Market Data

June 24, 2022

CRU: Green Transition Will Disrupt Steel Trade Flows

Written by Paul Butterworth

By CRU Research Managers Sarah Macnaughton and Paul Butterworth, and contribution from CRU Sustainability Analysts Zsombor Garzo

International trade is an essential part of the global steel industry, with over 20% of steel production traded today. However, as the world moves towards decarbonization, CRU finds that established trade flows are at risk. The green transition will lead to a fundamental restructuring of the industry’s cost curve, shifting traditional regional cost competitiveness. A low-cost position today is no guarantee of future cost competitiveness.

Steel Trade Is a Major Source of CO2 Emissions

The global steel industry is responsible for around 10% of global CO2 emissions annually and, in absolute terms, is the largest emitter in the metals commodity sector. As climate policies grow, the industry is facing increasing pressure to decarbonize, and this has sparked wide discussions about so-called ‘green’ steel. Much of the discussion on steel decarbonization has focused on individual companies’ green steel initiatives. An oft-overlooked fact is that the switch to green technology will result in a fundamental change in the steel industry’s cost structure and regional cost competitiveness, and this is likely to trigger changes in trade flows.

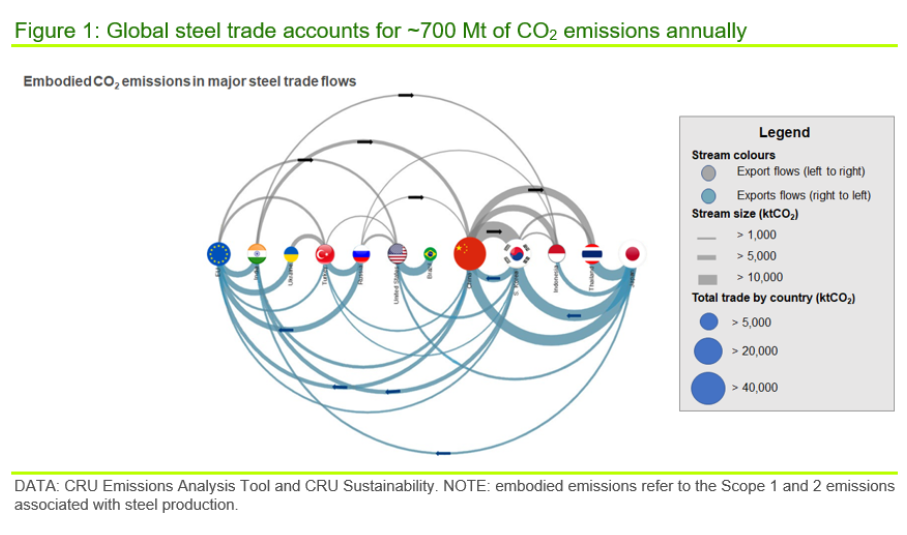

Today, ~20% of steel production is traded globally, representing an embodied carbon footprint of ~700 MtCO2/y – similar to the annual emissions output of Germany. These trade-related emissions are distributed unevenly across regions, as illustrated in Figure 1. The largest exports of embodied emissions are concentrated in a few key countries: South Korea, China, Japan, and Brazil. The EU and US are both major net importers of embodied emissions, which has helped to stimulate discussions about carbon border taxes among policymakers on both sides of the Atlantic.

Cost competitiveness is the biggest determinant of a country’s steel emissions trade position. The major steel exporting countries such as China, South Korea, and Brazil have low-cost, but relatively high emitting, blast furnace-basic oxygen furnace (BF-BOF) dominant industries based on competitive raw materials and labor costs. Conversely, steel net importing regions such as the US and Europe have higher cost, lower-emissions intensive steel industries that typically use high quality and higher-cost raw materials. With raw materials accounting for ~60-80% of steel production costs today, raw material competitiveness is the key driver of cost position. However, this will not necessarily hold true in a future decarbonized steel industry based on green technologies.

Green-Tech Will Alter the Steel Industry’s Cost Structure

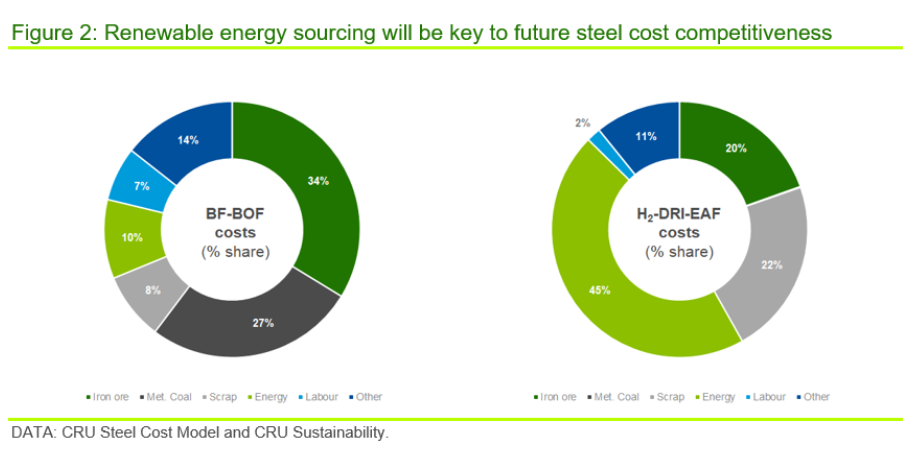

Figure 2 illustrates the typical cost structure of a BF-BOF steel plant and projected costs for a green hydrogen-based direct reduced iron-electric arc furnace (H2-DRI-EAF) in 2030. We have chosen to model H2‑DRI‑EAF costs as the proxy for green steel costs because we expect this to be the most developed low carbon technology by 2030 based on the current project pipeline.

