production pushed sheet prices higher w/w across the world. The largest of these increases were in Europe and the USA, with prices rising by triple-digit amounts for yet another week. Still, domestic buyers in both markets are growing wary of this sharp price spike and are generally only making purchases when necessary. Nearly all Asian exporters are now focused on sending material to Europe given the quick rise in prices there, leaving Chinese exporters as the only option for importers in other parts of Asia. Between this and logistical issues caused by the recent Covid-19 outbreak in China, prices around Asia were also up w/w.

USA

Rising raw material costs and heightened buying activity pushed sheet steel prices higher in the USA. HR coil rose by $98 /s.ton w/w, an 8.6% increase. CR coil and HDG coil also increased w/w, gaining $112 /s.ton and $146 /s.ton, respectively. Mills were reluctant to quote on inquiries as the war in Ukraine forced them to evaluate raw material supply lines and reconcile rapidly increasing costs. While some service centers and distributors have described worried customers beginning to pull forward 2022 Q2 requirements to ensure supply, those companies servicing OEMs have noticed a downturn in demand. Supply-chain issues have caused production disruptions across various manufacturers, which have resulted in a 15-30% difference between projected and actual steel usage, according to our contacts. There is growing unease that customer demand for steel-intensive goods will weaken if disposable income continues to shrink as inventory levels rise following the most recent buying spree beginning in late February.

U.S. West Coast mill prices remained steady this week as buyers awaited the opening of regional mill May order books and struggled to obtain quotes from domestic mills located in other regions. Demand has been solid as downstream customers begin pulling forward requirements to minimize the chances of running out of critical sizes.

Europe

European sheet prices soared this week after domestic producers hiked their offers on the back of continued supply disruptions from both Russia and Ukraine. Prices are changing daily, triggering a cautious approach from buyers who are holding off on purchases unless they desperately need it. In our latest assessment, German and Italian HR coil were assessed at €1,399 /t and €1,296 /t, respectively. This is a €146 /t and €113 /t w/w increase for both regions.

The massive domestic price increases over the past weeks have attracted offers from abroad. A Japanese supplier was heard to be offering CR coil to German buyers earlier this week at $1,380–1,400 /t CFR (~1,260 Eur /t CFR). This is somewhat attractive considering the current level that European producers are offering and the limited availability of material in domestic markets as input costs rise.

China

Chinese domestic sheet prices rose by RMB60-80 /t over the past week. Although the recent Covid-19 outbreak across the country has slowed the pace of the demand recovery, a new lockdown in Tangshan city of Hebei province has started to impact the steel supply chain. Local governments are enforcing a “Zero Covid-19 Case” strategy, requiring stricter testing and quarantines for both individuals at risk and those involved in steel logistics. The normal pace of transportation for steelmaking raw materials into Tangshan, as well as steel products out of the city, is expected to be delayed. Finished steel inventories, including sheet products at mill warehouses, have increased at a rapid rate while traders halt purchases from steel mills given logistics issues. This will prevent steel mills from maintaining the same production schedules. Meanwhile, existing steelmaking raw materials stocks can support normal production for up to 10 days, but integrated mills are worried about insufficient feedstocks going forward, which could lead to production halts or hot idlings. Nevertheless, buyers are still reluctant to place any big orders given such a volatile market, and the slower than expected demand recovery is also limiting this price increase. In this regard, we expect the recent sheet price increase will be supported by the expected output reduction in the coming weeks, but will be limited by the supply resumption after Covid-19 cases fall.

Asia

Prices of imported sheet products in Asia edged up this week as sellers continue to lift their offers. Only Chinese HR coil was available for Asian importers and offers were at $875 /t CFR Vietnam for SS400 grade and at $915-925 /t CFR Vietnam for SAE1006 grade. According to market sources, mills from India, Korea and Japan were not keen on offering to Asia because they can achieve much higher prices by selling to the European market. Their current HR coil offers are already above $1,000 /t on an FOB basis.

In addition, Formosa Ha Tinh released their new offer for May shipment. HR coil rerolling grade was offered at $930 /t CFR Vietnam, which is a $90 /t increase m/m. Hoa Phat offered their HR coil at $910 /t CFR Vietnam (a $80/t m/m increase).

CRU assessed HR coil prices at $920 /t CFR Far East Asia, a $10/t rise w/w. CR coil prices were assessed at $1,140 /t CFR Far East Asia, while HDG prices were assessed at $1,160 /t CFR Far East Asia, both up by $20 /t w/w.

India

Sheet buying activity eased in the past week after signs of buyer resistance to high prices emerged. HR coil price is unchanged w/w, while that of downstream products rose in the latest reported transactions. Several consumers are citing inflationary pressures and restricting themselves to need-based purchases. On the other hand, some steelmakers have started invoking force majeure clauses in their short- and long-term sales contracts, advising customers to either accept a price hike and continue with the existing contracts or renegotiate. They are attributing this force majeure to sharp increases in raw material cost (particularly that of coking coal) due to the global geopolitical situation.

While the domestic HR coil price has eased w/w, steelmakers have increased export offers to European buyers by $50 /t w/w to $1,300 /t CFR for May deliveries. Given that the European Commission has raised HR coil import quotas for Indian suppliers from 166,028t for Q1 to 273,178t for Q2 following the ban on Russian imports, enquiries for Indian HR coil from European buyers have increased.

Request more information about this topic.

Learn more about CRU’s services at www.crugroup.com