Market Data

June 17, 2022

Service Center Shipments and Inventories Report for May

Written by Estelle Tran

Editor’s note: Steel Market Update is please to share this abbreviated Premium content with our Executive members. For information on how to upgrade to a Premium-level subscription, email Info@SteelMarketUpdate.com. If you are part of a service center company and interested in becoming a data provider, please contact Estelle.Tran@CRUGroup.com.

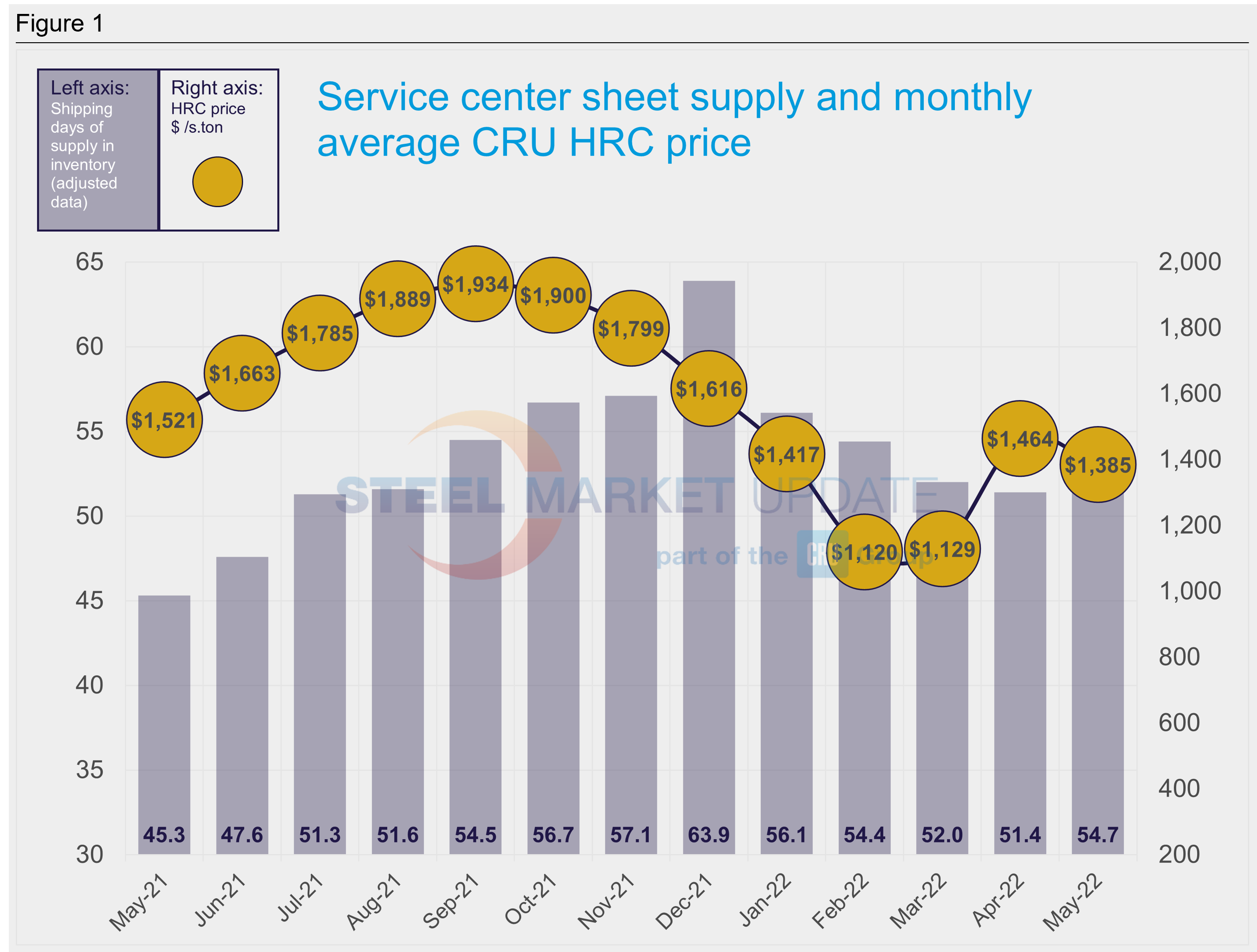

Flat Rolled = 54.7 Shipping Days of Supply

Plate = 55.2 Shipping Days of Supply

Flat Rolled

US service center flat rolled inventories rose in May as many service centers reported signs of slowing demand. At the end of May, service centers carried 54.7 shipping days of supply on an adjusted basis, according to SMU data. This was up from 51.4 shipping days in April. In terms of months of supply, service centers had 2.6 months of supply in May, which was consistent with 2.57 months in April.

May had 21 shipping days compared to April’s 20. Some service centers saw a decline in shipments in May despite the extra shipping day, and the daily shipping rate declined month-on-month. Ongoing supply chain issues, falling sheet prices and worries about falling demand or delayed projects have contributed to a slowdown in shipments. Market contacts expressed anxiety about the economy and about falling consumer spending, labor issues and ongoing supply chain stress. Service center contacts noted weaker demand in the automotive, appliance and agricultural sectors.

The amount of flat rolled on order has continued to fall after reaching a high point in March.

Considering 2019 levels and weaker demand outlooks, the amount of material on order still appears to be high. Some of this could be tied to imports with longer lead times.

We expect the amount of material on order to fall significantly as mills catch up on orders and as service centers remain hesitant about making new purchases. The SMU survey published June 9th found that 57% of service centers were maintaining inventory and that the remaining 43% were reducing inventory. As prices decline, service centers are seeing more customers sitting on the sidelines. This is a trend that we expect will continue heading into the summer slowdown.

Plate

US service center plate inventories increased again in May, after reaching a low point in March. At the end of May, service centers carried 55.2 shipping days of plate supply, according to SMU data. This is up from 48.3 shipping days in April. Plate inventories represented 2.63 months of supply in May, up from 2.41 months in April.

We expected some inventory building because of slowing shipments, and in May we saw the weakest daily shipping rate since December. Views on shipments have been mixed though. Anecdotally, service centers said that demand has been steady or even strong in the near term. Unlike sheet, some service centers reported steady or stronger shipments month-on-month but with more competition for resale. There are concerns about the pipeline for projects though, and some have expressed disappointment that there has not been more demand from the energy or construction sectors.

The amount of plate inventory on order fell in May. We are seeing plate lead times shorten in general with plate lead times hovering just above five weeks in the last three surveys.

Plate prices have slipped since Nucor announced a plate price decrease effective with the opening of July its order book. But the declines have been more moderate than those seen in sheet partly because of the lack of import competition.

By Estelle Tran, Estelle.Tran@CRUGroup.com