The two steel technologies have very different cost structures that reflect the switch from fossil fuel to an electricity-derived reductant. Production of green hydrogen is extremely energy-intensive, with ~3 MWh of electricity needed to produce enough hydrogen to convert 1 ton of iron ore to DRI. As a result, energy costs are the major component of H2-DRI-EAF costs, accounting for ~45% of inputs, while raw materials account for ~40% of costs. By comparison, BF-BOF costs are mostly driven by raw materials that make up ~70% of a typical plant’s costs.

The shift to the more electricity-intensive H2-DRI-EAF process has important implications for global steel cost competitiveness because the drivers of renewable cost competitiveness are very different from those for raw material costs. Amongst other factors, local weather patterns play a key role in determining a region’s renewable cost competitiveness, whereas raw material competitiveness is mostly driven by local geology. These nuances mean that steelmaking regions that have a structural cost advantage today will not necessarily maintain their competitiveness in the future.

US and China to Benefit from the Switch to Green Steelmaking

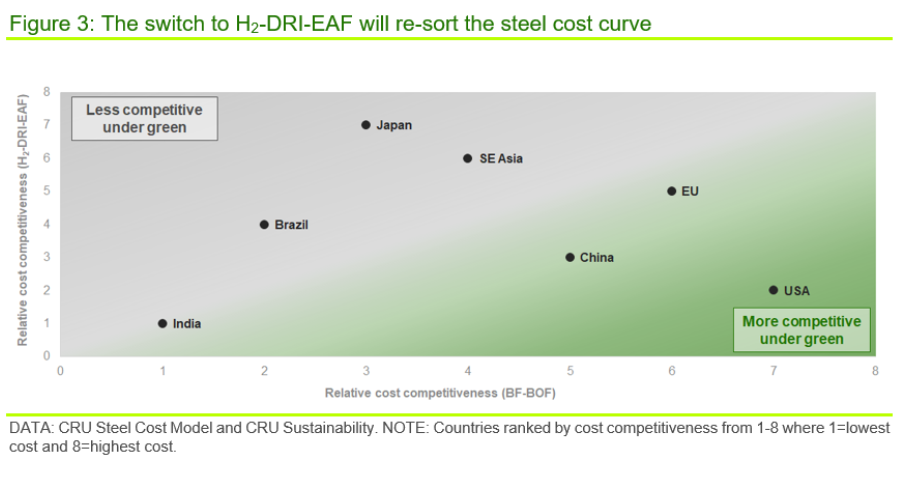

To test the impact of green technologies on regional global steel cost trends, CRU has undertaken research into renewable electricity cost trends and used this to derive costs for a theoretical H2-DRI-EAF plant in each of the major steelmaking regions in 2030. The results are shown in Figure 3 below. The x-axis indicates the relative cost position of each region under conventional BF-BOF technology, while the y-axis indicates the relative cost position under H2-DRI-EAF technology. Regions in the bottom right-hand quadrant have an improved cost position under the H2-DRI-EAF process (i.e., have moved from a high-cost to low-cost position). Regions in the top left-hand quadrant of the chart have reduced competitiveness under H2-DRI-EAF technology.

This analysis is based on typical operating parameters for each region and there may be differences between plants based on individual plant configuration, location, and power supply agreements. Nevertheless, our analysis suggests a dramatic shift in regional cost position in the major steel economies:

Japan shows a significant drop in competitiveness under H2-DRI-EAF steelmaking. The country is a major steel exporter today, but it would be difficult to maintain this role if it moved to a high-cost position. As a result, we could see increased Japanese investment in overseas production facilities, with better access to competitive renewable energy.

The US becomes significantly more cost-competitive under H2-DRI-EAF. The US is a major steel importer today, yet its improved cost position could see it expand steel capacity and shift to a neutral or net exporter position.

China becomes more competitive under green technology. The country is already a net exporter of steel but it could pivot its exports to capitalize on growing demand for green steel. Historically, the country’s steelmakers have shown the ability to build new capacity at a more rapid rate than global peers and at a lower cost, which means it could leapfrog the EU as the world’s major green steel producer if conditions allow.

Steel Exporters Will Need to Adapt in a Low Carbon World

From a cost perspective, there are clear winners and losers in a greener steelmaking world. However, there are a number of other headwinds for steel exporters on the road to decarbonization. Emerging carbon price and carbon border tax schemes will increasingly favor suppliers of lower carbon steel. Downstream consumers are already demanding low carbon steel products to meet their own supply chain emission goals, meaning steelmakers will need to reduce emissions to maintain market share in key customer segments. Finally, it is worth considering the impact of national greenhouse gas targets. Nations targeting strict emission reductions may increasingly scrutinize the value of generating millions of tonnes of CO2 emissions to satisfy overseas consumer demand. We have already seen local environmental concerns halt mining projects in regions such as Australia and Chile, and similar issues could yet emerge in the steel sector with regard to CO2 impacts.

The ultimate magnitude and timing of decarbonization-led trade disruption are still unclear, but one thing is certain – future steel trade flows will not look like those of today.

If you have any questions or want to discuss our research into green steel or the energy transition more generally, please get in touch. We will be happy to talk.

If you would like to find out more about carbon pricing schemes, other policy measures aimed at mitigating climate change or carbon price developments, please get in touch with us. We are more than happy to talk.

Learn more about CRU’s services at www.crugroup.com